A DSCR loan for Airbnb lets you buy a short-term rental property based on what the property earns. Not what you earn on a W-2 or tax return. If you’ve been running rental arbitrage and you’re ready to stop paying rent to a landlord while your guests pay you, DSCR financing is the bridge between operating someone else’s building and owning yours. I’ve watched dozens of arbitrage operators make this transition. The ones who understand DSCR lending move faster and build real wealth. The ones who don’t stay stuck on the arbitrage treadmill.

Below I’m breaking down exactly how DSCR loans for Airbnb work in 2026, what the real requirements look like (not the vague fluff you’ll find on lender websites), current interest rates, how lenders actually calculate your short-term rental income, and the step-by-step playbook for going from arbitrage profits to property ownership using DSCR financing.

What Is a DSCR Loan and How Does It Work?

DSCR stands for Debt Service Coverage Ratio. It measures one thing: can this property’s income cover its own debt obligations? That’s the whole game. The lender doesn’t care about your W-2, your tax returns, your employer, or your personal debt-to-income ratio. They care about whether the rental property’s income is enough to service the mortgage loan.

This is a fundamentally different approach from traditional lenders. A conventional mortgage lender wants to see your personal income, employment history, and debt-to-income ratio below 43-45%. A DSCR lender wants to see the property’s income potential, period.

The DSCR Formula

DSCR = Gross Monthly Rental Income ÷ Total Monthly Debt Service (PITIA)

PITIA breaks down to Principal, Interest, Taxes, Insurance, and Association dues (HOA if applicable). So if a vacation rental generates $5,000 per month in rental income and the total PITIA is $4,000, the debt service coverage ratio is 1.25x. That means the property earns 25% more than it costs to carry, and that’s the sweet spot for most DSCR lenders.

Here’s a quick reference for how lenders view different DSCR ratios:

| DSCR Ratio | What It Means | Lender Appetite |

|---|---|---|

| Below 0.75x | Property loses money significantly | Most lenders decline |

| 0.75x, 0.99x | Property doesn’t fully cover debt | Some “no-ratio” programs accept this with 25-30% down |

| 1.0x | Property breaks even on debt service | Minimum threshold for many lenders |

| 1.0x, 1.24x | Small positive cash flow margin | Approved, but rates may be higher |

| 1.25x, 1.49x | Property comfortably covers debt | Best rates and terms available |

| 1.5x+ | Strong property cash flow | Premium pricing, easiest approval |

A 1.25x ratio is what I tell every arbitrage operator to target. It gives you enough cushion for slow months, unexpected repairs, and the inevitable gaps between guests. Anything above 1.5x and you’re in excellent shape, lenders will fight for your business.

Why DSCR Works for Short-Term Rental Properties

Here’s why DSCR loans and short-term rental properties are a natural fit: vacation rentals generate 2-3x the income of traditional long-term leases in the right markets. A house that rents for $1,800/month on a year-long lease might pull $4,500-6,000/month on Airbnb. That higher revenue pushes the DSCR ratio well above 1.0x, making it easier to qualify than you’d expect.

The catch? DSCR lenders know that short-term rental income is more volatile than a signed 12-month lease. So they apply discount factors, typically crediting only 75-90% of projected income from platforms like AirDNA, or 90-100% of actual booking history from your Airbnb or VRBO account. More on that calculation below.

Why DSCR Loans Are the Best Financing for Airbnb Investors

If you’re a real estate investor, especially one building a portfolio of rental properties, DSCR loans solve the three biggest problems that block scaling:

No Personal Income Verification Required

This is the killer feature. Conventional mortgages require W-2s, tax returns, pay stubs, and a debt-to-income ratio below 43-45%. If you’re self-employed, run an LLC, or write off business expenses aggressively (like most smart real estate investors do), your tax returns make you look broke on paper.

DSCR loans skip all of that. No personal income verification. No tax returns. No W-2s. The lender evaluates the investment property on its own merits. Can the projected rental income cover the monthly mortgage payment? If yes, you qualify.

For rental arbitrage operators who are already self-employed and writing off expenses, this is a major shift. Your personal tax situation becomes irrelevant.

You Can Close in an LLC

Most conventional mortgages require you to borrow in your personal name. DSCR loans let you close in an LLC, which is exactly what you should be doing for liability protection on short-term rental properties. If a guest slips on your stairs or your local regulations create legal exposure, the LLC shields your personal assets.

No Cap on Number of Properties

Conventional lenders typically cap you at 10 financed properties. After that, good luck getting approved. DSCR lenders don’t care how many properties you own. If each investment property cash flows on its own, you can keep buying. I’ve seen investors hold 15, 20, even 30+ DSCR loans simultaneously. Each property stands on its own math.

This is how seasoned real estate investors build portfolios of multiple properties without hitting the conventional lending wall.

The Natural Progression: Arbitrage to Ownership

If you’re running rental arbitrage profitably, you already have the hardest skill: knowing how to operate a short-term rental that makes money. The missing piece is usually capital for a down payment and a financing vehicle that works for someone with non-traditional income. DSCR loans solve the financing side. Your arbitrage profits solve the capital side.

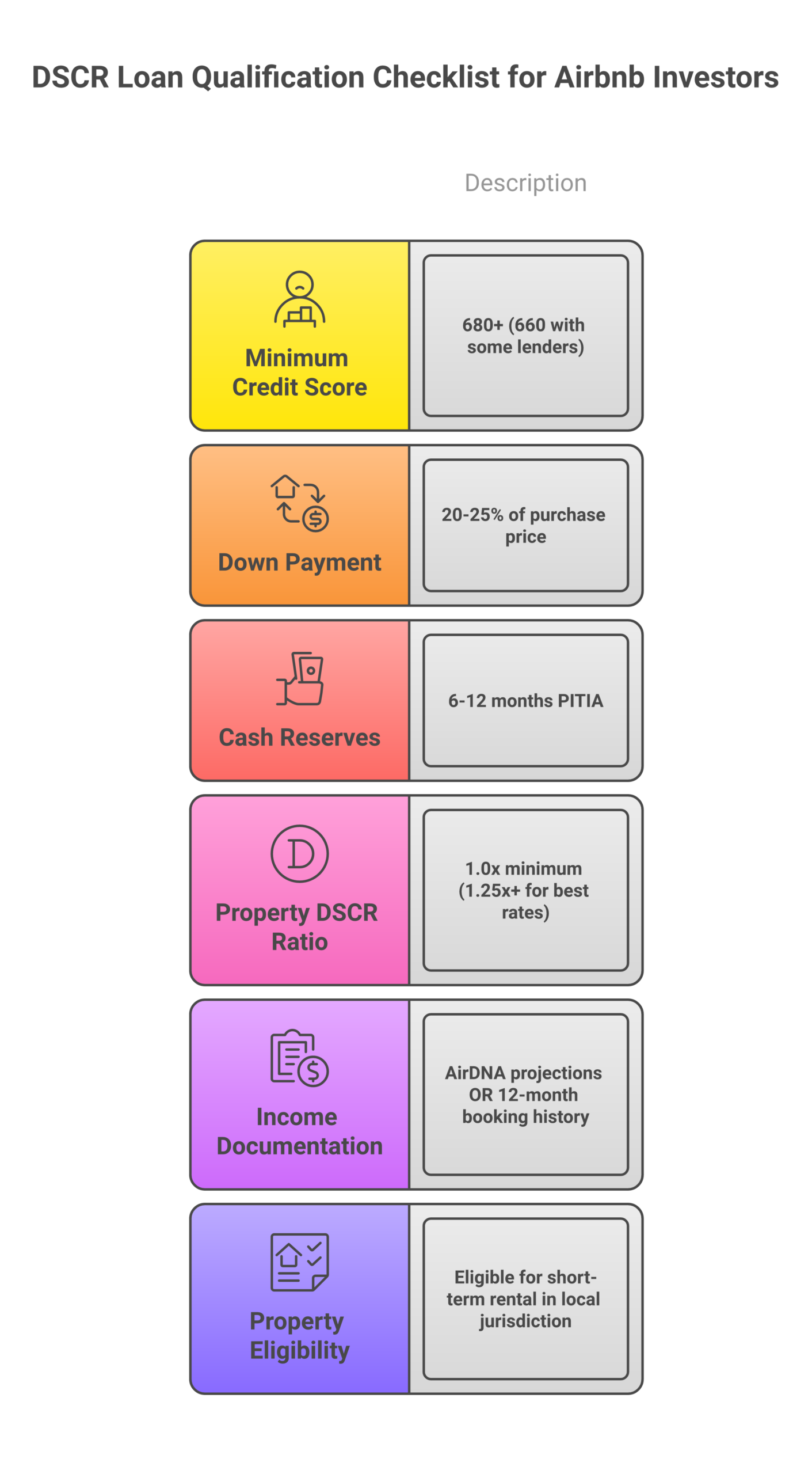

DSCR Loan Requirements for Airbnb Properties in 2026

Every lender is slightly different, but here are the real requirements you’ll encounter across most DSCR loan programs in early 2026. I’m giving you actual numbers. Not the sanitized ranges lender websites publish.

Minimum DSCR Ratio

Most lenders want a 1.0x minimum, the property at least breaks even. But the sweet spot is 1.25x or higher. At 1.25x+, you get access to the best rates and most favorable terms. Some “no-ratio” or “reduced doc” programs will go as low as 0.75x, but expect a higher down payment (25-30%) and an interest rate premium of 0.5-1.0%.

Down Payment

Standard range: 20-25% of the purchase price. For a $350,000 investment property, that’s $70,000-$87,500 out of pocket. Some lenders will go to 15% down if your DSCR ratio is above 1.5x and your credit score is 740+, but don’t count on it, 20% is the realistic floor for most borrowers.

Cash-out refinances typically max out at 70-75% loan-to-value. So if your property is worth $400,000, you can pull out up to $280,000-$300,000 minus your existing mortgage balance.

Minimum Credit Score

Here’s how credit tiers actually affect your DSCR loan pricing:

| Credit Score Range | Rate Impact | Availability |

|---|---|---|

| 740+ | Best rates (Tier 1) | All DSCR lenders |

| 700-739 | Slight premium (+0.25-0.50%) | Most DSCR lenders |

| 680-699 | Moderate premium (+0.50-1.0%) | Standard DSCR lenders |

| 660-679 | Higher premium (+1.0-1.5%) | Flexible DSCR lenders |

| 620-659 | Highest premium (+1.5-2.0%) | Limited availability, higher down payment |

The minimum credit score for most DSCR programs is 660-680. A few flexible lenders go down to 620, but expect punitive rates. My honest advice: if your score is below 680, spend 3-6 months improving it before applying. The interest rate savings over a 30-year loan will dwarf whatever you “save” by rushing.

Reserve Requirements

Lenders want to see cash reserves after closing, typically 6-12 months of PITIA sitting in your bank account. For short-term rental properties, many lenders lean toward the higher end (9-12 months) because Airbnb income is seasonal and more volatile than long-term lease income.

On a property with a $3,500 monthly PITIA, that means $21,000-$42,000 in reserves on top of your down payment and closing costs. This catches a lot of first-time buyers off guard. Budget for it.

Property Types That Qualify

DSCR loans work for most residential investment property types:

- Single-family homes – the most common and easiest to finance

- Condominiums – with HOA approval for short-term rentals (verify this before buying)

- Townhomes – generally straightforward

- 2-4 unit properties – multi-unit buildings where each unit can generate rental income

- Cabins, lake houses, and unique properties – select lenders only, often at a premium

The property must be in a jurisdiction where short-term vacation rentals are legally permitted. Lenders will verify this. Don’t waste everyone’s time applying for a DSCR loan on a property in a city that bans Airbnb.

Airbnb Income Documentation

This is where DSCR for short-term rentals differs from traditional rental DSCR. Lenders need to verify the projected rental income somehow. They accept:

- AirDNA market reports – the industry standard for STR income projections (more on this below)

- 12-24 months of actual booking history from Airbnb, VRBO, or other platforms

- 1007 rent schedule from an appraiser (less common for STR, more for long-term)

- CPA-prepared profit and loss statement – for multi-platform or direct-booking operators

DSCR Loan Interest Rates and Terms in 2026

Let me give you the real numbers instead of the aspirational rates lenders advertise.

Current Rate Ranges (February 2026)

As of early 2026, 30-year fixed DSCR loan rates for well-qualified borrowers (740+ credit, 1.25x+ DSCR, 25% down) start around 6.125%, with most programs falling in the 6.12-6.62% range. Here’s how it breaks down by lender tier:

| Lender Tier | Rate Range | Typical Borrower Profile |

|---|---|---|

| Tier 1 (Prime) | 5.75%, 6.25% | 740+ credit, 1.25x+ DSCR, 25% down |

| Tier 2 (Standard) | 6.25%, 7.25% | 680-739 credit, 1.0x-1.24x DSCR, 20-25% down |

| Tier 3 (Flexible) | 7.25%, 8.75% | 660-679 credit, 0.75x-0.99x DSCR, 25-30% down |

Yes, DSCR rates run about 0.5-1.5% higher than conventional mortgage rates. That premium is the cost of skipping personal income verification. For most real estate investors, it’s a bargain, the ability to qualify without tax returns and scale without property limits is worth far more than a half-point on your interest rate.

DSCR vs Conventional Rate Comparison

| Feature | DSCR Loan | Conventional Mortgage |

|---|---|---|

| Rate range (Feb 2026) | 5.75%, 8.75% | 5.25%, 7.25% |

| Income verification | None (property-based) | Full (W-2s, tax returns, pay stubs) |

| Debt-to-income check | No | Yes (max 43-45%) |

| Close in LLC | Yes | Usually personal name only |

| Property limit | None | Typically 10 |

| Down payment | 20-25% | 15-25% |

| Closing timeline | 30-45 days | 45-60 days |

| Best for | Self-employed, portfolio builders, LLC owners | W-2 employees with clean tax returns |

ARM vs Fixed Rate Options

Most DSCR loans are 30-year fixed, but adjustable-rate options exist. ARMs typically start 0.5-1.0% below fixed rates with a 5/1 or 7/1 structure (fixed for 5 or 7 years, then adjusts annually). The ARM makes sense if you plan to sell or refinance within 5-7 years. For a buy-and-hold Airbnb property, I’d lock the 30-year fixed and forget about it.

Prepayment Penalties

Most DSCR loans carry a prepayment penalty, typically a 3-2-1 step-down (3% of the loan balance in year 1, 2% in year 2, 1% in year 3) or a 5-year flat 1-2% penalty. On a $280,000 loan, a 3% prepayment penalty is $8,400. That’s real money.

Ask about the prepayment structure before you sign. Some lenders offer a “no prepay” option at a 0.25-0.50% rate premium. If you think you’ll refinance within 3 years, the no-prepay option might save you thousands.

How Lenders Calculate Airbnb Income for DSCR Qualification

This section matters more than people realize. The way a lender calculates your projected rental income determines your DSCR ratio, which determines your rate, your loan amount, and whether you get approved at all. Here are the four methods lenders use:

Method 1: AirDNA Market Projections

AirDNA is the industry standard for short-term rental income projections. Lenders pull an AirDNA report for the subject property’s address, which estimates annual revenue based on comparable vacation rentals in the area, seasonal occupancy patterns, and market demand.

The catch: lenders don’t use 100% of the AirDNA projection. They apply a discount factor, typically 75-90% of the projected income. So if AirDNA projects $72,000/year in gross revenue, the lender might credit $54,000-$64,800 for DSCR calculation purposes.

Why the haircut? Because projections are just that, projections. They don’t account for your specific property management skills, your pricing strategy, or the fact that your neighbor just listed an identical house at a lower nightly rate.

Method 2: Actual 12-24 Month Booking History

If you’re buying a property that’s already operating as an Airbnb (or if you own it and are refinancing), lenders can use actual booking history from your Airbnb, VRBO, or Booking.com accounts. This carries more weight, they’ll credit 90-100% of actual documented short-term rental income.

You’ll need to provide platform screenshots, payout summaries, or exported CSV data showing 12-24 months of rental history. This is the strongest form of income documentation for DSCR qualification because it’s real money, not a forecast.

Method 3: CPA-Prepared Profit & Loss Statement

For operators who book through multiple platforms or take direct bookings (no platform intermediary), a CPA-prepared P&L statement covering 12+ months works with many lenders. The CPA verifies the income sources and net operating income. Lenders typically credit 80-90% of the documented income.

Method 4: 1007 Rent Schedule (Market Rent Estimates)

The traditional approach: an appraiser includes a “1007 rent schedule” with market rent estimates based on comparable long-term rentals. This is the most conservative method because it values the property as a long-term rental, ignoring the premium that short-term rentals command. Some lenders still require this as a floor, even if they’re also looking at AirDNA data.

For Airbnb investors, you want a lender who uses AirDNA or actual booking history. Not one who defaults to 1007 market rent estimates. The difference can make or break your DSCR ratio.

Income Discount Factors by Method

| Income Documentation Method | Discount Factor Applied | Best For |

|---|---|---|

| AirDNA projections (no history) | 75-90% of projected income | New purchases, no operating history |

| Actual booking history (12-24 months) | 90-100% of actual income | Refinances, properties with track record |

| Hybrid (projections + partial history) | 80-90% of blended figure | Properties with 6-12 months of data |

| CPA-prepared P&L | 80-90% of documented income | Multi-platform or direct-booking operators |

| 1007 rent schedule (market rents) | 100% of appraised market rent | Conservative lenders, long-term rental income baseline |

STR Operating Costs That Affect Your DSCR Ratio

Most first-time Airbnb buyers underestimate operating costs, and that miscalculation kills their DSCR ratio. Short-term rental properties carry substantially higher operating costs than long-term rental properties. Here’s what actually comes out of your gross revenue before the DSCR calculation:

| Expense Category | Percentage of Gross Revenue | Annual Range (on $60K gross) |

|---|---|---|

| Property management company | 8-12% | $4,800-$7,200 |

| Cleaning & turnover costs | 10-15% | $6,000-$9,000 |

| Platform fees (Airbnb, VRBO) | 6-16% | $3,600-$9,600 |

| STR-specific insurance | 3-6% | $1,800-$3,600 |

| Maintenance & supplies | 5-8% | $3,000-$4,800 |

| Utilities (if host-paid) | 4-7% | $2,400-$4,200 |

| Total operating costs | 36-64% | $21,600-$38,400 |

That $60,000 in gross revenue turns into $21,600-$38,400 in net operating income after expenses. If you’re self-managing (no property management company), you save that 8-12%. But you’re trading time for money. Most lenders calculate DSCR using gross revenue (before operating expenses), but some factor in a management expense even if you self-manage. Ask your lender which method they use.

This is why I always tell new investors to run the numbers conservatively. Overestimating your short-term rental income by even 15% can turn a comfortable 1.25x DSCR into a razor-thin 1.05x, and that difference means worse rates, higher fees, or outright denial.

DSCR Loans vs Other Loan Types for Airbnb Properties

DSCR isn’t the only way to finance an Airbnb. But for most investors scaling beyond their first property, it’s the best option. Here’s how every major financing vehicle stacks up:

DSCR Loan vs Conventional Mortgage

Conventional loans win on rate (0.5-1.5% cheaper) but lose on everything else for real estate investors. You need full personal income verification, tax returns, a clean debt-to-income ratio, and you’re capped at 10 financed properties. If you have a steady W-2 job and you’re buying your first or second investment property, conventional might work. Beyond that? DSCR is the only scalable path.

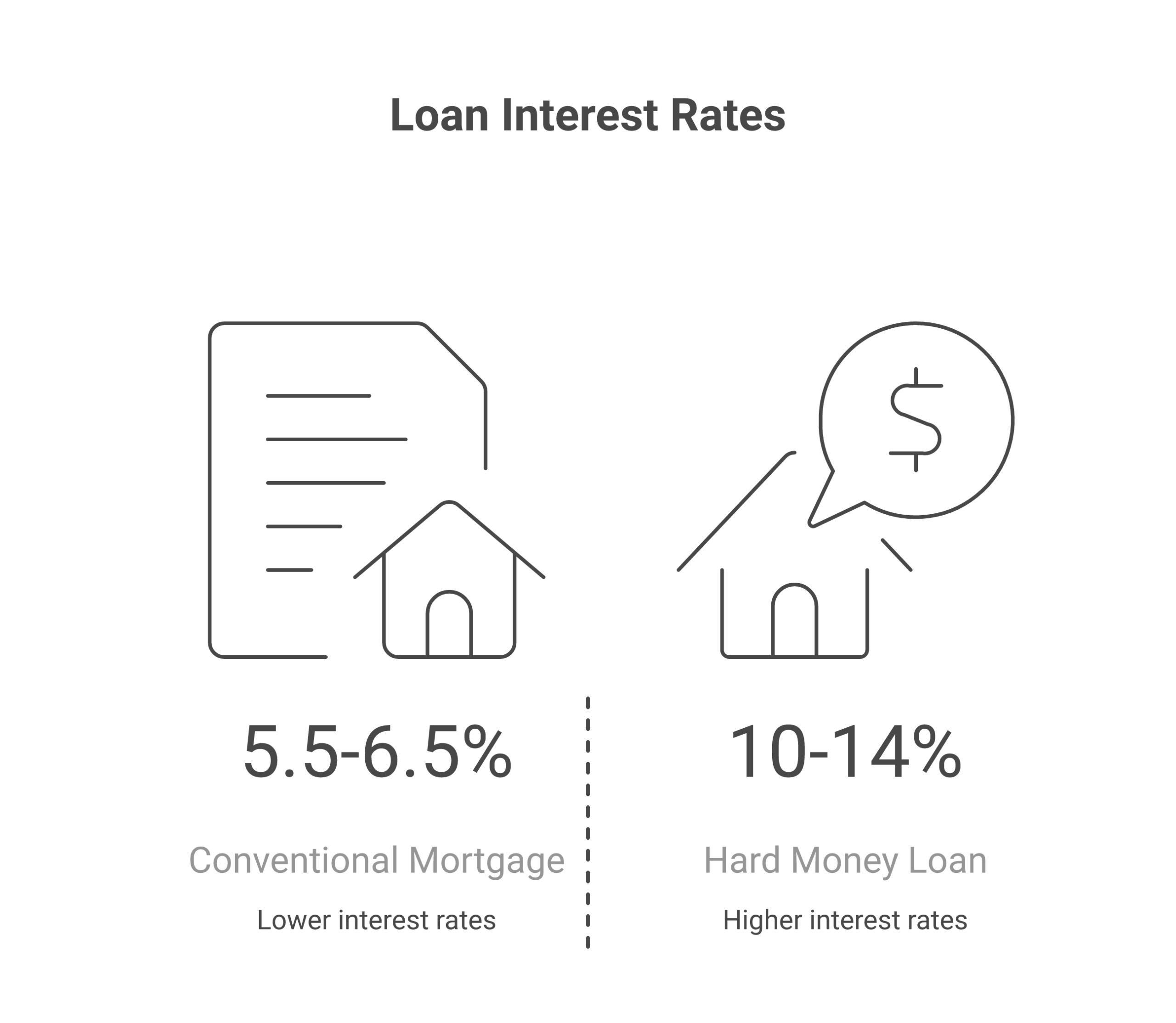

DSCR Loan vs Hard Money Loan

A hard money loan is a short-term, high-interest loan (typically 10-14% interest with 2-4 points in origination fees) designed for property flips or bridge financing. Terms are usually 12-24 months. Hard money makes sense for fix-and-flip projects where you’ll renovate and sell quickly. For a buy-and-hold Airbnb property that you plan to rent for years? Hard money interest rates will eat your cash flow alive. DSCR is the long-term hold vehicle.

| Feature | DSCR Loan | Hard Money Loan | Conventional | HELOC |

|---|---|---|---|---|

| Interest rate | 5.75-8.75% | 10-14% | 5.25-7.25% | 7-9% (variable) |

| Term | 30 years fixed | 12-24 months | 30 years fixed | 10-year draw |

| Down payment | 20-25% | 25-35% | 15-25% | Uses existing equity |

| Income docs | None | Minimal | Full | Full |

| Close in LLC | Yes | Yes | Usually no | No |

| Closing speed | 30-45 days | 7-14 days | 45-60 days | 30-45 days |

| Best for | Buy-and-hold STR | Fix-and-flip | First 1-2 properties | Down payment fund |

| Scalable | Unlimited properties | One at a time | Max 10 properties | Limited by equity |

DSCR Loan vs HELOC

A HELOC (Home Equity Line of Credit) lets you borrow against equity in a property you already own. Some arbitrage operators use a HELOC on their primary residence to fund the down payment on a DSCR-financed investment property. This is a legitimate strategy. But understand you’re putting your home on the line. Variable HELOC rates (currently 7-9%) plus a DSCR mortgage payment can create dangerous cash flow pressure if your short-term rental income drops.

The Hybrid Approach: HELOC for Down Payment + DSCR for the Purchase

One pattern I’ve seen work well for arbitrage operators: pull $50,000-$80,000 from a HELOC on your primary residence for the down payment, then finance the investment property with a DSCR loan. You’re stacking debt, so the numbers need to work. But if the property’s cash flow is strong enough to cover both the DSCR mortgage payment and help service the HELOC, it’s a fast way to get into ownership.

How Seasonal Income Affects DSCR Qualification for Vacation Rentals

This trips up a lot of Airbnb investors. Short-term rental income isn’t flat. It’s seasonal. A beach house might gross $12,000/month in summer and $2,000/month in winter. A ski cabin does the opposite. Market demand drives everything.

Lenders annualize the income, which smooths out the seasonality. They take your projected annual revenue (or your actual 12-month booking history) and divide by 12 to get a monthly figure. Strong peak-season months offset weaker months in the calculation.

But here’s what catches people: your monthly mortgage payment stays the same year-round. In slow months, you might be dipping into reserves to cover the mortgage loan even though the annual DSCR looks healthy. Budget accordingly. Those 9-12 months of required reserves? They exist specifically for this reason.

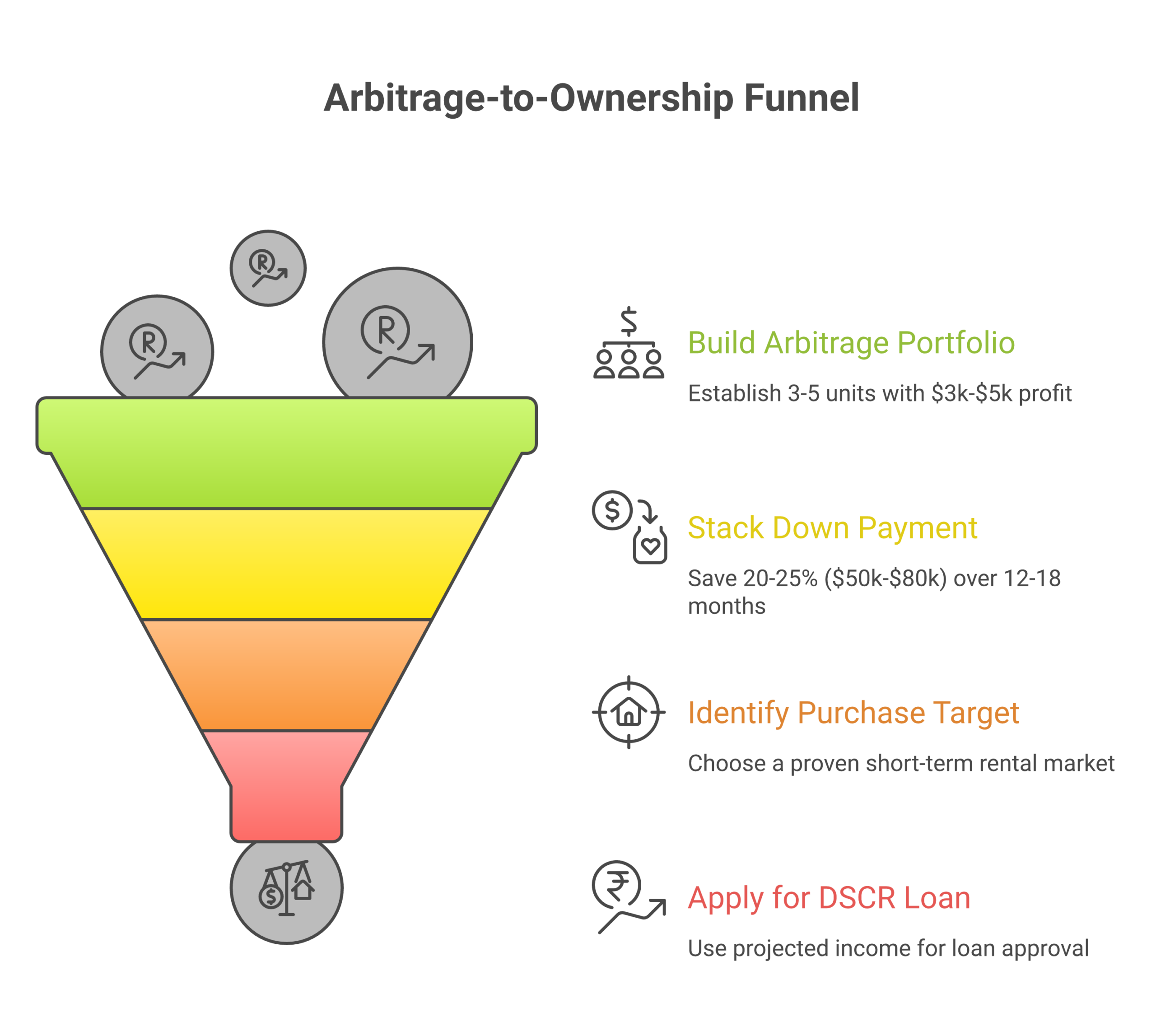

The Arbitrage-to-Ownership Playbook

This is the roadmap I’d follow if I were going from rental arbitrage to owning short-term rental properties with DSCR financing. Five steps. No shortcuts.

Step 1: Build Your Arbitrage Portfolio First

Before you even think about buying, build a profitable rental arbitrage operation with 3-5 units generating $3,000-$5,000/month in net profit. This does three things: it proves you can operate a short-term rental profitably, it generates the cash flow you’ll need for a down payment, and it gives you market knowledge that makes you a smarter buyer.

Don’t rush this step. Most failed purchases trace back to operators who tried to buy before they’d proven the business model.

Step 2: Stack Your Down Payment From Arbitrage Profits

A 20-25% down payment on a $300,000-$400,000 property is $60,000-$100,000. Plus 9-12 months of reserves ($31,500-$42,000 on a $3,500/month PITIA). Plus closing costs (2-5% of the loan amount). You’re looking at $100,000-$160,000 in total cash needed.

At $4,000/month net arbitrage profit, that’s 25-40 months of saving everything. Tight? Yes. But this is exactly what separates the operators who build wealth from the ones who stay stuck. Arbitrage is the cash machine. Ownership is the wealth machine.

Curious what your arbitrage operation could realistically generate? The Airbnb profit calculator can help you model different scenarios.

Step 3: Identify Your Purchase Target in a Proven Market

Buy in a market you already know, ideally one where you’re already running arbitrage. You understand the seasonality, the guest demographics, the pricing dynamics, and the local regulations. This market knowledge is your unfair advantage over out-of-state investors who are relying entirely on AirDNA data.

Check the best cities for Airbnb arbitrage for markets with strong fundamentals for short-term rental investing.

Step 4: Apply for DSCR Loan Using Projected or Actual STR Income

Get your documentation ready before you apply:

- AirDNA report for the target property (or comparable properties in the area)

- Your Airbnb/VRBO booking history from your existing arbitrage units (proves operational competence)

- 6-12 months of bank statements showing reserves

- LLC formation documents (if closing in an LLC)

- Property insurance quote (STR-specific policy)

Shop at least 3 DSCR lenders. Rates, terms, and discount factors vary significantly between lenders. The difference between a 6.25% and a 7.25% rate on a $280,000 loan is about $200/month, or $2,400/year, for 30 years. That’s $72,000 over the life of the loan. Shopping matters.

Step 5: Run Arbitrage and Owned Properties Simultaneously

Don’t drop your arbitrage units when you buy. Run both. Your arbitrage cash flow covers your living expenses and builds reserves for the next purchase. Your owned property builds equity and long-term wealth. This dual-track approach is how you go from one property to a real portfolio of multiple properties.

A Real-World Example With Numbers

Let’s walk through a realistic scenario for an arbitrage operator making the jump:

- Current situation: 4 arbitrage units netting $4,500/month after all expenses

- Purchase target: $350,000 single-family home in a market you already operate in

- Down payment (25%): $87,500

- Loan amount: $262,500

- DSCR loan rate: 6.5% (30-year fixed)

- Monthly PITIA: $2,450 (principal + interest + taxes + insurance)

- Projected monthly rental income: $4,200 (from AirDNA, lender credits 80% = $3,360)

- DSCR ratio: $3,360 / $2,450 = 1.37x, comfortably above the 1.25x threshold

- Monthly cash flow (after PITIA): $1,750 using full projected income

- Annual equity buildup: ~$4,800 in principal paydown (year 1)

Add that to your $4,500/month arbitrage income, and you’re now generating $6,250/month, with an asset that appreciates over time. That’s the math that makes DSCR loans transformational for real estate investors.

Short-Term Rental DSCR vs Long-Term Rental DSCR: Key Differences

If you’ve looked at DSCR loans for long-term rentals, know that the STR version has some important differences:

| Factor | STR DSCR (Airbnb/VRBO) | LTR DSCR (Long-Term Lease) |

|---|---|---|

| Income source | Airbnb/VRBO revenue or AirDNA projections | Signed lease or appraisal market rents |

| Income stability | Variable, seasonal | Fixed for lease term |

| Operating history required | 0-24 months (varies by lender) | None |

| Reserve requirements | 9-12 months PITIA | 6 months PITIA |

| Income discount factor | 75-100% depending on documentation | Usually 100% of lease amount |

| Interest rate premium | Slight premium over LTR DSCR | Standard DSCR pricing |

| Lender availability | Growing (100+ STR-specific programs in 2026) | Widely available (200+ lenders) |

| Revenue potential | 2-3x higher than LTR in strong markets | Stable, predictable, lower |

The STR DSCR market has grown fast. According to industry data, vacation rental properties financed through DSCR programs grew by over 40% between 2024 and 2025. By 2026, over 100 wholesale lenders offer STR-specific DSCR products. The market is maturing, and that means more competition between lenders, which benefits borrowers.

Top DSCR Lenders for Short-Term Rentals in 2026

I’m not going to name specific lenders because the landscape changes quarterly and my recommendation today might be stale by the time you read this. Instead, here’s what to look for and the types of DSCR lenders you’ll encounter:

Types of DSCR Lenders

- Non-QM specialty lenders – companies that focus exclusively on investment property loans. They understand STR income and typically offer the most competitive DSCR terms

- Portfolio lenders – banks and credit unions that keep loans on their own books. More flexibility in underwriting, but may have geographic restrictions

- Wholesale mortgage brokers – brokers who shop your deal across 100+ lenders. A good wholesale broker can compare STR-specific DSCR pricing across dozens of programs in a single submission. This is often the fastest path to the best rate

- Hard money lenders transitioning to DSCR – some hard money lenders now offer 30-year DSCR products alongside their short-term loans. Quality varies widely

What to Look for in a DSCR Lender

- Experience with short-term rental properties (not just traditional rentals)

- Acceptance of AirDNA data for projected income (not just 1007 rent schedule or market rent estimates)

- LLC closing capability

- Transparent prepayment penalty terms

- Clear explanation of how they calculate the maximum loan amount based on your property’s revenue

- Competitive rate lock policies (DSCR rates can move daily)

Questions to Ask Before Applying

- What’s your minimum DSCR ratio for short-term rental properties?

- What income documentation do you accept, AirDNA, booking history, or 1007 only?

- What discount factor do you apply to projected rental income?

- What’s the minimum credit score and how do credit tiers affect pricing?

- Can I close in my LLC?

- What are the prepayment penalty terms?

- What reserve requirements do you have for STR properties?

- What’s the maximum loan amount you’ll approve for this property type?

5 Strategies to Maximize Your DSCR Ratio

If your DSCR ratio is borderline (between 0.95x and 1.20x), these strategies can push you over the threshold or into a better pricing tier:

- Increase the down payment. More cash down = smaller loan = lower monthly payment = higher DSCR. Going from 20% to 25% down on a $350,000 property reduces your loan by $17,500 and your monthly mortgage payment by roughly $110-120.

- Buy in a higher-revenue market. Not all markets generate enough rental income to support a DSCR ratio above 1.0x. Markets with strong tourism, business travel, or event-driven demand produce higher nightly rates and occupancy. Do your homework with AirDNA before committing.

- Optimize your property listing before applying. If you’re refinancing and using actual booking history, maximize your revenue in the 3-6 months before application. Professional photos, dynamic pricing, optimized listing copy, all of this flows directly into your DSCR calculation.

- Choose the right income documentation method. If you have 12+ months of strong booking history, use actual income (90-100% credit) rather than AirDNA projections (75-90% credit). The difference can move your DSCR by 0.10-0.25x.

- Shop for properties with lower carrying costs. A property in a low-tax, low-insurance area with no HOA will have a lower PITIA than the same property in a high-tax state with a mandatory HOA. Lower PITIA = higher DSCR on the same revenue.

Short-Term Rental Financing Beyond DSCR: Emerging Options

The short-term rental financing market is evolving fast. A few newer options worth knowing about:

Hybrid STR Mortgage Loans

Some lenders now offer hybrid products that combine conventional mortgage underwriting with DSCR elements. You can qualify using both personal income and verified rental performance, giving you access to higher use, better rates, and smoother underwriting. These work well for investors who could qualify conventionally but want to factor in their STR income to increase their maximum loan amount.

Portfolio Lines of Credit

For investors with multiple properties, some lenders offer portfolio-level financing, a single line of credit or blanket loan secured by multiple rental properties. This simplifies management and can offer better terms than individual DSCR loans on each property.

Seller Financing with DSCR Refinance

A creative strategy: negotiate seller financing on the initial purchase (no bank involved), operate the property for 12-24 months to build booking history, then refinance into a DSCR loan using actual income data. This gives you the strongest possible DSCR application because you have documented cash flow, not just projections.

Common Mistakes With DSCR Loans for Airbnb

I’ve seen every version of these mistakes. Learn from other people’s money.

1. Not Shopping Multiple Lenders

DSCR loan rates, terms, and qualification criteria vary dramatically between lenders. I’ve seen the same borrower quoted 6.25% by one lender and 7.75% by another for the same property. On a $280,000 loan, that 1.5% spread is $350+/month. Always get at least 3 quotes.

2. Overestimating Short-Term Rental Income

The single most common mistake. Investors look at top-performing Airbnb listings in their target market and assume they’ll match those numbers. Reality check: those listings have hundreds of reviews, professional photography, and years of optimization. Your year-one revenue will be 15-25% below the market leaders. Run your numbers at 75-80% of AirDNA projections and see if the deal still works.

3. Forgetting About Reserves Post-Closing

The down payment and closing costs wipe out your savings, and now you have zero reserves. First slow month, you’re sweating the mortgage loan payment. Build your reserves BEFORE closing and don’t touch them. Those 9-12 months of PITIA reserves aren’t just a lender requirement. They’re your survival fund.

4. Ignoring Prepayment Penalties

You buy at 7.0% thinking you’ll refinance when rates drop. Then you discover there’s a 3% prepayment penalty that costs $8,400 on your $280,000 loan. That eats most of your refinancing savings. Understand the prepayment structure before signing.

5. Buying in an STR-Restricted Market

Some cities have banned or severely restricted short-term vacation rentals. Others are moving in that direction. If your city passes a ban after you buy, your “Airbnb income” evaporates, and your DSCR ratio goes to zero. Research local regulations thoroughly before committing.

6. Not Getting a Proper STR Appraisal

A standard residential appraisal values the property based on comparable sales. Not its income potential as a short-term rental. Some lenders require an “income approach” appraisal that factors in STR revenue. If your lender uses a standard appraisal and your DSCR ratio is borderline, ask about an income-approach alternative.

7. Treating the DSCR Ratio as the Only Number That Matters

A 1.5x DSCR looks great on paper. But if your property cash flow depends on 85% occupancy in a seasonal market, one bad quarter can drop you well below 1.0x in reality, even though the annual number looks healthy. Look at the monthly cash flow projections, not just the annual ratio.

Tax Implications of DSCR-Financed Airbnb Properties

DSCR loans don’t change the tax treatment of your investment property. But owning (versus arbitraging) changes your tax picture significantly. Here’s what matters:

- Mortgage interest deduction: The interest on your DSCR loan is deductible as a business expense on Schedule E. On a $262,500 loan at 6.5%, that’s roughly $17,000 in deductible interest in year one alone

- Depreciation: You can depreciate the property (not land) over 27.5 years for residential rental. On a $350,000 property where the building is worth $280,000, that’s roughly $10,182/year in depreciation deductions, a non-cash expense that reduces your taxable income

- Operating expense deductions: Cleaning, maintenance, supplies, property management company fees, platform fees, insurance, utilities, and repairs are all deductible

- Cost segregation: An advanced strategy where a specialist accelerates depreciation by identifying building components that can be depreciated over 5, 7, or 15 years instead of 27.5. This can generate massive first-year deductions

For a deep dive on Airbnb tax strategy, check the complete Airbnb tax guide. And if you haven’t already, get an Airbnb business plan together that accounts for these deductions in your financial projections.

Frequently Asked Questions About DSCR Loans for Airbnb

What credit score do I need for a DSCR loan?

Most DSCR lenders require a minimum credit score of 660-680. You can find programs at 620, but rates will be 1.5-2.0% higher. For the best rates and terms, target 720+. The difference between a 660 and a 740 credit score can be $200-300/month on a typical DSCR loan.

Can I use a DSCR loan for my first investment property?

Yes. DSCR loans don’t require prior real estate investment experience, though some lenders prefer borrowers who can demonstrate operational knowledge. Having arbitrage experience, even without property ownership, is a strong signal to lenders that you know how to run a profitable short-term rental.

How long does it take to close a DSCR loan?

Typical closing timeline is 30-45 days from application to funding. Some lenders can close in 21-25 days if all documentation is ready upfront. Conventional mortgages take 45-60 days by comparison.

Do I need a property management company to qualify for a DSCR loan?

No. You can self-manage. However, some lenders may factor in a 8-12% management expense when calculating your DSCR ratio regardless of whether you use a property management company. This is a conservative underwriting approach, ask your lender whether they deduct management fees from the projected income calculation.

Can I use DSCR loan proceeds to buy a property and then rent it on Airbnb?

Yes, that’s exactly what DSCR loans for Airbnb are designed for. You’re buying an investment property with the intent to generate short-term rental income. The lender underwrites the deal based on the property’s projected or actual income from vacation rentals.

What happens if my Airbnb income drops below the DSCR threshold after closing?

Nothing happens to your loan, DSCR is a qualification metric at origination, not an ongoing covenant. Your monthly mortgage payment stays the same regardless of whether your rental income covers it. However, if you can’t cover the payment from cash flow, you’ll need to draw from reserves or your arbitrage income. That’s why reserves and enough rental income buffer matter.

Can I refinance a DSCR loan later?

Yes. DSCR-to-DSCR refinances are common, especially when rates drop or your property’s revenue increases (improving the ratio). Watch for prepayment penalties. Most DSCR loans have them for the first 3-5 years. Factor that cost into your refinance math.

Are DSCR loan interest rates tax deductible?

Yes. Mortgage interest on a DSCR loan for an investment property is deductible as a business expense, just like any other rental mortgage. Consult your CPA for specifics based on your tax situation and entity structure.

How many DSCR loans can I have at the same time?

There’s no universal cap. Many seasoned real estate investors carry 10, 15, or 20+ DSCR loans simultaneously. Each property is underwritten independently. As long as each property’s debt service coverage ratio qualifies on its own merits, you can keep buying multiple properties without hitting the financing wall that conventional mortgages create.

What’s the maximum loan amount for a DSCR Airbnb loan?

Maximum loan amounts vary by lender, typically ranging from $1 million to $3 million per property. Some specialty lenders go higher for luxury vacation rentals. The maximum loan is determined by the purchase price, your down payment, and the property’s DSCR qualification. Not your personal income.

How much do Airbnb hosts actually make?

Revenue varies enormously by market, property type, and management quality. For realistic numbers across different markets, check out how much Airbnb hosts actually make – it breaks down income by city and property size with real data.

The Bottom Line: DSCR Is How Arbitrage Operators Become Property Owners

DSCR loans exist to solve one problem: how do real estate investors who don’t have conventional income documentation buy rental properties based on the property’s income potential? For Airbnb operators, especially those transitioning from rental arbitrage to ownership, they’re the single most important financing tool available.

The math is straightforward. If the property earns enough rental income to cover its own monthly mortgage payment with room to spare, you qualify. No W-2s. No tax returns. No personal income verification. No cap on the number of properties you can own.

Rates in early 2026 sit in the 5.75-7.25% range for well-qualified borrowers, competitive by historical standards and significantly better than where they were 18-24 months ago. The STR DSCR lending market has grown over 40% since 2024, meaning more lenders competing for your business, which pushes rates down and terms up.

If you’re running profitable short-term rental arbitrage and you’ve been waiting for the right moment to make the jump to ownership, here’s what to do:

- Get your credit score above 700 (ideally 720+)

- Save 20-25% for a down payment plus 9-12 months of reserves

- Document your arbitrage income and operations

- Shop 3+ DSCR lenders, rates vary by 1-2% for the same deal

- Buy in a market you know from your arbitrage experience

- Run the numbers conservatively at 75-80% of AirDNA projections

- Make the move

Arbitrage builds skills and cash flow. DSCR loans turn that cash flow into property ownership. Ownership builds real, generational wealth. That’s the progression from zero to a real short-term rental portfolio.

Disclaimer: Interest rates, loan terms, and lender requirements referenced in this article are estimates based on February 2026 market conditions and are subject to change. DSCR loan availability varies by lender and state. This article is for educational purposes and does not constitute financial or lending advice. Always consult with a licensed mortgage professional and financial advisor before making financing decisions.