Airbnb hosts running rental arbitrage need three types of insurance: Airbnb’s Host Protection (free, covers up to $1M liability), a commercial general liability policy ($500-$1,500/year), and short-term rental insurance from providers like Proper or CBIZ ($1,000-$3,000/year). Standard renter’s or homeowner’s policies won’t cover you. Here’s exactly what each policy covers and which ones you actually need.

I’ve watched arbitrage operators lose $8,000, $15,000, even $30,000+ because they assumed AirCover would step in. It didn’t. Over the past four years, I’ve tested policies from Proper Insurance, CBIZ, Safely, and Steadily across multiple rental property portfolios. This guide covers exactly what airbnb insurance rental arbitrage operators need, what you can safely skip, how much it costs per unit, and how to structure insurance solutions across a growing STR business without bleeding money on duplicate coverage.

Why Homeowners Insurance and Landlord Insurance Won’t Cover Rental Arbitrage

Before we get into what you need, you have to understand what doesn’t work. The most expensive mistake in the short-term rental industry isn’t picking the wrong insurance company. It’s assuming your existing coverage applies.

Homeowners Insurance: The Silent Policy Killer

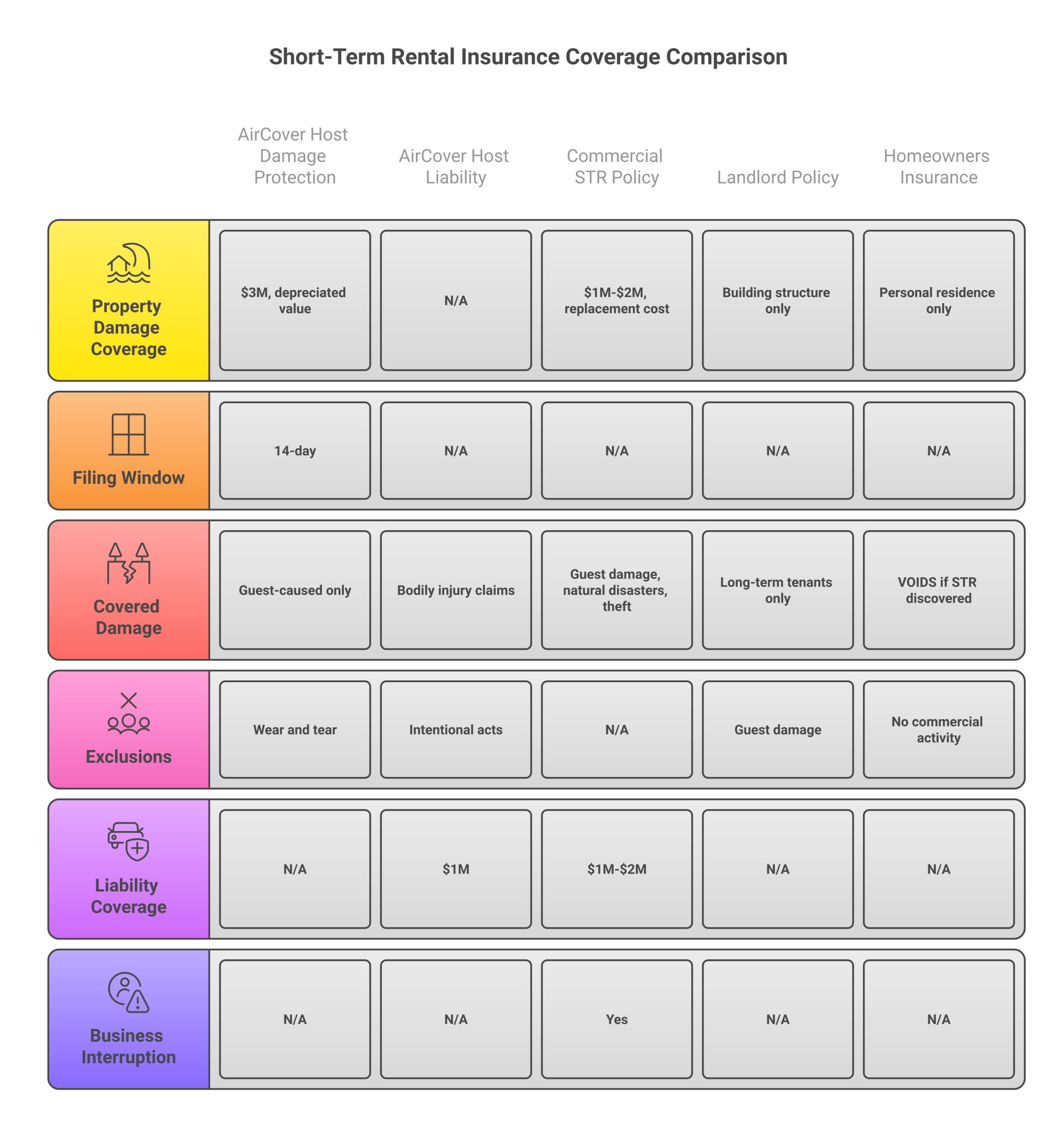

Standard homeowners insurance is designed for owner-occupied residences. The moment you list a property on Airbnb or any short-term rental platform, you’ve created a commercial activity that violates the core terms of a homeowners policy. Most carriers won’t just deny a claim, they’ll void the entire policy retroactively, leaving you uninsured for everything, including fire and theft.

This isn’t theoretical. I know a host in Nashville who had a kitchen fire during a guest stay. Her homeowners insurance denied the $47,000 claim because the property was listed on Airbnb. She lost coverage entirely and had to start from scratch with a new carrier at higher rates. That’s not a coverage gap. That’s a coverage cliff.

Landlord Insurance: Designed for the Wrong Tenant

Landlord insurance covers long-term tenant scenarios: a 12-month lease, steady occupancy, one family living there consistently. It does not cover guest-caused property damage from rotating short-term rentals, liability from strangers staying overnight, or the commercial revenue model that defines arbitrage.

Some landlord insurance policies explicitly exclude properties rented for fewer than 30 consecutive days. Others have blanket exclusions for “commercial hospitality” operations. Even if your insurance agent doesn’t flag the conflict, the claims adjuster will, right when you need coverage most.

The Lease Complication for Arbitrage Operators

If you don’t own the property, and in rental arbitrage, you typically don’t. There’s an additional layer. Your landlord’s property insurance doesn’t cover your business operations on their property. If a guest trips, falls, and sues, the lawsuit names both you and the property owner. Without proper insurance that lists the landlord as an additional insured, you’ve created a liability nightmare that could terminate your lease and your business simultaneously.

AirCover for Hosts: What It Actually Covers (and Where It Fails)

Airbnb rebranded their Host Guarantee and Host Protection Insurance as AirCover in late 2022. The headline figures, $3 million in host damage protection and $1 million in host liability insurance, look adequate on paper. They’re not.

What AirCover Does Cover

Host Damage Protection ($3M cap) reimburses you when a guest physically damages your property or belongings during a confirmed Airbnb stay. This includes broken furniture, stained carpets, holes in walls, and damaged appliances. The cap is per occurrence, not annual.

Host Liability Insurance ($1M cap) covers you if a guest or third party is injured at your property during a stay and you’re found legally responsible. This is underwritten by an actual insurance carrier and provides bodily injury and property damage liability protection up to $1 million per occurrence.

Where AirCover Falls Short

Here’s where the coverage gaps destroy arbitrage operators:

- Depreciated value only. AirCover reimburses at depreciated value, not replacement cost. That $2,500 couch your guest destroyed? After depreciation, you might get $800. A proper commercial insurance policy pays replacement cost, the actual price to buy an equivalent new item

- 14-day filing deadline. You must file a damage claim within 14 days of guest checkout or before the next guest checks in (whichever comes first). Miss this window and your claim is dead. Period. If you’re managing multiple short-term rentals with back-to-back bookings, this window can close before you even discover the damage

- Wear and tear excluded. That mattress sagging after 200 guests? Not covered. Carpet wearing thin? Nope. AirCover only covers acute guest-caused damage, not the accelerated depreciation that comes from running a commercial hospitality operation

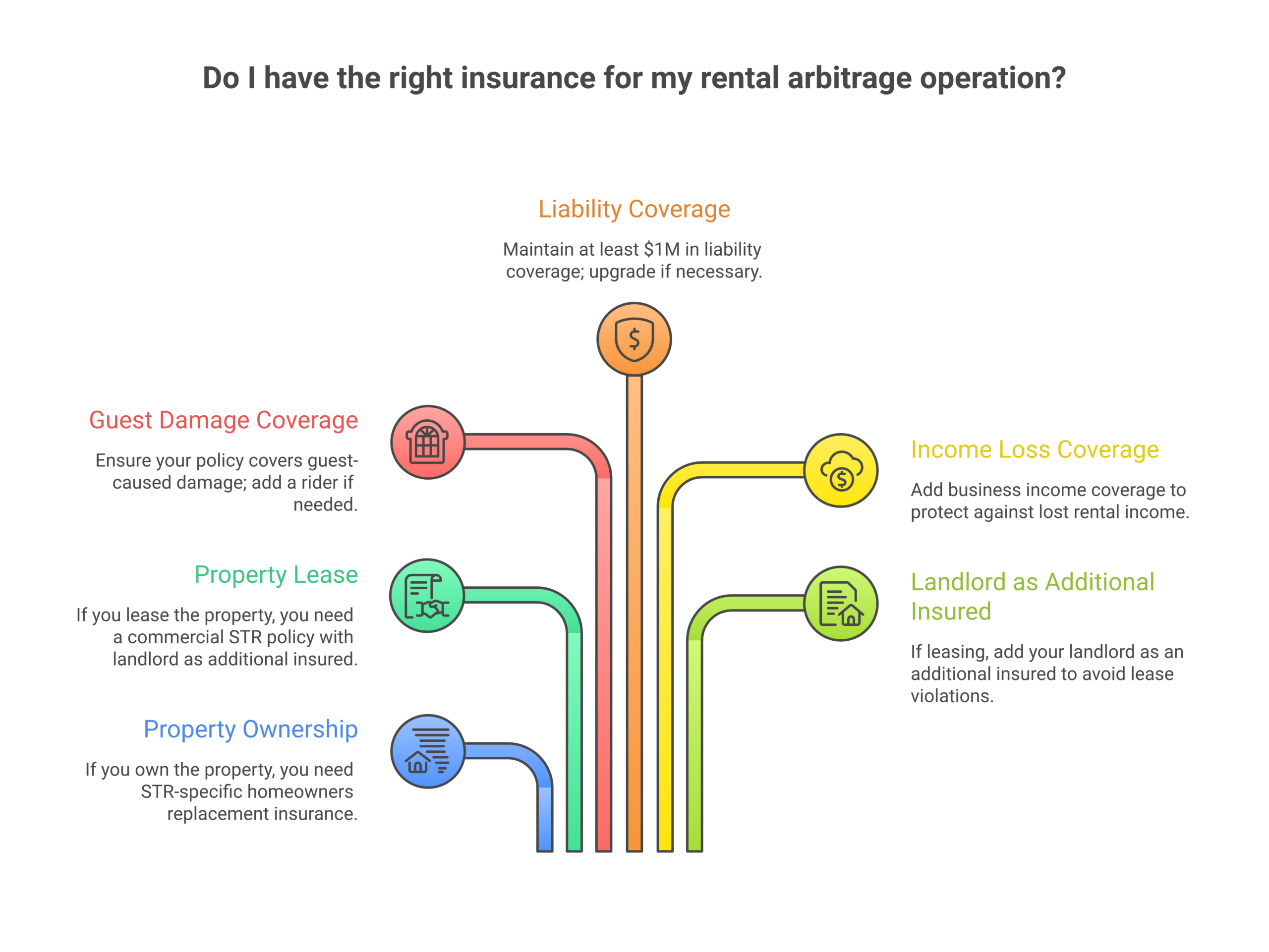

- No lost rental income coverage. If damage makes your property unbookable for two weeks, AirCover doesn’t reimburse the lost income. You eat those lost bookings. For an arbitrage unit generating $3,000-$5,000/month in revenue, two weeks of downtime is $1,500-$2,500 in lost rental income you’ll never recover

- No business interruption protection. A burst pipe, electrical failure, or HVAC breakdown that forces cancellations? Not AirCover’s problem. Business interruption coverage is commercial insurance territory

- Aggressive documentation requirements. AirCover requires timestamped photos before and after every stay, receipts for every item, and often a police report for theft. The documentation burden is designed to reduce payouts, and Airbnb’s community forums are filled with hosts reporting denied claims despite providing evidence

- Only covers Airbnb bookings. If you cross-list on Vrbo, Booking.com, or take direct bookings through an Airbnb direct booking website, AirCover provides zero protection for those stays. Your commercial policy needs to cover all booking channels

The Claims Denial Pattern

I’ve spoken with dozens of hosts who’ve filed AirCover claims. The pattern is consistent: small claims under $500 get paid relatively quickly. Claims between $500 and $2,000 face heavy scrutiny and documentation demands. Claims above $2,000 frequently get denied on technicalities, late filing, insufficient documentation, or Airbnb classifying the damage as “wear and tear” rather than guest-caused.

Does AirCover have value? Yes, as a supplementary layer for guest-caused damage on Airbnb bookings specifically. Should you rely on it as your primary coverage? Absolutely not. It’s a reimbursement program masquerading as insurance policies, and treating it otherwise is gambling with your STR business.

What Insurance You Actually Need for Rental Arbitrage

The right insurance stack for an airbnb arbitrage operation has three layers. Not two. Not one. Three. Each serves a distinct purpose, and skipping any layer creates exposure that can wipe out months of STR income.

Layer 1: Commercial Short-Term Rental Insurance (Non-Negotiable)

This is your foundation. A commercial short-term rental insurance policy replaces your homeowners insurance or renter’s insurance with coverage specifically designed for STR operations. Every legitimate STR insurance provider structures policies around the reality that strangers are sleeping in your short term rental property every few days.

What it covers:

- Guest-caused property damage at replacement cost (not depreciated value)

- Liability coverage for guest injuries ($1M-$2M per occurrence)

- Lost rental income during covered claim repairs (typically up to 12 months)

- Business interruption from covered perils (fire, water damage, storms)

- Theft by guests or third parties

- Vandalism and malicious damage

- Amenity coverage (pools, hot tubs, fire pits, bicycles)

Coverage limits to target: Minimum $1,000,000 in liability coverage per occurrence. For properties in high-litigation states (California, New York, Florida), consider $2,000,000. Property coverage should match full replacement cost of building contents, furnishings, and equipment.

Layer 2: Landlord Additional Insured Endorsement (Critical for Arbitrage)

This is the layer most arbitrage guides ignore completely, and it’s the one that keeps your lease alive. When you add your landlord as an additional insured on your commercial STR policy, you’re providing them with liability protection that extends from your business operations on their property.

Why this matters: If a guest sues after an injury, the lawsuit typically names both the operator (you) and the property owner (your landlord). Without this endorsement, your landlord’s own insurance has to defend the claim, and their carrier will immediately investigate whether they knew about your STR operation. If they didn’t, they may deny the landlord’s claim. If they did, the landlord’s premiums spike.

Either scenario ends your lease. The additional insured endorsement eliminates this risk and gives landlords confidence to approve your arbitrage LLC’s subletting arrangement.

Layer 3: Umbrella Liability Policy (Portfolio Protection)

Once you’re operating three or more short-term rentals, an umbrella liability policy becomes essential. This sits above your commercial policies and provides an additional $1M-$5M in liability protection that kicks in when your primary coverage limits are exhausted.

A single catastrophic incident, a structure fire that injures multiple guests, a drowning in a pool, carbon monoxide exposure, can generate liability claims that exceed $1M faster than you’d expect. An umbrella policy costs $300-$600/year for the first $1M in additional coverage and is the cheapest insurance per dollar of protection in your entire stack.

Short-Term Rental Insurance Providers: Honest Comparison

I’ve used or directly evaluated policies from five major STR insurance providers. Here’s what actually matters about each one. Not the marketing copy, but the claims experience, pricing reality, and coverage specifics.

Proper Insurance

Best for: Operators who want complete, no-gaps coverage and are willing to pay for it.

Proper writes dedicated short-term rental policies backed by Lloyd’s of London. Every policy starts at $1M in liability per occurrence with the option to increase to $2M. They cover the building (if owned), contents, lost rental income, business interruption, and amenity liability. Crucially, they offer landlord additional insured endorsements for arbitrage operators.

Cost: $1,200-$3,600/year per property ($100-$300/month), depending on location, property value, and coverage limits. Properties in hurricane zones or high-cost markets run toward the upper end.

Claims experience: Generally fast. Most hosts report 2-4 week claim resolution for straightforward property damage. Proper pays replacement cost, not depreciated value. This alone can save you thousands on a single covered claim.

Limitation: More expensive than competitors. Not ideal if you’re running thin margins on your first arbitrage unit. But you get what you pay for, and Proper’s coverage depth is unmatched in the STR insurance space.

CBIZ Vacation Rental Insurance

Best for: Operators scaling to 5+ units who want tailored commercial insurance with multi-property pricing.

CBIZ provides commercial insurance solutions specifically for short-term rental property portfolios. They offer flexible policy structures that can bundle multiple properties under a single master policy with per-location endorsements. This reduces administrative overhead and often produces better per-unit pricing at scale.

Cost: $1,000-$3,000/year per property ($85-$250/month). Multi-property discounts can bring per-unit costs down 15-25%.

Claims experience: Solid. CBIZ assigns dedicated account managers for portfolio clients, which streamlines the claims process compared to dealing with a general insurance company call center.

Safely

Best for: New arbitrage operators with 1-2 units who want lower fixed costs and integrated guest screening.

Safely’s model is unique: they charge per booking rather than a flat monthly premium. Each reservation includes guest screening (background check, identity verification) plus up to $1M in property damage coverage and $1M in liability coverage for that stay. This pay-per-booking approach means you only pay for insurance when you have guests.

Cost: $8-$12 per booking. For a property averaging 20 bookings/month, that’s $160-$240/month. For a property with 10 bookings/month, it’s $80-$120/month. The economics favor properties with fewer, longer stays.

Limitation: No business interruption coverage. No lost income protection. If a covered claim makes your property unbookable, Safely doesn’t reimburse the revenue gap. For this reason, I consider Safely a supplementary provider, not a standalone solution for serious arbitrage operators.

Steadily

Best for: Landlords and property owners who also do STR. Less ideal for pure arbitrage operators.

Steadily offers landlord insurance that explicitly covers short-term rental activity, a differentiator since most landlord insurance policies exclude short term rentals. Their online quoting process is fast (under 5 minutes), and policies can be bound same-day.

Cost: $960-$2,400/year ($80-$200/month). Competitive for property owners, but arbitrage operators may find the landlord-focused policy structure doesn’t perfectly fit their operational model.

Allstate HostAdvantage

Best for: Existing Allstate homeowners policyholders who occasionally rent their primary residence.

HostAdvantage is an add-on endorsement to existing Allstate homeowners policies. It extends coverage for theft, liability, and lost income during guest stays. It’s not a standalone commercial STR policy. It’s a rider that modifies your homeowners coverage to accommodate occasional short-term rentals.

Cost: $300-$800/year ($25-$65/month) on top of your existing homeowners premium.

Limitation: Not designed for full-time arbitrage operations. Coverage limits are lower, and the policy assumes STR is secondary to personal use. If you’re running a property as a dedicated vacation rental, HostAdvantage isn’t sufficient.

Provider Comparison Table

| Provider | Liability Limit | Property Damage | Lost Income | Monthly Cost | Best For |

|---|---|---|---|---|---|

| Proper Insurance | $1M-$2M | Replacement cost | Up to 12 months | $100-$300 | Complete coverage |

| CBIZ | $1M-$2M | Replacement cost | Up to 12 months | $85-$250 | Multi-property portfolios |

| Safely | $1M/stay | $1M/stay | None | $80-$240* | Low-volume properties |

| Steadily | $1M | Actual cash value | Yes (limited) | $80-$200 | Property owners doing STR |

| Allstate HostAdvantage | $500K-$1M | Varies | Limited | $25-$65 | Occasional hosting |

*Safely pricing varies based on booking volume; shown range assumes 10-20 bookings/month.

How Much Does Rental Arbitrage Insurance Actually Cost?

Total insurance cost per arbitrage unit depends on your location, coverage limits, property value, and how many units you’re operating. Here’s what the real numbers look like based on my portfolio and conversations with dozens of operators.

Single-Unit Cost Breakdown

| Coverage Component | Monthly Cost | Annual Cost |

|---|---|---|

| Commercial STR policy | $100-$300 | $1,200-$3,600 |

| Landlord additional insured | Included or $10-$25 | Included or $120-$300 |

| Umbrella (prorated per unit) | $10-$25 | $120-$300 |

| Total per unit | $120-$350 | $1,440-$4,200 |

For context, if your arbitrage unit generates $3,000/month in gross revenue and you’re paying $1,500/month in rent, insurance at $150-$250/month represents 5-8% of gross revenue. That’s a reasonable cost of doing business. If that premium eats too much margin, the unit’s economics were already marginal, insurance isn’t the problem, the deal is.

How Monthly Rent Affects Insurance Economics

Insurance costs as a percentage of revenue stay relatively stable regardless of your monthly rent. A $1,200/month apartment and a $3,000/month luxury condo cost roughly the same to insure if coverage limits are equivalent. The difference is in what percentage of your revenue that insurance represents.

On a high-margin unit, say, $5,000/month gross revenue on $2,000/month rent, $200/month in insurance is 4% of gross. Easily absorbed. On a thin-margin unit, $2,500/month revenue on $1,800/month rent, that same $200 is 8% of gross and 29% of your net margin before other expenses. That’s a much harder pill to swallow, which is why running your profit numbers before signing a lease matters so much.

Portfolio-Scale Insurance Strategies

Once you pass five units, commercial insurance pricing changes significantly. Bundle discounts, master policy structures, and higher deductibles (in exchange for lower premiums) become available. Here’s how I think about insurance at scale:

- 1-3 units: Individual policies from Proper or CBIZ. Total cost: $150-$300/month per unit. Simple, straightforward, easy to manage

- 4-7 units: Master policy with per-location endorsements. 15-20% discount vs individual policies. One renewal date, one payment, one claims contact

- 8+ units: Custom commercial program through a broker. Negotiate higher deductibles ($2,500-$5,000) for lower premiums. Self-insure small claims, transfer catastrophic risk to the carrier. At this scale, you should be working with a specialized insurance agent who understands the short term rental industry

Liability Coverage: How Much Is Enough?

The short answer: $1M minimum per occurrence, $2M if you’re in a high-litigation state or have amenities like pools, hot tubs, or waterfront access.

Why $1M Is the Floor

A single slip-and-fall injury at your short term rental property can generate medical bills exceeding $100,000. Add legal fees, pain and suffering claims, and potential negligence findings, and you’re looking at settlements in the $300,000-$700,000 range for moderate injuries. Spinal injuries, drownings, or wrongful death claims routinely exceed $1M.

Liability coverage at $1M per occurrence with $2M aggregate is the industry standard for a reason. It covers the vast majority of injury scenarios while keeping premiums manageable. Going below this threshold to save $20/month is the definition of penny-wise and pound-foolish.

When You Need $2M

Increase your liability coverage limits to $2M per occurrence if:

- Your property has a swimming pool, hot tub, dock, or waterfront access

- You operate in California, New York, Florida, or New Jersey (historically high jury awards)

- Your property regularly hosts families with children

- You offer experiences or activities (kayaks, bicycles, fire pits)

- Your property is multi-story with exterior staircases or balconies

The cost difference between $1M and $2M in liability protection is typically $15-$30/month. Against the risk exposure, that’s the best insurance investment in your entire stack.

Lost Rental Income and Business Interruption Coverage

This is the coverage category that separates adequate insurance from excellent insurance. AirCover doesn’t offer it. Most basic STR policies include it. And when you need it, it’s the difference between weathering a crisis and hemorrhaging cash.

What Lost Rental Income Coverage Does

If a covered peril (fire, flood, storm damage, major plumbing failure) makes your property unbookable, lost rental income coverage reimburses the revenue you would have earned during repairs. Most policies cover up to 12 months of lost income based on your documented booking history and revenue records.

For an arbitrage operator paying $2,000/month in rent on a unit that generates $4,500/month in bookings, a two-month repair period without lost income coverage means:

- $4,000 in rent still owed to your landlord (the lease doesn’t pause)

- $9,000 in lost rental income

- $13,000 total financial impact, before repair costs

With lost income coverage, you recover the $9,000 in lost revenue (minus your deductible), reducing your exposure to just the rent obligation and deductible. That’s the difference between a setback and a business-ending event.

Business Interruption vs. Lost Income: What’s the Difference?

These terms overlap but aren’t identical. Lost rental income coverage specifically replaces revenue from bookings you couldn’t fulfill. Business interruption coverage is broader. It can also cover continuing fixed expenses (rent, utilities, subscriptions, loan payments) that you must pay regardless of whether the property is generating income.

For arbitrage specifically, business interruption coverage is more valuable because your biggest ongoing cost, the monthly rent, continues even when the property is down. Look for policies that explicitly cover “continuing expenses” during a covered claim period.

How to Structure Insurance Across Your Arbitrage Portfolio

As your STR business grows from one unit to many, your insurance strategy needs to evolve. Here’s the approach that minimizes cost while maintaining complete coverage.

Phase 1: Your First Arbitrage Unit (1-2 Properties)

Keep it simple. Get a standalone commercial STR policy from Proper Insurance or CBIZ. Add your landlord as additional insured. Make sure you have at least $1M in liability coverage and replacement cost property damage coverage.

At this stage, your insurance agent relationship matters more than the carrier brand. Find an agent who specializes in short-term rental insurance. Not a generalist who Googles “STR insurance” while you’re on the phone. A specialist knows which exclusions to watch for, which endorsements to add, and how to structure the policy for your specific market.

Phase 2: Building Your Portfolio (3-5 Properties)

Consolidate to a single carrier if possible. Request multi-property pricing. Add an umbrella liability policy at $1M above your base coverage. This is also when you should formally structure your business as an LLC (if you haven’t already) and ensure all insurance policies are in the LLC’s name, not your personal name.

Review your arbitrage LLC structure with both your insurance agent and attorney. The LLC provides legal liability protection; the insurance provides financial protection. They’re complementary, not redundant.

Phase 3: Scaling Operations (6+ Properties)

Work with a commercial insurance broker. Not a single-carrier agent. A broker shops multiple carriers on your behalf and can build custom policy structures that a single-company agent can’t. At this scale, you’re looking at:

- Master commercial policy with per-location schedules

- Higher deductibles ($2,500-$5,000) for lower premiums

- Umbrella policy at $2M-$5M

- Possibly a self-insurance reserve for claims under your deductible

- Workers’ compensation if you have cleaning or maintenance employees

At six-plus units, insurance typically runs $100-$175/month per unit at portfolio pricing, significantly cheaper than the $200-$300/month you’d pay with individual policies.

Airbnb Arbitrage Legal Requirements: Insurance and Regulations

Insurance isn’t just smart business, in many jurisdictions, it’s legally required. Short term rental regulations vary by location, and the intersection of STR regulations and insurance mandates varies wildly by city and state, and ignorance isn’t a defense.

States and Cities That Require STR Insurance

A growing number of municipalities require short-term rental operators to carry minimum liability coverage as a condition of their STR permit or license. Common requirements include:

- $500,000-$1,000,000 in commercial liability coverage

- Proof of insurance submitted with permit application and at each renewal

- Landlord notification or consent for non-owner-occupied properties

- Certificate of insurance naming the city as certificate holder

Cities with explicit STR insurance requirements include (but aren’t limited to): San Francisco, Portland, New Orleans, Nashville, Denver, and Austin. Check your local airbnb arbitrage legal requirements before signing a lease, discovering you need a $1M policy after you’ve committed to rent payments creates unnecessary financial pressure.

Insurance as a Lease Negotiation Tool

Here’s something most arbitrage guides miss: proper insurance is your strongest lease negotiation asset. When you approach a landlord about subletting for short-term rentals, their biggest fear is liability. When you can show them a $1M commercial policy with their name as additional insured, you’ve eliminated their primary objection.

I’ve seen landlords who initially rejected arbitrage proposals reverse their decision once they saw the insurance package. The additional insured endorsement costs you nothing (or a negligible $10-$25/month), but it provides the landlord with free liability protection they wouldn’t otherwise have. Frame it as a benefit to them, because it genuinely is.

The Insurance Claim Process: What to Do When Things Go Wrong

Having insurance is useless if you can’t collect on it. The claims process for STR insurance follows a specific workflow, and preparation is everything.

Before Any Claim: Documentation Protocol

Set up a documentation system from day one, before any damage occurs. This baseline evidence is what makes or breaks a covered claim:

- Photo inventory: Photograph every room, every item of value, and all appliances before your first guest. Use a timestamped photo app. Update after any furniture or equipment changes

- Receipt archive: Keep digital copies of receipts for all furnishings, electronics, linens, kitchenware, and decor. Your insurance company needs proof of value to calculate replacement cost

- Booking records: Maintain exportable records of all bookings, revenue, and occupancy rates. This documentation supports lost rental income claims

- Maintenance log: Document all maintenance, repairs, and property improvements with dates and costs. This demonstrates responsible property management and strengthens any claim

When Damage Occurs: Step-by-Step

- Document immediately. Photograph all damage before cleaning or repairing anything. Video is even better. Get close-ups and wide shots that show context

- Notify your insurance company within 24 hours. Most commercial policies require “prompt notice” of any incident that could lead to a claim. Don’t wait to assess the full extent of damage, file preliminary notice immediately

- File with AirCover simultaneously if the booking was on Airbnb. Your commercial insurer typically expects you to pursue all available first-party reimbursement. But don’t wait for AirCover’s resolution before proceeding with your commercial claim

- Get repair estimates. Obtain two to three written estimates from licensed contractors. Your adjuster will use these to evaluate the claim

- Don’t accept the first offer. Insurance adjusters start with lower settlement amounts. If the offer doesn’t cover your actual replacement cost, negotiate. Provide additional documentation, comparable pricing, and be specific about why the offer is insufficient

The Dual-Filing Strategy

File with AirCover first for any Airbnb booking-related damage. Your commercial insurer expects you to pursue all available first-party reimbursement before they step in. However, don’t wait for AirCover’s resolution before notifying your insurer, file preliminary notice with both simultaneously, then let AirCover process first. If AirCover denies or underpays, your commercial policy picks up the remainder (minus your deductible). This dual-filing approach maximizes your recovery while satisfying both parties’ requirements.

Common Insurance Mistakes That Cost Arbitrage Operators Thousands

After reviewing insurance setups for over 50 arbitrage operators, the same mistakes keep showing up. Avoid these and you’ll be better protected than 90% of hosts.

Mistake 1: Relying on AirCover as Primary Coverage

Already covered above, but it bears repeating: AirCover is supplementary host damage protection, not business insurance. Treat it as a bonus reimbursement layer, never as your foundation.

Mistake 2: Not Telling Your Insurance Company About STR Activity

If you have a personal renter’s policy or homeowners insurance and start doing arbitrage without informing your carrier, you’ve created a coverage void. The moment you file a claim related to STR activity, the investigation will reveal the commercial use, and your claim, and possibly your entire policy, gets denied.

Mistake 3: Underinsuring Contents

Most arbitrage operators significantly underestimate the total value of furnishings, decor, electronics, linens, and kitchenware in a furnished rental. A properly furnished one-bedroom arbitrage unit typically has $8,000-$15,000 in contents. A two-bedroom with quality furnishings can reach $15,000-$25,000. Underinsuring means paying premiums for coverage that won’t make you whole after a major loss.

Mistake 4: Skipping Lost Income Coverage to Save $20/Month

This is the coverage cut that seems reasonable until you need it. Saving $240/year by dropping lost rental income coverage looks smart until a burst pipe takes your unit offline for six weeks and costs you $7,000+ in lost bookings plus ongoing rent obligations.

Mistake 5: Not Adding the Landlord as Additional Insured

For rent arbitrage operators specifically, this omission can end your business. Without it, a single liability incident can trigger lease termination, and you lose both the property and the income. The cost to add this endorsement is negligible. The cost of not having it is potentially everything.

Tax Implications of STR Insurance

Good news: insurance premiums for your rental arbitrage business are fully tax-deductible as a business expense. This applies to:

- Commercial STR insurance premiums

- Umbrella policy premiums (prorated to business use)

- Any insurance endorsements or riders

- Deductible amounts paid on covered claims

Your insurance costs reduce your taxable rental income dollar-for-dollar. At a 25% effective tax rate, a $200/month insurance premium has an after-tax cost of $150/month. That context matters when evaluating whether complete coverage is “too expensive.” For a full breakdown of STR tax strategy, see our Airbnb tax guide.

Airbnb Insurance for Rental Arbitrage FAQ

Does Airbnb provide insurance for hosts?

Airbnb provides AirCover, which includes Host Damage Protection (up to $3M) and Host Liability Insurance (up to $1M). However, AirCover is not a substitute for commercial insurance. It only covers Airbnb bookings, reimburses at depreciated value, excludes lost rental income and business interruption, and has a 14-day filing deadline that catches many hosts off guard. Every serious arbitrage operator needs a standalone commercial short-term rental insurance policy in addition to AirCover.

How much does short-term rental insurance cost for arbitrage?

Expect to pay $120-$350/month per property for complete coverage including commercial STR policy, landlord additional insured endorsement, and prorated umbrella coverage. Annual costs range from $1,440 to $4,200 per unit. Multi-property operators typically pay less per unit (15-25% discount) through bundled or master policies. The exact cost depends on location, property value, coverage limits, and deductible selection.

Can I use renter’s insurance for Airbnb arbitrage?

No. Standard renter’s insurance excludes commercial activity, including short-term rental operations. Using renter’s insurance for arbitrage can void your policy entirely, leaving you uninsured for both personal belongings and business operations. You need a commercial short term rental insurance policy specifically designed for STR activity.

What is the minimum liability coverage for rental arbitrage?

The industry standard minimum is $1,000,000 per occurrence in liability coverage. Many experienced operators and some local regulations require $1M-$2M. If your property has pools, hot tubs, or waterfront access, $2M is strongly recommended. Going below $1M to save money exposes you to personal financial ruin from a single serious injury claim.

Does my landlord need to be on my insurance policy?

For arbitrage operators: yes. Adding your landlord as an “additional insured” on your commercial STR policy protects them from liability arising from your business operations. Most sophisticated landlords require this as a lease condition. Even if your landlord doesn’t require it, adding them costs very little ($0-$25/month) and significantly reduces the risk of lease termination after an incident.

What’s the difference between replacement cost and actual cash value?

Replacement cost coverage pays the full price to buy an equivalent new item. Actual cash value (ACV) deducts depreciation from the payout. For a $2,000 sofa that’s three years old, replacement cost pays $2,000 (the price of a new equivalent sofa). ACV might pay $800-$1,200 after depreciation. AirCover pays depreciated value. Commercial STR policies from providers like Proper and CBIZ typically offer replacement cost coverage. Always choose replacement cost, the premium difference is minimal, but the claims payout difference is enormous.

Does STR insurance cover damage from guests on platforms other than Airbnb?

Yes. A commercial short-term rental insurance policy covers your property regardless of which platform the booking came through, Airbnb, Vrbo, Booking.com, direct bookings, or any other channel. This is a critical advantage over AirCover, which only protects Airbnb bookings. If you cross-list on multiple platforms (and you should for maximum occupancy), commercial insurance is the only way to maintain consistent coverage across all booking sources.

Should I file claims with AirCover or my insurance first?

File with AirCover first for any Airbnb booking-related damage. Your commercial insurer typically expects you to pursue all available first-party reimbursement before they step in. However, don’t wait for AirCover’s resolution before notifying your insurer, file preliminary notice with both simultaneously, then let AirCover process first. If AirCover denies or underpays, your commercial policy picks up the remainder (minus your deductible). This dual-filing approach maximizes your recovery while satisfying both parties’ requirements.

Is short-term rental insurance tax deductible?

Yes. All insurance premiums related to your rental arbitrage business are fully deductible as ordinary business expenses. This includes your commercial STR policy, umbrella policy (prorated to business use), endorsements, and deductible amounts paid on claims. At a 25% effective tax rate, a $200/month premium effectively costs $150/month after the tax benefit.

How do I find an insurance agent who understands rental arbitrage?

Start with STR-specific providers (Proper Insurance, CBIZ, Safely) who work exclusively in this space. If you prefer a local insurance agent, ask specifically about their experience with short-term rental policies, whether they understand the difference between landlord policies and STR policies, and whether they can add a landlord as additional insured. If they can’t answer these questions confidently, find someone who can. The wrong agent can cost you thousands in coverage gaps you won’t discover until you file a claim.

Bottom Line: What to Do Right Now

If you’re operating even one arbitrage unit without commercial short-term rental insurance, stop reading and start calling providers. Every day without proper insurance is a day where a single incident could wipe out months of STR income, or worse.

Here’s your action plan:

- Today: Request quotes from Proper Insurance and CBIZ. Provide your property details, coverage needs, and ask about landlord additional insured endorsements

- This week: Compare quotes. Choose the policy that provides $1M+ liability coverage, replacement cost property damage, and lost rental income coverage

- Before your next guest: Bind the policy. Set up your documentation protocol (photos, receipts, booking records). Add your landlord as additional insured

- This month: Review your revenue projections to ensure insurance costs are factored into your unit economics. If insurance makes a unit unprofitable, the unit was already marginal

Insurance costs money. Not having insurance costs more. The operators who build lasting, scalable arbitrage portfolios treat insurance as infrastructure, not overhead. Get covered, document everything, and get back to growing your STR business.