You can start an Airbnb business with no money, or damn close to it. I’ve watched hundreds of students build profitable rental arbitrage portfolios without owning property, draining savings, or begging a bank for a large down payment. The short term rental market doesn’t care about your net worth. It cares about hustle, market knowledge, and execution speed.

Whether you have $0 or $5,000, there’s a proven path into the vacation rental industry that matches your situation right now. Rental arbitrage, co-hosting, house hacking, seller financing, home equity loans. Each method has different startup costs, risk profiles, and income ceilings. Some generate $2,000–$8,000 per month per unit. Others start smaller but compound fast. I’m going to break down every method that actually works in 2026, show you the real numbers, and tell you which one to pick based on where you’re starting from.

What Does “Start Airbnb With No Money” Actually Mean?

Let me be real with you. “No money” doesn’t always mean literally zero dollars. It means you don’t need to buy an investment property outright, save up a massive down payment, or take on crippling debt to get your first unit live on Airbnb. Most people assume you need $50,000–$100,000 in upfront capital to enter the short term rental market. That assumption is wrong.

The strategies I’m covering let you start an Airbnb business with little or no money by using other people’s properties, creative financing structures, or assets you already own. Some methods, like co-hosting and Airbnb Experiences, genuinely cost $0. Others, like the Airbnb rental arbitrage route, require $2,000–$5,000 for furnishing a leased unit. But compared to buying a rental property with a traditional 20% down payment on a $300,000 home ($60,000 plus closing costs), these alternatives look practically free.

Here’s how each method stacks up:

| Method | Startup Cost | Monthly Profit Potential | Owning Property Required? | Time to First Booking |

|---|---|---|---|---|

| Rental Arbitrage | $2,000–$5,000 | $1,000–$8,000/unit | No | 30-60 days |

| Co-Hosting | $0 | $500–$3,000 | No | 14-30 days |

| House Hacking | 3.5% down (FHA) | $500–$2,500 | Yes (you live there) | 60-90 days |

| Seller Financing | $0–$5,000 | $1,000–$5,000 | Yes (negotiate terms) | 30-90 days |

| HELOC / Cash-Out Refi | $0 out of pocket | $1,000–$4,000 | Yes (existing home) | 30-60 days |

| Airbnb Experiences | $0 | $500–$2,000 | No | 7-14 days |

| Property Management | $0 | $1,000–$5,000 | No | 14-30 days |

Method 1: Airbnb Rental Arbitrage (The Fastest Path Without Owning Property)

Rental arbitrage is the most popular way to start an Airbnb business without owning property, and I recommend it to most people because the economics are simple to understand and the barrier to entry is low. You sign a long-term lease on an apartment or house, get the property owner’s written permission to sublet, furnish it, then list it on Airbnb at a nightly rate that exceeds your monthly rent. The spread is your profit.

Here’s what the real numbers look like. Say you lease a two-bedroom apartment in a mid-size city for $1,500 per month. You furnish it for $3,000 using Facebook Marketplace and budget retailers. If you charge $130 per night and maintain 70% occupancy, your gross monthly revenue hits $2,730. After rent ($1,500), utilities ($150), cleaning ($200), supplies ($80), and Airbnb’s host fee (3% of revenue = $82), you’re clearing roughly $718 per month from one unit. Scale to three units and that’s $2,150 per month, a meaningful income stream that didn’t require a single dollar of investor capital or a large down payment on a property.

But here’s where it gets interesting. Operators in high-demand markets like Nashville, Scottsdale, and Savannah regularly clear $3,000–$8,000 per month per unit on well-located properties near tourist attractions, event venues, or downtowns. The key variables that separate a $700/month unit from a $5,000/month unit:

- Market selection – Target cities where short term rental nightly rates are 2-3x monthly rent. This is non-negotiable. A $1,500/month apartment that rents for $80/night on Airbnb won’t work. You need markets where that same apartment commands $120–$180/night

- Landlord negotiation – You need written permission to sublet. Frame it to the property owner as a win: guaranteed occupancy, higher maintenance standards, and a tenant who treats the airbnb property like a business asset

- Furnishing strategy – Start lean. A clean, well-photographed space with solid fundamentals (comfortable bed, quality towels, coffee maker, fast WiFi) consistently outperforms expensive but poorly staged units

- Dynamic pricing – Tools like PriceLabs or Wheelhouse adjust your rates based on local demand, events, and seasonality. Static pricing leaves money on the table during peak periods and leads to empty calendars during slow weeks

The biggest misconception about the Airbnb rental arbitrage route is that it requires significant upfront capital. It doesn’t. Some landlords accept first month’s rent plus security deposit, $3,000–$4,500 total. If you furnish strategically (buy used, negotiate bulk deals, skip non-essentials), your total out-of-pocket can land under $5,000. I’ve seen students start with less than $2,800 by finding move-in specials and sourcing furniture from estate sales.

One thing you need to understand about rental arbitrage: your lease is your biggest expense and your biggest risk. If occupancy drops or local regulations change, you’re still on the hook for rent payments. Always have a reserve fund equal to two months’ rent before going live. That’s not optional.

Method 2: Co-Hosting and Property Management ($0 Startup)

If you literally have zero dollars to invest, co-hosting is your entry point into the Airbnb business. You manage someone else’s Airbnb property, handling guest communication, pricing, cleaning coordination, and reviews, in exchange for 10-25% of booking revenue. The property owner keeps their listing. You do the work. No lease, no furnishing, no financial risk.

Property management takes this a step further. Instead of just co-hosting a single listing, you build a portfolio of properties you manage for multiple owners. Some operators manage 10-50+ units earning $1,000–$5,000 per month without owning a single one. The property owner benefits because they don’t want to deal with guest messages at 11 PM or coordinate turnovers. You benefit because you build operational experience and a consistent income stream with zero capital at risk.

How to find co-hosting clients:

- Facebook groups – Search for local Airbnb host groups. Property owners regularly post looking for management help

- Direct outreach – Message Airbnb hosts in your area whose listings have poor reviews or inconsistent availability. They’re struggling and likely open to help

- Real estate investor meetups – Real estate investors who own a vacant property or underperforming rentals often want passive income without the hands-on work

- Airbnb’s co-host marketplace – Airbnb now has a built-in co-host matching system that connects property owners with experienced managers

The strategic play here: use co-hosting as a stepping stone. Learn the business on someone else’s dime, build reviews and a track record, then transition to rental arbitrage or purchasing your own investment property once you’ve saved enough from management fees. Many of our most successful students started exactly this way.

Method 3: House Hacking Your Primary Residence

House hacking is the best way to start an Airbnb business when you want to eventually own property but can’t stomach a traditional 20% down payment. The concept: buy a home you live in, then rent part of it on Airbnb to cover your monthly mortgage payments, or even generate positive cash flow on top.

Here’s why this works financially. An FHA loan lets you buy a primary residence with as little as 3.5% down if your credit score is 580 or above. On a $250,000 duplex, that’s $8,750 down plus closing costs (typically 2-5% of the purchase price). You live in one unit and list the other on Airbnb. If the second unit generates $1,800/month in rental income and your total monthly mortgage payments (principal, interest, taxes, insurance) are $1,900, you’re essentially living rent-free while building equity.

The numbers get even better with a triplex or fourplex. FHA loans cover up to four-unit properties as long as you occupy one unit as your primary residence for at least 12 months. A fourplex where three units generate short term rental income can produce a meaningful income stream that covers all your housing costs and puts cash in your pocket.

Key considerations for house hacking:

- FHA loan limitations – FHA rules technically prohibit rentals shorter than 30 days in some interpretations. Many house hackers use conventional loans (minimum 5% down) to avoid this gray area, or list on platforms with 30+ day minimums initially

- Location matters more than price – A $200,000 duplex in a tourist-friendly neighborhood outperforms a $350,000 duplex in a suburb with no visitor demand. Research the short term rental market in your target area before you buy

- Living on-site is an advantage – You can handle turnovers personally, respond to guest issues immediately, and maintain the property without hiring help. That saves 20-30% on management costs

- Tax benefits stack up – Mortgage interest, property taxes, depreciation, and operating expenses on the rented portion are deductible. Talk to a CPA who understands short-term rental taxation

Method 4: Seller Financing (Skip the Bank Entirely)

Seller financing is one of the most underused strategies in the vacation rental industry, and one of the most powerful for people who can’t qualify for traditional bank loans. Instead of getting a mortgage from a lender, the property owner acts as your bank. You negotiate monthly payments directly with the seller, who holds the note on the property until you pay it off or refinance.

Why would a seller agree to this? Several reasons. They want to sell quickly. They want to defer capital gains taxes (installment sale). The property has been sitting on the market. Or they’re retiring and want a predictable income stream from the monthly payments without the hassle of being a landlord.

Typical seller financing terms:

- Down payment – Negotiable, often 5-10% of market value (compared to 15-25% for a conventional investment property loan). Some motivated sellers accept 0% down if you demonstrate strong cash flow potential

- Interest rate – Usually 5-9%, slightly above conventional rates but without the credit score requirements, income verification, or closing costs of a bank loan. You pay interest to the seller monthly instead of a bank

- Loan term – Typically 3-7 years with a balloon payment, giving you time to build equity and then refinance with a traditional lender at a better interest rate

- No bank qualification – This is the biggest advantage. No W-2 requirements, no debt-to-income ratio scrutiny, no two-year employment history. The deal lives or dies based on your negotiation skills and the property’s income potential

Where to find seller financing deals: look for “for sale by owner” listings, properties that have been on the market 90+ days, estate sales, and landlords tired of managing their own vacant property. These property owners are motivated and often open to creative deal structures that a bank would never approve.

Method 5: Cash Out Refinance and Home Equity Loans

If you already own a home, even your primary residence, you’re sitting on a potential goldmine of upfront capital that can fund your Airbnb business without spending a dollar from your savings account. Two strategies make this possible: a cash out refinance and home equity loans (or a HELOC).

Cash out refinance: You replace your existing mortgage with a new, larger mortgage and pocket the difference in cash. If your home is worth $350,000 and you owe $200,000, you might refinance for $280,000 at a 6.5% interest rate and take $80,000 in cash. That’s enough to buy an Airbnb property outright in some markets, or fund the down payment and furnishing for a rental arbitrage portfolio of 8-10 units.

Home equity loans and HELOCs: A home equity loan gives you a lump sum secured against your home’s equity. A HELOC (Home Equity Line of Credit) works like a credit card. You draw on it as needed. Both typically carry interest rates of 7-9% in 2026 and require a credit score of 680+ for the best terms. The key advantage: you only pay interest on what you use, and the interest may be tax-deductible if the funds are used for investment purposes.

The risk with both approaches: you’re putting your primary residence on the line. If the Airbnb income doesn’t cover the new monthly payments, you’re in trouble. Run conservative projections, assume 50% occupancy, not 80%, before pulling equity from your home. I’ve seen real estate investors get burned by overleveraging during seasonal slowdowns.

Method 6: DSCR Loans for Airbnb Investment Properties

DSCR (Debt Service Coverage Ratio) loans are purpose-built for real estate investors who want to buy an Airbnb property based on its rental income potential. Not their personal income. If you’re self-employed, have irregular income, or just don’t want to show tax returns, DSCR loans are your best option for acquiring an investment property.

How DSCR loans work: the lender evaluates whether the property’s projected rental income covers the monthly mortgage payments. They calculate a ratio by dividing monthly rental income by total monthly debt (principal, interest, taxes, insurance). A DSCR of 1.25 means the property generates 25% more income than the debt payments require. Most lenders want a minimum DSCR between 1.0 and 1.25.

Current DSCR loan terms in 2026:

| Factor | Typical Range |

|---|---|

| Down payment | 15-25% of market value |

| Interest rate | 6.1-8% (30-year fixed) |

| Credit score minimum | 620 (680+ for best rates) |

| Income documentation | None (property income only) |

| Cash reserves required | 6-12 months PITI |

| Income verification source | AirDNA projections or actual rental history |

Here’s the “no money” angle with DSCR loans: combine a DSCR loan with equity pulled from a cash out refinance or home equity loan on your primary residence. You use the equity for the down payment, and the property’s rental income covers the DSCR loan payments. Your out-of-pocket? Potentially zero, though you’re still taking on debt secured by your assets.

Over 100 wholesale lenders now offer STR-specific DSCR programs, making this the most accessible institutional financing option for Airbnb investors who can’t or won’t qualify through traditional channels.

Method 7: Airbnb Experiences and Low-Cost Entry Points

Not every Airbnb business involves renting a property. Airbnb Experiences let you sell guided tours, cooking classes, photography walks, or adventure activities to travelers. No property required. Startup cost: $0. You’re selling your time, knowledge, and local expertise.

I know an operator in Austin who runs a “Hidden Taco Trail” walking tour that generates $3,200/month working only weekends. Another in Asheville leads a foraging and wild cooking experience earning $1,800/month. The margins are nearly 100% because there’s no rent, no furnishing, no utilities.

Other $0–$500 entry points:

- Rent out a spare room – If you already own or rent a home, listing a vacant room on Airbnb is the simplest path. You might clear $800–$2,000/month depending on your city. This is classic house hacking without needing a new mortgage

- Airbnb virtual assistant – Property managers need help with guest messaging, pricing adjustments, and listing optimization. Pay ranges from $15–$30/hour, and you can manage multiple hosts remotely

- Cleaning service – Airbnb turnovers are a recurring need. Start a cleaning business focused on short-term rentals with $500 in supplies. Charge $75–$150 per turnover and you can build a solid income stream while networking with property owners who might later need management

Creative Financing: Raising Investor Capital Without Banks

Banks aren’t the only source of funding. Many successful Airbnb operators fund their first properties with investor capital from friends, family, or private investors who want passive exposure to the short term rental market without doing the work themselves.

How the deal structure typically works:

- Find the deal – You identify a property with strong Airbnb potential. Run the numbers. Build projections showing monthly cash flow, occupancy assumptions, and annual returns

- Create a business plan – Document the market analysis, comparable listings, revenue projections, expense breakdown, and your management strategy. Use our Airbnb business plan template as a starting point

- Pitch the investor – Present the deal to someone with capital. Offer them a preferred return (8-12% annually) plus a share of profits above that threshold. They put up the money. You do all the work

- Structure the entity – Form an LLC with an operating agreement that spells out capital contributions, profit splits, management responsibilities, and exit terms

Common profit-split structures in the vacation rental industry:

- 70/30 split – Investor gets 70% of profits (they put up all the capital). You get 30% plus a management fee

- 50/50 split – More common when you’re bringing significant operational value, an existing portfolio, or the deal itself

- Preferred return + equity kicker – Investor gets 8-10% return first, then remaining profits split 50/50. This is the most investor-friendly structure and easiest to raise capital with

The benefit of using investor capital: zero personal debt, zero monthly payments from your pocket, and zero credit risk. The downside: you give up a chunk of profits and answer to someone else. For someone starting with no money, that trade-off is usually worth it.

Understanding the Real Costs of Starting an Airbnb Business

Even when starting an Airbnb with no money, or close to it, you need to understand what expenses exist so you’re not caught off guard. Here’s an honest breakdown for someone using the rental arbitrage method:

Upfront Costs (Rental Arbitrage)

| Expense Category | Budget Range | Notes |

|---|---|---|

| Security deposit + first month | $2,000–$3,500 | Some landlords negotiate waived deposits |

| Furnishing | $1,500–$4,000 | Buy used on FB Marketplace, estate sales |

| Photography | $100–$300 | Professional photos convert 40% better |

| Supplies and essentials | $200–$500 | Linens, toiletries, kitchen basics, lockbox |

| LLC formation | $50–$500 | Varies by state |

| Total estimated | $3,850–$8,800 | Lean operators: under $4,000 |

Monthly Recurring Costs

- Rent – Your biggest line item. This is your existing mortgage equivalent for arbitrage operators

- Utilities – $100–$250/month depending on unit size and season

- Cleaning – $60–$150 per turnover (factor 8-15 turnovers/month at 70% occupancy)

- Supplies restocking – $50–$100/month for toiletries, coffee, paper goods

- Software – Dynamic pricing tools ($20–$50/month), channel manager ($10–$30/month)

- Insurance – STR-specific insurance runs $100–$250/month. Don’t skip this

- Airbnb host fee – 3% of booking subtotal

Use the Airbnb profit calculator to model your specific numbers before signing any lease. I can’t stress this enough, run the projections twice, assume 50% occupancy for your first two months, and verify that the property still cash flows at that conservative level.

Step-by-Step: From $0 to Your First Airbnb Booking

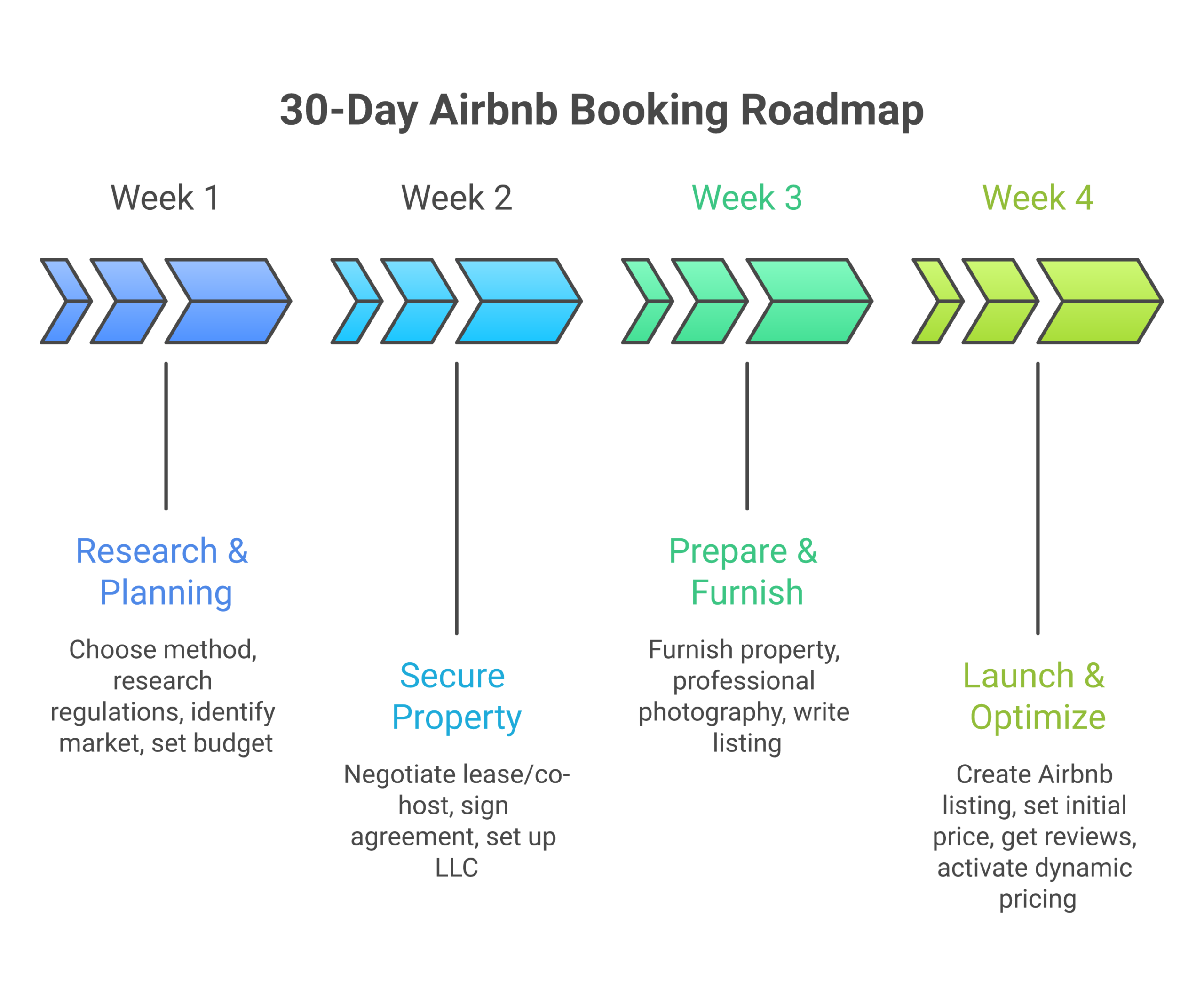

Regardless of which method you choose, here’s the tactical step-by-step to go from nothing to your first booking:

Week 1: Research and Market Selection

- Choose your method – Based on the table above, pick the strategy that matches your capital situation. Zero dollars? Start with co-hosting. Under $5,000? Rental arbitrage. Own a home? House hacking or cash out refinance

- Research local STR regulations – Check your city’s short-term rental ordinances. Some cities require permits, limit the number of rental days, or restrict STRs to certain zones. This step is non-negotiable, getting shut down after you’ve invested kills everything

- Analyze your target market – Use AirDNA or Mashvisor to check average nightly rates, occupancy rates, and revenue potential in your target area. You want markets where the average Airbnb property generates at least 2x the monthly rent in gross revenue

- Set financial targets – Define your monthly income goal. Then work backward: how many units, at what occupancy, at what nightly rate gets you there?

Week 2: Secure Your Property or Client

- For arbitrage – Contact landlords, schedule viewings, negotiate lease terms with subletting permission. Have your business plan ready to show them

- For co-hosting – Reach out to 20+ Airbnb hosts in your area. Offer a free trial month of management. Convert 2-3 into paying clients

- For house hacking – Get pre-approved for an FHA or conventional loan. Start property shopping with a real estate agent who understands STR investing

- Set up your business entity – Form an LLC for liability protection. Open a separate business bank account. Get STR insurance

Week 3: Prepare and Furnish

- Furnish strategically – Prioritize: comfortable bed and quality linens first, living room seating second, kitchen essentials third. Everything else can wait

- Professional photography – This is not optional. Properties with professional photos earn 24-40% more per booking. Invest $150–$300 for a photographer or learn to shoot with natural light and a smartphone tripod

- Write your listing – Highlight what makes your space unique. Be specific about amenities. Mention proximity to local attractions. Your title should include the neighborhood and a key differentiator

- Install smart lock – Self-check-in improves guest satisfaction and eliminates the need for physical key exchanges. A $150 smart lock pays for itself immediately in operational simplicity

Week 4: Launch and Optimize

- Go live on Airbnb – Create your listing. Set your calendar for at least 90 days out

- Price aggressively for your first 3-5 bookings – Set rates 15-20% below comparable listings to attract your first guests and build reviews. Reviews are everything on Airbnb. A listing with 0 reviews converts at roughly 30% the rate of one with 10+ positive reviews

- Cross-list on VRBO and Booking.com – Multi-platform listings increase visibility by 30-40%. Use a channel manager to sync calendars and avoid double bookings

- Activate dynamic pricing – Once you have 3-5 reviews, switch to algorithmic pricing. This alone can increase revenue by 15-25% annually

Which Method Is Right for You?

Decision-making shouldn’t be complicated. Answer these three questions:

Question 1: How much capital do you have right now?

- $0 – Co-hosting, property management, or Airbnb Experiences. Start building experience and cash flow with zero risk

- $1,000–$5,000 – Rental arbitrage. This is the sweet spot for most people breaking into the Airbnb business. You have enough for a deposit and basic furnishing

- $5,000–$15,000 – Rental arbitrage (2-3 units) or seller financing on a small property

- Existing home equity – Cash out refinance or HELOC to fund a rental property purchase or Airbnb arbitrage portfolio

Question 2: Do you want to own the property?

- Yes – House hacking (FHA loan), seller financing, DSCR loan, or equity-based financing

- No – Rental arbitrage, co-hosting, or property management. Many operators build six-figure businesses without ever owning property

Question 3: How fast do you need income?

- This month – Co-hosting or listing a spare room. You can have bookings within 7-14 days

- Within 60 days – Rental arbitrage. Budget 30-45 days from lease signing to first guest

- Within 90 days – House hacking or seller financing (property transactions take longer)

How 10XBNB Students Build Airbnb Portfolios from Nothing

Theory is useless without proof. Here’s what I see consistently from students who start an Airbnb business with little or no money:

The arbitrage sprint pattern: Student signs one lease, furnishes the unit for under $3,000, gets it to 70%+ occupancy within 60 days, then uses the cash flow from unit one to fund unit two. By month four, they have two producing units. By month eight, three or four. This compounding effect is why rental arbitrage builds faster than almost any other real estate strategy. You’re reinvesting rental income directly into growth without waiting years to build equity.

The co-host-to-operator pipeline: Student starts managing 3-5 properties for other owners. Earns $1,500–$3,000/month in management fees. Uses that capital to sign their own arbitrage lease after 2-3 months. Now they’re managing other people’s units AND running their own. Combined income: $4,000–$8,000/month within six months, starting from zero.

The house hacker advantage: Student buys a duplex with an FHA loan (3.5% down). Lives in one unit, lists the other on Airbnb. Airbnb income covers the entire monthly mortgage payments. After 12 months, they refinance into a conventional loan, move out, and list both units. Then they buy another property using the same FHA strategy. Rinse and repeat.

The common thread? Nobody waited until conditions were “perfect.” They picked a method, took imperfect action, and iterated. The students who earn $10,000+/month didn’t start with money. They started with a plan and moved fast.

Common Mistakes When Starting an Airbnb Business With No Money

I’ve seen enough failed launches to know where people go wrong. Avoid these:

- Skipping market research – Signing a lease without checking AirDNA data, local regulations, or comparable listings is gambling, not investing. Spend a week on research before you spend a dollar on a deposit

- Overfurnishing – You don’t need a $5,000 living room. Guests care about cleanliness, comfort, and WiFi speed. A $2,000 furnished unit with professional photos outperforms a $6,000 unit with phone pictures every time

- Ignoring regulations – Getting shut down by code enforcement after furnishing a unit is an expensive lesson. Pull permits, register your STR, and follow local ordinances from day one

- No emergency fund – If you launch with zero reserves and have a slow first month, you can’t cover rent. Always have two months’ rent in reserve before going live

- Pricing too high at launch – New listings with zero reviews can’t command premium rates. Start low, build reviews, then raise prices. Ego pricing kills new listings

- Single-platform dependency – Listing only on Airbnb limits your exposure. Cross-list on VRBO, Booking.com, and direct booking sites to maximize occupancy

- No business entity – Operating without an LLC exposes your personal assets to liability. A guest slips and falls? Without an LLC, your personal bank account is on the hook

- Underestimating cleaning costs – Turnovers are the highest variable expense in the Airbnb business. Budget $80–$150 per turnover and factor this into your pricing model

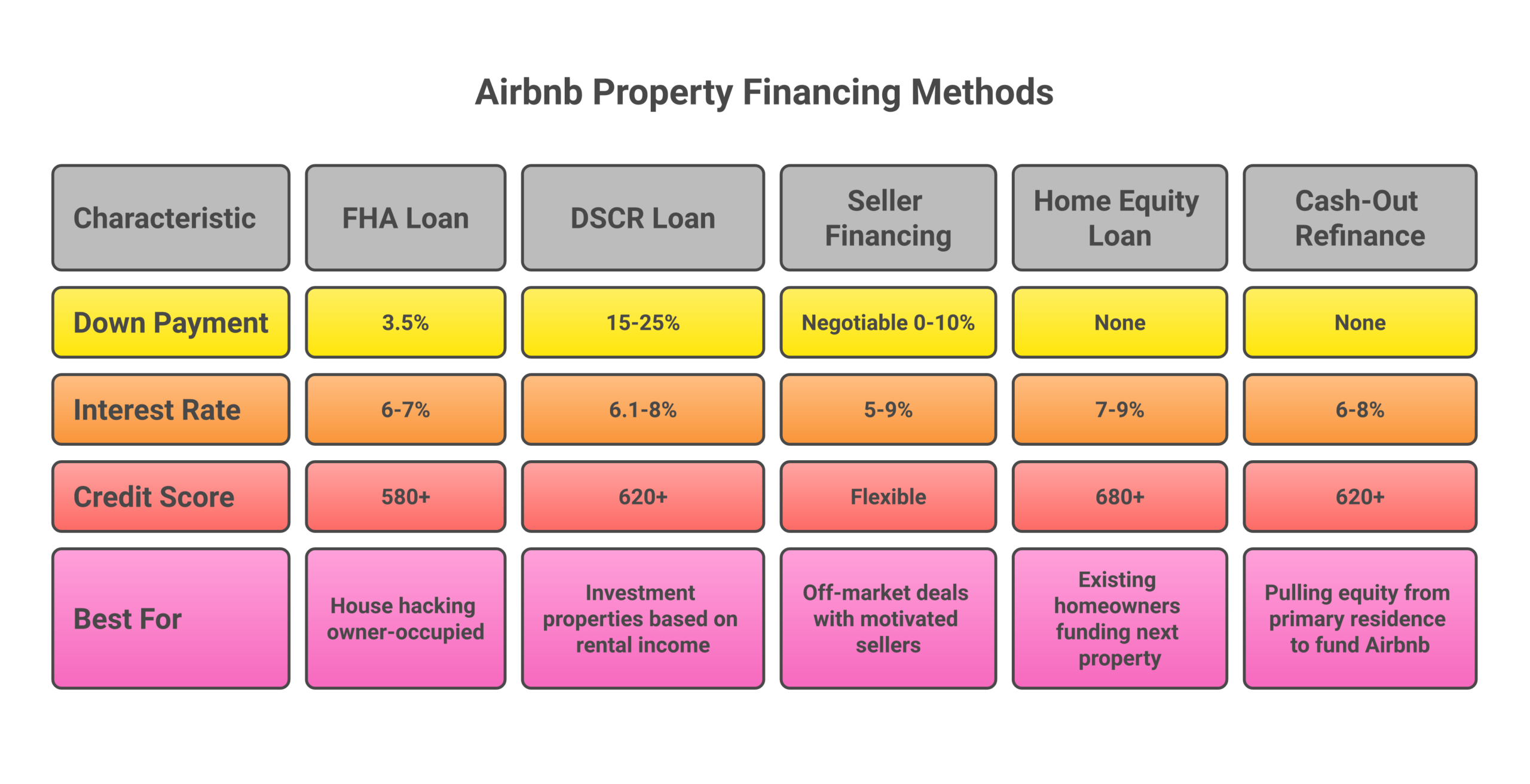

Financing Comparison: Every Way to Fund Your First Airbnb Property

For those who want to eventually own their investment property, here’s every financing method available ranked by how much capital you need upfront:

| Financing Method | Down Payment | Interest Rate (2026) | Credit Score | Best For |

|---|---|---|---|---|

| FHA Loan | 3.5% | 6-7% | 580+ | House hacking (must owner-occupy) |

| Conventional | 5-20% | 6.5-7.5% | 620+ | Primary or investment property |

| DSCR Loan | 15-25% | 6.1-8% | 620+ | Investment property (no income docs) |

| Seller Financing | 0-10% | 5-9% | Flexible | Off-market deals, flexible terms |

| HELOC | None (uses equity) | 7-9% | 680+ | Existing homeowners |

| Cash Out Refinance | None (taps equity) | 6-8% | 620+ | Pulling equity from existing mortgage |

| Investor Capital | $0 (investor funds) | N/A (profit split) | N/A | Operators with deal flow, no capital |

| Hard Money | 10-20% | 10-15% | Flexible | Short-term bridge to permanent financing |

The lowest-barrier path for most aspiring Airbnb operators: start with rental arbitrage (no property purchase needed), build cash flow, then use that income to fund a down payment on your first owned rental property through a DSCR loan or conventional mortgage. This is the playbook that real estate investors in the STR space use to scale from zero to portfolio ownership without needing family money or a six-figure salary.

How Much Do Airbnb Hosts Actually Make?

Airbnb host income varies dramatically based on location, property type, and operational quality. But here are the realistic ranges based on what I see across hundreds of operators:

- Spare room rental – $500–$2,000/month. Low effort, low ceiling, but a great starting point

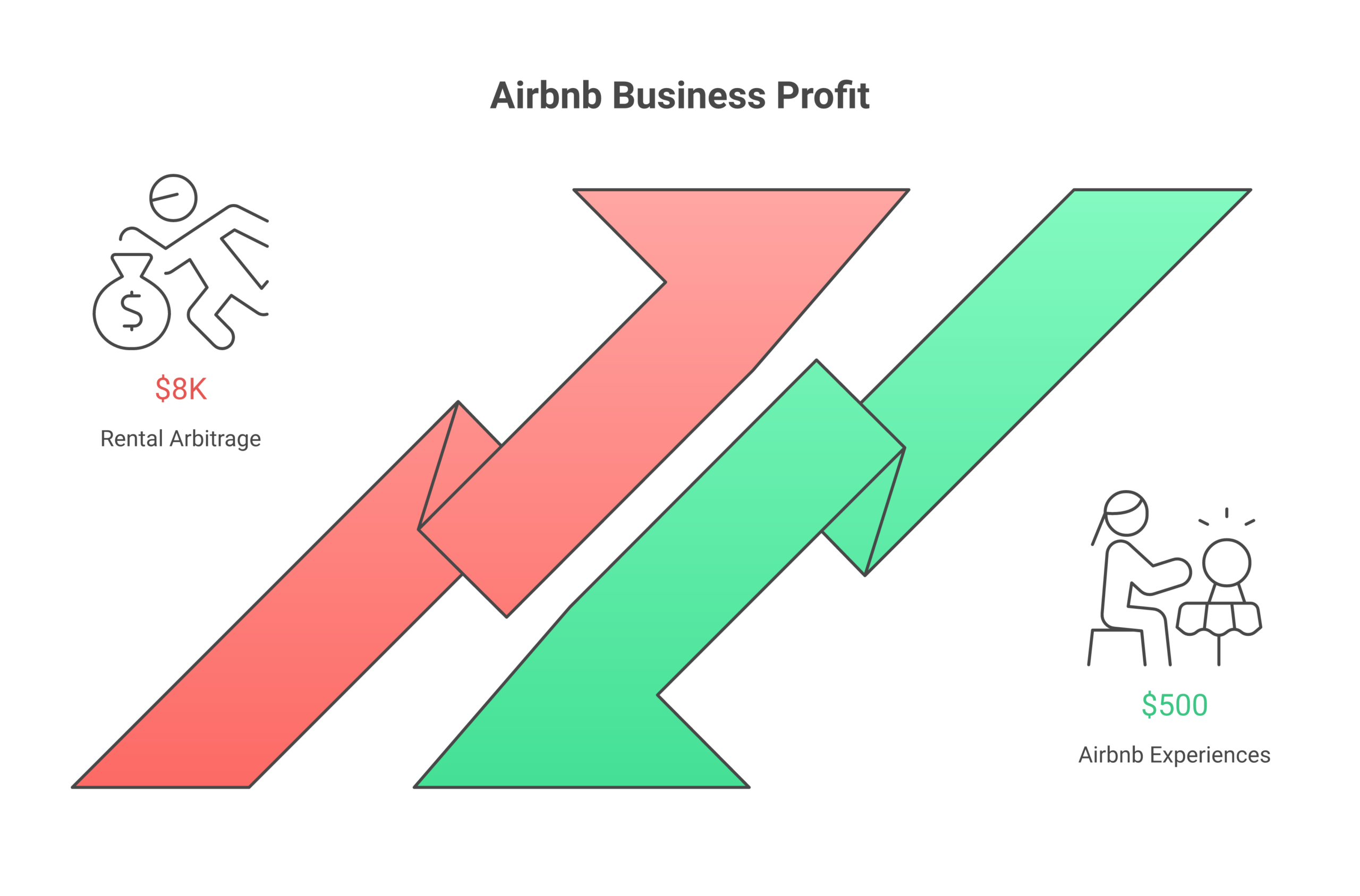

- Single arbitrage unit (mid-market) – $500–$1,500/month net profit after all expenses

- Single arbitrage unit (premium market) – $2,000–$8,000/month net profit in high-demand destinations

- Multi-unit arbitrage portfolio (3-5 units) – $3,000–$15,000/month depending on markets and occupancy

- Owned investment property – $1,000–$5,000/month net after monthly mortgage payments, depending on equity position and market value of the property

- Property management portfolio (10+ units) – $5,000–$20,000/month in management fees

The people who earn at the top of these ranges do three things consistently: they pick the right markets, they obsess over guest experience (which drives reviews and repeat bookings), and they use dynamic pricing to extract maximum revenue from every night.

Frequently Asked Questions

Can you really start an Airbnb with no money?

Yes, but “no money” usually means no property purchase. Not zero dollars ever. Co-hosting and Airbnb Experiences genuinely cost $0 to start. Rental arbitrage requires $2,000–$5,000 for a deposit and furnishing. Creative financing (seller financing, investor capital, home equity loans) lets you acquire an airbnb property with little or no money from your own pocket.

What is the cheapest way to start an Airbnb business?

Co-hosting other people’s properties costs nothing upfront. You manage their listing for 10-25% of revenue. If you want your own listing, renting a spare room in your primary residence is the cheapest option. You already pay the rent or existing mortgage, so incremental costs are just supplies and cleaning.

Is rental arbitrage legal?

Airbnb rental arbitrage is legal in most jurisdictions as long as you have the property owner’s written permission to sublet and comply with local short-term rental regulations. Some cities ban or restrict STRs entirely, so always check local ordinances before signing a lease.

How much money do you need for Airbnb arbitrage?

Budget $2,000–$5,000 for your first unit. This covers first month’s rent, security deposit, and basic furnishing. Aggressive operators who source used furniture and negotiate move-in specials have started with as little as $1,500–$2,800.

What is seller financing and how does it work for Airbnb?

Seller financing means the property owner finances your purchase directly instead of a bank. You negotiate a down payment (often 0-10%), interest rate (typically 5-9%), and monthly payments with the seller. There’s no bank qualification, no closing costs from a lender, and terms are fully negotiable. The seller holds the note until you pay interest and principal on the agreed schedule or refinance.

What is a DSCR loan?

A DSCR loan qualifies you based on the rental property’s projected income rather than your personal income. Lenders want to see that the property’s monthly rental income exceeds the monthly mortgage payments by at least 1.0-1.25x. Down payments range from 15-25%, interest rates start around 6.1% in 2026, and no W-2 or tax return is required.

Should I form an LLC for my Airbnb business?

Yes. An LLC separates your personal assets from your Airbnb business liabilities. If a guest gets injured or files a lawsuit, only the LLC’s assets are at risk. Not your personal savings, car, or home. Formation costs $50–$500 depending on your state.

How long does it take to get your first Airbnb booking?

Most new listings get their first booking within 7-14 days if priced competitively and listed with quality photos. If you haven’t received a booking after 21 days, your pricing is too high, your photos are weak, or your listing description needs work.

Can I do Airbnb without owning property?

Absolutely. Airbnb arbitrage, co-hosting, and property management all operate without owning property. Rental arbitrage is the most profitable non-ownership method, letting you control an airbnb property through a lease rather than a purchase. Many operators manage 10+ units without owning a single one.

What is a cash out refinance and how can it fund an Airbnb?

A cash out refinance replaces your existing mortgage with a larger loan, giving you the difference in cash. If your home has $100,000 in equity, you might pull $60,000–$80,000 in cash at a 6-8% interest rate. That capital can fund down payments on investment properties or furnish multiple airbnb rental arbitrage units.