Last Updated: April 2026

Reviewed by: 10XBNB Editorial Team | Insurance information verified against Airbnb Help Center, NAIC guidelines, and provider documentation

This article provides general information about insurance and Airbnb and short term rentals hosting. Coverage, premiums, and terms and requirements vary by state, property value, and provider. Always consult a licensed insurance agent for specific policy recommendations.

No, standard renters insurance does not cover Airbnb hosting. When you charge guests to stay in your rental property, that counts as commercial business activity, and nearly all standard renters insurance policies exclude business use. Your insurer will deny claims and may cancel your policy if they discover you have been hosting on Airbnb without disclosing it. Instead of relying on a standard renters policy, Airbnb hosts need one of these options: Airbnb’s free AirCover program ($1M liability, $3M damage protection), a dedicated short-term rental policy from Proper Insurance or CBIZ ($800-$2,500/year), a pay-per-booking plan from Safely ($5-15 per reservation), or a homeowners policy endorsement from carriers like Allstate HostAdvantage ($300-$600/year). This guide covers exactly why renters insurance fails, what AirCover protects and where it falls short, six insurance options with real costs by hosting scenario, and how to file claims when damage happens.

Why Renters Insurance Doesn’t Cover Airbnb

Standard renters insurance policies contain a business activity exclusion clause that automatically voids coverage when you use your rental home or property for commercial purposes. According to the National Association of Insurance Commissioners (NAIC), approximately 60% of standard homeowners’ and renters’ policies automatically void when you begin short term rental hosting.

What Renters Insurance Actually Covers

Traditional renters insurance is designed to protect you as a tenant for:

- Personal property damage: Your furniture, electronics, and belongings if damaged by covered perils (fire, theft, vandalism)

- Personal liability: If YOU accidentally injure someone or damage their home or property while living in your rental

- Additional living expenses: Hotel costs if your rental becomes temporarily uninhabitable due to covered damage

- Medical payments: Small medical bills ($1,000-$5,000) if a guest YOU invited is injured

The Commercial Activity Trigger

The instant you charge a guest to stay in your rental home or property, you’ve crossed from personal use to commercial activity. This triggers the business pursuits exclusion, which states that coverage does not apply to:

- Business operations conducted at the premises

- Rental or holding of premises for business purposes

- Liability arising from short term rental arrangements

The Real Risk: Claim Denial AND Policy Cancellation

If you host on Airbnb without proper coverage and file a claim, your insurance company will investigate. When they discover you’ve been operating a short-term rental, they will:

- Deny your claim (leaving you financially exposed)

- Cancel your entire renters insurance policy

- Report the cancellation to the insurance database, making future coverage more expensive or difficult to obtain

This has happened to thousands of hosts who assumed their existing coverage was sufficient. Industry data shows that 78% of hosts operating without dedicated short-term rental coverage have had claims denied when insurers discovered the commercial activity.

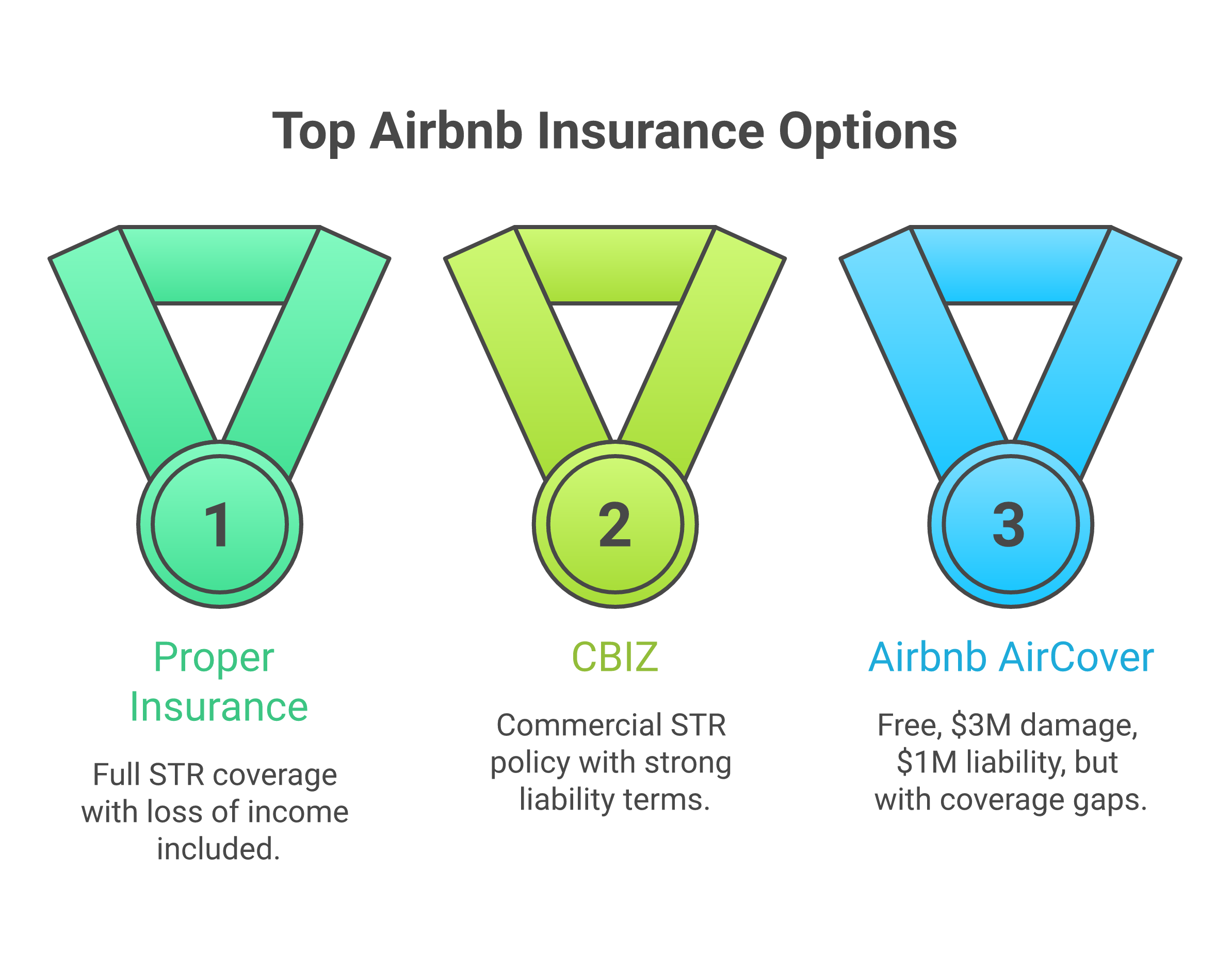

What Airbnb’s AirCover Actually Covers (And What It Doesn’t)

Airbnb’s AirCover program provides automatic protection for all hosts at no additional cost. However, understanding its limitations is critical for managing your risk exposure.

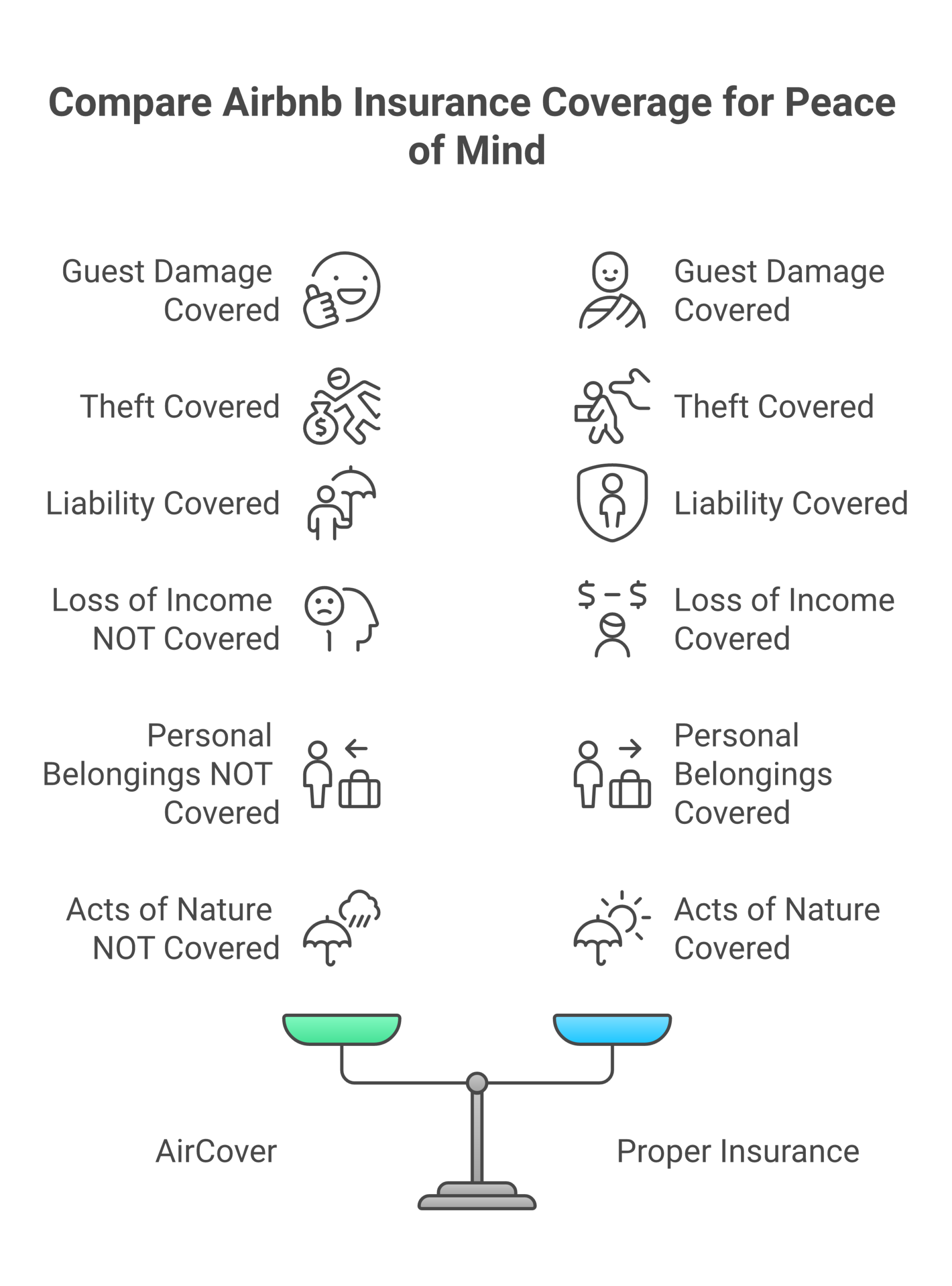

What’s Covered by AirCover

Host Liability Insurance: $1 Million

- Bodily injury to guests while on your home or property

- Property damage to guest belongings caused by you or your home or property

- Legal defense costs if a guest sues you

- Automatically applies to every booking

Host Damage Protection: Up to $3 Million

- Guest-caused damage to your home or property, furniture, and belongings

- Accidental damage during their stay

- Malicious damage by guests

- Covers repair or replacement costs

Experiences Liability Insurance: $1 Million

- Protection for hosts offering Airbnb Experiences

- Bodily injury or property damage during hosted activities

- Separate from accommodation coverage

Deep Cleaning Reimbursement

- Up to $200 for excessive cleaning beyond normal turnover

- Requires documentation and photos

Automatic Enrollment

- Every host is covered from their first booking

- No application or approval process required

- Coverage applies worldwide

Critical Gaps: What AirCover Does NOT Cover

Loss of Rental Income

If your home or property is damaged and becomes unrentable for weeks or months, AirCover does not compensate you for lost bookings. A fire or flood that requires 8 weeks of repairs could cost you $8,000-$20,000 in lost income with no reimbursement.

Bed Bug Infestations

AirCover explicitly excludes bed bug-related claims. Eradication costs $1,500-$5,000, and you’ll lose weeks of bookings during treatment and inspection periods.

Normal Wear and Tear

Gradual deterioration, stains from normal use, and expected depreciation are not covered. Only sudden, accidental damage qualifies.

Theft of Host Belongings (Limited Coverage)

While AirCover covers some theft, high-value items like electronics, jewelry, or collectibles often fall outside coverage limits or require separate documentation.

Acts of God / Natural Disasters

Hurricanes, floods, earthquakes, and other natural disasters are excluded. These require separate flood insurance or earthquake coverage through traditional insurers.

Pet Damage (Very Limited)

Despite Airbnb’s pet-friendly policies, pet-related damage claims are notoriously difficult to get approved through AirCover. Many hosts report denials for carpet damage, chewed furniture, and pet stains.

Cash, Securities, and Collectibles

Currency, stocks, bonds, rare coins, artwork, and collectibles are explicitly excluded from AirCover protection.

Your Personal Injury on the Property

If you’re injured while preparing the home or property or during a guest’s stay, AirCover provides no coverage. You’d need your own health insurance or a separate accident policy.

Damage to Common Areas

If you’re hosting a condo or apartment unit, damage to hallways, lobbies, pools, or other shared spaces is not covered by AirCover. Your HOA or building insurance may not cover short-term rental guest damage either.

Important AirCover Claim Limitation: You must report damage within 24 hours of guest checkout or within 24 hours before the next guest checks in, whichever is earlier. Missing this window can result in automatic claim denial.

6 Insurance Options That Actually Protect Airbnb Hosts

| Provider | Type | Annual Cost | Coverage | Best For | Key Benefit |

|---|---|---|---|---|---|

| Proper Insurance | Dedicated STR | $800-$2,500/yr | Up to $2M liability, income loss, bed bugs, $1M property damage | Full-time hosts (5+ properties or year-round hosting) | Most complete STR coverage; includes business interruption |

| Safely | Pay-per-booking | $5-15/booking | $5K damage protection + $1M liability per booking | Occasional hosts (<50 nights/year) | Only pay when you host; no annual commitment |

| Allstate HostAdvantage | Endorsement add-on | $300-$600/yr | Add-on to existing homeowners; $500K-$1M liability | Existing Allstate customers who host occasionally | Cheapest option if you already have Allstate |

| CBIZ | Commercial STR | $700-$1,200/yr | Business interruption + $1-2M liability + contents | Multi-property professionals (3+ units) | Strong business income protection; portfolio discounts |

| Liberty Mutual | Premium policy | $1,000-$5,000/yr | High-value contents + $2M+ liability + staff coverage | Luxury properties ($500K+ value) | Valuables riders, employee liability, concierge coverage |

| Foremost (Farmers) | Landlord + STR rider | $600-$1,500/yr | Landlord base policy with STR endorsement | Property owners who also do long-term rentals | Combined landlord/STR coverage; transition flexibility |

Proper Insurance

Proper is the most recognized dedicated short-term rental insurance provider in the U.S. They offer complete coverage specifically designed for Airbnb and VRBO hosts, including business interruption (lost rental income), bed bug eradication, and commercial general liability. Proper is ideal for hosts who treat Airbnb as a primary income source or manage multiple properties. Their policies can cover up to 40 properties under one portfolio policy with volume discounts.

Safely

Safely operates on a pay-per-booking model, charging $5-15 per reservation depending on property value and location. This makes it perfect for hosts who only rent occasionally or seasonally. There’s no annual premium, so you’re not paying for coverage during months when your home or property sits vacant. Safely provides $5,000 in damage protection (supplements AirCover) and $1 million in liability per booking.

Allstate HostAdvantage

If you already have an Allstate homeowners or renters policy, HostAdvantage is an endorsement you can add for $300-$600 annually. This is the most cost-effective option for existing Allstate customers who host their primary residence occasionally. It extends your existing coverage to include short-term rental activity that would otherwise be excluded. Note: Not available in all states; check with your Allstate agent.

CBIZ

CBIZ specializes in commercial insurance for short-term rental businesses. They’re particularly strong for hosts operating multiple properties as a business, offering business interruption coverage that reimburses you for lost rental income during repair periods. CBIZ policies can be customized with umbrella coverage, cyber liability (if you handle guest data), and employee coverage if you have cleaners or co-hosts on payroll.

Liberty Mutual

Liberty Mutual’s premium short-term rental policies are designed for high-value properties ($500,000+) and luxury hosts who offer concierge services or have valuable contents. They offer valuables riders for artwork, wine collections, and high-end furniture, as well as coverage for staff (housekeepers, property managers) and business activities beyond just accommodation. Premiums range from $1,000-$5,000 depending on property value and coverage limits.

Foremost (Farmers Insurance Group)

Foremost offers landlord insurance policies with short-term rental endorsements, making them ideal for property owners who do both long-term and short-term rentals or are transitioning between the two. Their policies provide flexibility to adjust coverage as your rental strategy changes. Premiums typically run $600-$1,500 annually depending on property location and value.

How Much Does Airbnb Host Insurance Cost? (By Scenario)

Scenario 1, Occasional Host (1 property, under 50 nights/year)

Profile: You rent out your primary residence when you travel 2-4 times per year, or rent a spare room occasionally.

Recommended Coverage:

- AirCover: Free (included with Airbnb)

- Supplemental: Safely pay-per-booking ($5-15 per booking)

Total Annual Cost: $250-$750

Calculation: If you host 50 nights per year at an average of $5-15 per booking (assuming 10-20 bookings depending on length), your total insurance cost is approximately $250-$750 annually. This is the most cost-effective option for occasional hosts who don’t want to pay for year-round coverage.

What’s Covered: Guest liability, damage protection, and supplemental coverage gaps that AirCover misses. You’re still exposed to business interruption risk, but the lower hosting frequency makes this acceptable for many occasional hosts.

Scenario 2, Full-Time Host (1-2 properties, year-round)

Profile: You rent out your home or property or properties consistently throughout the year, generating significant monthly income ($2,000-$10,000/month).

Travel nurses are the largest mid term tenant segment. See our renting to travel nurses for setup details.

Recommended Coverage:

- AirCover: Free (but insufficient alone)

- Primary Insurance: Proper Insurance or Allstate HostAdvantage

Total Annual Cost: $800-$1,500 per property

What’s Covered: Complete liability ($1-2M), property damage, business interruption (lost income), bed bug coverage, legal defense, and most gaps left by AirCover. This level of coverage is essential when Airbnb income is a primary revenue source.

Why It Matters: If your property is damaged and unrentable for 30-60 days, business interruption coverage reimburses you for lost income ($4,000-$15,000 depending on your nightly rate and occupancy). Without this coverage, you absorb the entire loss.

Scenario 3, Multi-Property Professional (3+ properties)

Profile: You operate a short-term rental business with 3 or more properties, generating $10,000-$50,000+ monthly in gross revenue.

Recommended Coverage:

- AirCover: Free (definitely insufficient)

- Primary Insurance: CBIZ or Proper Insurance multi-property policy

Total Annual Cost: $2,000-$5,000 (portfolio pricing with volume discounts)

What’s Covered: Commercial general liability ($2M+), business interruption for all properties, commercial property coverage, potential umbrella coverage ($5M+), and optional employee liability if you have staff. Portfolio policies often provide 15-25% discounts compared to insuring each property individually.

Additional Considerations: At this level, you may also need:

- Cyber liability insurance (if you manage bookings/payments through your own systems)

- Errors & omissions insurance (if you offer property management services)

- Workers’ compensation (if you have W-2 employees)

Scenario 4, Rental Arbitrage Operator (no property ownership)

Profile: You lease properties from landlords and sublet them on Airbnb without owning the real estate.

Recommended Coverage:

- AirCover: Free (doesn’t fully cover landlord’s property)

- Primary Insurance: Commercial general liability policy ($80-$200/month) + renter’s policy with business use rider

Total Annual Cost: $960-$2,400

What’s Covered: Liability for guest injuries, damage to the landlord’s property beyond what AirCover covers, your personal property (furniture, electronics you’ve added), and legal defense if the landlord sues you for lease violations or property damage.

Critical Note: Most rental arbitrage leases REQUIRE proof of insurance naming the landlord as an additional insured. Failing to maintain required coverage can result in immediate lease termination. Always submit insurance certificates to your landlord upon policy purchase and renewal.

Coverage Gap Analysis: What Each Insurance Type Covers

| Risk Scenario | AirCover | Standard Renters | STR Policy | Landlord Policy |

|---|---|---|---|---|

| Guest bodily injury on property | ✅ Yes ($1M) | ❌ No (business exclusion) | ✅ Yes ($1-2M) | ✅ Yes (limited) |

| Guest damages property/furniture | ✅ Yes ($3M) | ❌ No | ✅ Yes ($3M+) | ✅ Yes |

| Loss of rental income during repairs | ❌ No | ❌ No | ✅ Yes (Proper, CBIZ) | ⚠️ Sometimes |

| Bed bug infestation and treatment | ❌ No | ❌ No | ✅ Yes (Proper) | ❌ Rarely |

| Theft of your belongings by guest | ⚠️ Limited | ❌ No | ✅ Yes | ✅ Yes |

| Natural disaster damage (hurricane, flood, earthquake) | ❌ No | ⚠️ Yes (if primary residence) | ✅ Yes | ✅ Yes |

| Your personal injury on property | ❌ No | ✅ Yes | ⚠️ Depends | ❌ No |

| Pet damage to property | ⚠️ Very limited | ❌ No | ✅ Yes (most) | ⚠️ Depends |

| Legal defense costs if sued | ✅ Yes (included) | ❌ No | ✅ Yes | ✅ Yes |

| Damage to common areas (condos) | ❌ No | ❌ No | ⚠️ Sometimes | ✅ Yes |

| Cash, jewelry, collectibles theft | ❌ No | ⚠️ Limited | ⚠️ With rider | ⚠️ With rider |

| Liability for co-host or employee actions | ❌ No | ❌ No | ⚠️ With endorsement | ❌ No |

Key:

✅ Yes = Covered

❌ No = Not covered

⚠️ Limited/Depends = Partial coverage or coverage with terms and conditions

How to File an Insurance Claim (Step-by-Step)

Filing an AirCover Claim

Step 1: Document Damage Within 24 Hours

Take complete photos and videos of all damage immediately after guest checkout. Include:

- Wide shots showing the entire room or area

- Close-up shots of specific damage

- Photos of the same area in clean condition (from before checkout if possible)

- Timestamped images (most smartphones include this automatically)

Step 2: Obtain Repair Estimates or Receipts

- Get quotes from contractors, furniture retailers, or cleaning services

- For items that need replacement, find equivalent items online and screenshot prices

- For injuries, collect medical bills and incident reports

Step 3: Submit Through Airbnb Resolution Center

- Go to airbnb.com/resolutions

- Select the relevant reservation

- Choose “Request money for damages”

- Upload all documentation (photos, estimates, receipts)

- Clearly describe what happened and the financial impact

Step 4: Guest Response Period (24 Hours)

The guest has 24 hours to respond to your claim. They can:

- Accept and pay the claim voluntarily

- Dispute the claim with their own evidence

- Ignore the claim (defaults to Airbnb review)

Step 5: Airbnb Review (7-14 Days Typical)

Airbnb’s safety and claims team reviews all submitted evidence. They evaluate:

- Whether damage occurred during the reservation period

- If the damage is covered under AirCover terms

- Reasonableness of repair costs

- Guest’s response and evidence

Step 6: Decision: Payout or Denial

Airbnb will either:

- Approve the claim and process payment to your account (3-7 business days)

- Deny the claim with specific reasoning

- Request additional documentation before making a decision

Step 7: Appeal Process

If your claim is denied, you can appeal by submitting additional evidence within 14 days. Include:

- Additional photos or documentation

- Expert assessments (for structural damage)

- Witness statements (from cleaners, neighbors, co-hosts)

Common AirCover Claim Denials:

- Reported after the 24-hour window

- Insufficient photo evidence

- Damage classified as normal wear and tear

- Pre-existing damage visible in previous listing photos

- Damage amount below deductible thresholds

Filing a Third-Party Insurance Claim (Proper, CBIZ, etc.)

Step 1: Report Incident Immediately

Call your insurance provider’s claims hotline as soon as you discover damage or receive notice of an injury. Most policies require reporting within 24-72 hours. Provide:

- Your policy number

- Property address

- Description of incident

- Estimated damage amount

Step 2: File Police Report (If Applicable)

For theft, vandalism, or guest injuries requiring medical attention, file a police report. Insurance companies often require this for claims exceeding $2,500 or involving criminal activity.

Step 3: Document Everything

Gather complete evidence:

- Photos and videos of damage from multiple angles

- Receipts for items that need replacement

- Original purchase invoices (to establish value)

- Witness statements from cleaners, co-hosts, or neighbors

- Guest communication records (messages, reviews)

- Reservation confirmation and payment records

Step 4: Complete Insurer’s Claim Forms

Your insurance company will send claim forms (digital or paper). Complete all sections accurately:

- Date and time of incident

- Detailed description of what happened

- List of damaged items with estimated values

- Contact information for all parties involved

- Whether police were involved

Step 5: Adjuster Inspection (1-3 Business Days)

The insurance company will assign a claims adjuster who will:

- Visit the home or property to assess damage

- Take their own photos and measurements

- Interview you and potentially the guest (if still reachable)

- Verify that damage falls under covered perils

- Estimate repair or replacement costs

Step 6: Review Period (3-30 Days)

The insurance company reviews all documentation and the adjuster’s report. Timeline depends on claim complexity:

- Simple damage claims: 3-7 days

- Complex claims (structural damage, liability injury): 14-30 days

- Claims requiring investigation: 30-90 days

Step 7: Payout to Your Account

If approved:

- Payment is typically issued within 7-10 business days

- For property damage, payment may go directly to contractors

- For liability claims, payment goes to the injured party’s legal representative

- You’ll receive a claim settlement letter documenting the payout

Denied Claims: Next Steps

If your claim is denied:

- Request written explanation citing specific policy language

- Review your policy to verify the denial is accurate

- Provide additional evidence that addresses the denial reason

- If still denied, request a formal appeal or escalation to management

- Consider hiring a public adjuster (they take 10-15% of settlement but can increase payout)

State-Specific Insurance Requirements for Airbnb Hosts

Cities and States with Mandatory Insurance Requirements

Nashville, Tennessee

- Requirement: $1 million general liability insurance to obtain short-term rental permit

- Verification: Must submit proof of coverage with permit application and renewals

- Consequence: Operating without required insurance = permit revocation + fines up to $2,500

Austin, Texas

- Requirement: $300,000 liability insurance minimum for Type 1 and Type 2 STR licenses

- Verification: Annual submission of certificate of insurance

- Consequence: License denial or suspension until proof provided

Portland, Oregon

- Requirement: Proof of liability coverage for short-term rental permit

- Minimum: $1 million recommended, though no specific minimum stated

- Verification: Uploaded with annual permit renewal

Palm Springs, California

- Requirement: $1 million commercial general liability for STR permits

- Additional: Must name the City of Palm Springs as additional insured

- Consequence: Permit suspension for lapsed coverage

New Orleans, Louisiana

- Requirement: $500,000 general liability for short-term rental licenses

- Verification: Certificate of insurance submitted with application

- Additional: Many hosts carry $1M+ due to high-value properties

States with No Specific Requirement (But Strongly Recommended)

Most states, including Florida, Colorado, New York, California (outside specific cities), and Arizona, do not mandate insurance at the state level. However:

- HOAs and Condo Associations frequently require $1-2M liability and additional insured endorsements

- Mortgage lenders may require disclosure of STR activity and proof of appropriate coverage

- Landlords (for rental arbitrage) universally require proof of insurance

Always check your specific city and county terms and requirements before hosting. Regulations change frequently, and non-compliance can result in fines ranging from $500 to $10,000+ depending on jurisdiction.

Common Insurance Mistakes Airbnb Hosts Make

1. Assuming Renters or Homeowners Insurance Covers Hosting

The Mistake: 67% of new Airbnb hosts believe their existing renters or homeowners insurance automatically covers short-term rental activity.

The Reality: Standard policies explicitly exclude business use, including short-term rentals. If you file a claim and your insurance policy provider discovers you’ve been hosting, they will deny the claim and may cancel your policy entirely.

The Fix: Disclose your Airbnb activity to your current insurer and either add an endorsement (if available) or purchase dedicated STR coverage. Never assume existing coverage applies.

2. Relying Solely on AirCover

The Mistake: Thinking “Airbnb provides $3 million in coverage, so I’m fully protected.”

The Reality: AirCover has significant gaps including no coverage for lost rental income, bed bugs, theft of high-value items, natural disasters, or your personal injury. It’s a safety net, not complete protection.

The Fix: Treat AirCover as supplemental coverage, not primary insurance. Add dedicated STR insurance that covers business interruption, natural disasters, and items excluded by AirCover.

3. Not Disclosing STR Activity to Your Homeowners Insurer

The Mistake: Continuing to pay for homeowners insurance without telling your insurer you’re hosting on Airbnb, assuming “what they don’t know won’t hurt them.”

The Reality: Insurance fraud. If you file any claim (even unrelated to Airbnb), your insurer will investigate your property use. Discovering undisclosed STR activity gives them grounds to deny all claims and cancel your policy.

The Fix: Notify your homeowners insurer immediately when you start hosting. Some insurers (like Allstate, Farmers, Liberty Mutual) offer endorsements to extend coverage. If your current insurer won’t cover STR activity, switch to an STR-friendly carrier before hosting.

4. Skipping Insurance for Rental Arbitrage

The Mistake: Thinking “I don’t own the home or property, so I don’t need insurance. That’s the landlord’s responsibility.”

The Reality: You are legally liable for guest injuries and property damage as the operator. Your landlord’s insurance doesn’t cover your business activity. Most arbitrage leases REQUIRE proof of insurance naming the landlord as an additional insured.

The Fix: Purchase commercial general liability ($1-2M) and a business renter’s policy that covers furniture, electronics, and property damage beyond AirCover limits. Expect to pay $960-$2,400 annually.

5. Not Reading the Fine Print (Exclusions, Deductibles, Claim Time Limits)

The Mistake: Buying insurance without reviewing what’s actually covered, assuming “insurance is insurance.”

The Reality: Policies vary dramatically. Some exclude pets entirely. Others require claims within 12 hours. Many have $1,000-$5,000 deductibles, meaning small claims aren’t worth filing.

The Fix: Before purchasing, ask these specific questions:

- What is the deductible per claim?

- What are the excluded perils (pets, bed bugs, acts of God)?

- What is the claim reporting window?

- Does it include business interruption?

- Are there coverage limits on specific item categories (electronics, jewelry)?

6. Not Updating Coverage as Your Portfolio Grows

The Mistake: Buying insurance for your first property, then adding 3-5 more properties without updating your policy.

The Reality: Your policy only covers listed properties. Claims on unlisted properties will be denied. You’re also missing portfolio discounts that could save 15-25% on premiums.

The Fix: Notify your insurer every time you add a home or property. Most dedicated STR insurers (Proper, CBIZ) offer portfolio policies with volume discounts. Update annually or whenever your property count changes.

Related guides for Airbnb hosts: See the complete rental arbitrage guide for the full business model, check the startup costs breakdown including insurance budgeting, use the profit calculator to estimate returns after insurance costs, and explore co-host training if you want to manage properties where the owner carries the insurance. For choosing the right market, see our most profitable Airbnb cities ranking and the co-listing agreement template which covers insurance terms between co-hosts and property owners.

Frequently Asked Questions

Does renters insurance cover Airbnb damage?

No. Standard renters insurance policies contain business activity exclusions that automatically void coverage when you engage in short-term rental hosting. The moment you charge a guest to stay, you’re conducting commercial activity, which is explicitly excluded from personal renters insurance policies. If you file a claim related to Airbnb hosting, it will be denied, and your policy may be canceled.

To be covered, you need dedicated short-term rental insurance from providers like Proper Insurance, Safely, or CBIZ, or an endorsement from STR-friendly carriers like Allstate HostAdvantage or Foremost.

Is Airbnb’s AirCover enough protection?

For occasional hosts with low-value properties and minimal financial risk, AirCover may be sufficient. However, AirCover has critical gaps:

- No coverage for lost rental income if your property is damaged and unrentable

- No bed bug coverage ($1,500-$5,000 to treat)

- No natural disaster coverage (floods, hurricanes, earthquakes)

- Very limited pet damage coverage despite Airbnb’s pet-friendly stance

- No coverage for theft of high-value items (jewelry, electronics, collectibles)

For full-time hosts, multi-property operators, or anyone relying on Airbnb income to pay their mortgage, AirCover alone is insufficient. You need supplemental coverage for business interruption, natural disasters, and excluded perils.

How much does Airbnb host insurance cost?

Costs vary based on property value, location, and coverage limits:

- Occasional hosts (<50 nights/year): $250-$750/year with pay-per-booking plans like Safely

- Full-time hosts (1-2 properties): $800-$1,500/year per property with Proper Insurance or Allstate HostAdvantage

- Multi-property professionals (3+ properties): $2,000-$5,000/year for portfolio policies with volume discounts

- Rental arbitrage operators: $960-$2,400/year for commercial general liability plus renter’s policy with business rider

- Luxury properties ($500K+): $1,000-$5,000/year with Liberty Mutual or similar premium carriers

Do I need insurance for rental arbitrage?

Yes, absolutely. Even though you don’t own the home or property, you are legally liable for:

- Guest injuries on the premises

- Damage to the landlord’s property beyond what AirCover covers

- Damage to your furniture, electronics, and improvements you’ve added

- Legal defense if the landlord sues you for property damage or lease violations

Most rental arbitrage lease agreements explicitly require proof of insurance with the landlord named as an additional insured. Operating without insurance can result in immediate lease termination. Expect to pay $960-$2,400 annually for adequate coverage (commercial general liability + renter’s policy with business use rider).

What happens if a guest gets injured at my Airbnb?

If a guest is injured on your property:

Immediate Steps:

- Ensure the guest receives necessary medical attention (call 911 if serious)

- Document the incident (photos of the scene, witness statements, incident report)

- Do NOT admit fault or liability in writing or verbally

- Report the incident to Airbnb within 24 hours

AirCover Protection:

Airbnb’s Host Liability Insurance ($1 million) covers guest bodily injuries and medical expenses. The guest (or their attorney) files a claim against you, and AirCover’s insurance covers:

- Medical bills

- Lost wages

- Pain and suffering (if applicable)

- Legal defense costs if you’re sued

When AirCover Isn’t Enough:

If injuries are severe (permanent disability, death) and result in claims exceeding $1 million, you need additional coverage. This is why hosts with high-value properties or significant assets purchase dedicated STR policies with $2M+ liability limits.

Critical: Never settle or negotiate directly with an injured guest. Always involve Airbnb and your insurance provider immediately.

Does homeowners insurance cover Airbnb?

No, standard homeowners insurance policies do NOT cover Airbnb activity. Like renters insurance, homeowners policies contain business pursuits exclusions that void coverage when you use your home for short-term rental income.

However, some carriers offer endorsements or riders that extend coverage to include STR activity:

- Allstate HostAdvantage: $300-$600/year endorsement

- Farmers/Foremost: Landlord policy with STR rider

- Liberty Mutual: Premium homeowners with STR coverage

If your current homeowners insurer doesn’t offer an STR endorsement, you have two options:

- Switch to an STR-friendly carrier (Proper, Foremost, Liberty Mutual)

- Purchase a separate dedicated STR policy while maintaining your homeowners policy for personal coverage

Critical: Notify your homeowners insurer BEFORE you start hosting. Failure to disclose STR activity is considered insurance fraud and can result in all claims being denied and policy cancellation.

Can my insurance be canceled for Airbnb hosting?

Yes. If your insurance company discovers you’re hosting on Airbnb without disclosing it, they can:

- Cancel your existing policy immediately for material misrepresentation (failing to disclose business use)

- Deny any pending or future claims related to the home or property

- Report the cancellation to insurance databases, making it harder and more expensive to get coverage elsewhere

How Insurers Discover Undisclosed Hosting:

- You file a claim and they investigate the circumstances

- They find your home sharing listing online during routine checks

- A neighbor or guest reports you to the insurer

- Public records (STR permits, business licenses) reveal hosting activity

How to Avoid Cancellation:

Proactively disclose your STR activity to your insurer before you start hosting. If they won’t offer coverage, switch to an STR-friendly carrier. Transparency is always cheaper than dealing with cancellation and denied claims.

What insurance do I need for co-hosting?

If you’re a co-host (managing someone else’s Airbnb property), you need:

Commercial General Liability Insurance ($1-2M)

- Covers your professional liability for property management activities

- Protects you if a guest is injured due to your negligence (e.g., you forgot to fix a broken step)

- Covers legal defense costs if you’re sued

- Costs: $500-$1,200/year depending on number of properties managed

Errors & Omissions Insurance (E&O)

- Covers mistakes in property management (booking errors, miscommunication, failure to perform duties)

- Protects against financial losses the owner suffers due to your errors

- Costs: $400-$800/year

Workers’ Compensation (If You Have Employees)

- Required in most states if you hire cleaners, maintenance staff, or other co-hosts as W-2 employees

- Covers medical expenses and lost wages if an employee is injured on the job

- Costs: Varies by state, typically 1-3% of payroll

Host-Provided Coverage:

Some property owners require co-hosts to be named as additional insureds on their STR policy. Verify this in your co-hosting agreement and get a certificate of insurance confirming your insurance policy coverage.

Want to see how real short-term rental operators handle insurance and other challenges as they build their businesses? Read 10XBNB reviews from actual students who share their complete journey, including how they set up proper coverage from day one.

Disclaimer: This content is for informational purposes only and should not be considered insurance advice. Insurance policies, coverage limits, and premiums vary by state, provider, and individual circumstances. Consult a licensed insurance professional before making insurance decisions. Links to insurance providers are for reference only; 10XBNB does not receive compensation from insurance companies mentioned in this article.

Sources: Airbnb AirCover Terms of Service | National Association of Insurance Commissioners | Airbnb Host Liability Insurance Program Summary | State-specific insurance department websites | Provider documentation from Proper Insurance, Safely, CBIZ, Allstate, Liberty Mutual, and Foremost