Rental arbitrage hosts pay self-employment tax (15.3%) plus income tax on net profit after deductions. You can deduct rent, utilities, furniture, cleaning fees, supplies, and depreciation of assets. If your property qualifies under the IRS short-term rental loophole, losses can offset your W-2 income. This Airbnb tax guide breaks down every deduction, quarterly filing deadline, and tax strategy for rental arbitrage in 2026.

I’m not a CPA, and nothing here is personal tax advice. But after years in the arbitrage business, managing multiple listings across different jurisdictions, dealing with occupancy taxes, service fees, and quarterly estimated payments, I’ve learned exactly what most hosts leave on the table. And it’s a lot.

How Airbnb Income Gets Taxed: The Basics Every Host Must Know

Before we get into deductions, you need to understand the tax structure. Airbnb rental income is taxable. Period. Whether you’re renting one spare bedroom or managing 15 arbitrage units, the IRS expects you to report every dollar of income on your return.

Here’s the part that confuses people: Airbnb reports your gross earnings to the IRS via a Form 1099-K. But the 1099-K is a reporting mechanism, not a tax trigger. You owe taxes on all rental income regardless of whether Airbnb sends you that form.

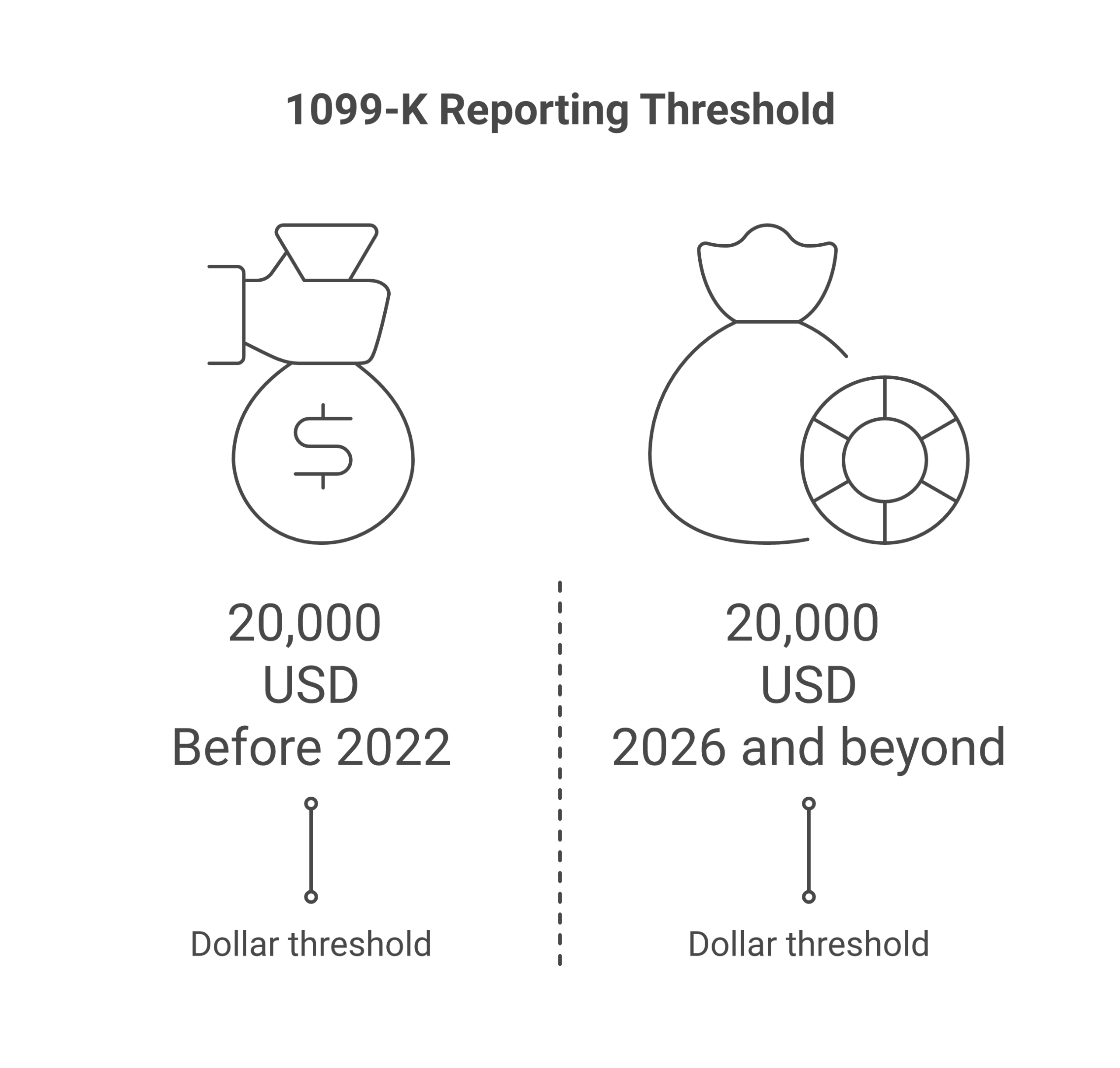

The 1099-K Threshold: What Changed Under the OBBBA

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, permanently reverted the 1099-K reporting threshold back to the pre-2022 standard: $20,000 in gross payments AND more than 200 transactions in a calendar year. Here’s the timeline of how we got here:

| Tax Year | 1099-K Dollar Threshold | Transaction Threshold | What Happened |

|---|---|---|---|

| Before 2022 | $20,000 | 200+ | Original threshold |

| 2022-2023 | $600 (planned) | 1 (planned) | IRS delayed implementation |

| 2024 | $5,000 | Any | Transitional threshold |

| Jan-Jul 2025 | $2,500 | Any | Planned phase-in |

| Jul 2025 onward | $20,000 | 200+ | OBBBA permanently reverted |

What does this mean practically? If you earn less than $20,000 or have fewer than 200 bookings in a year, Airbnb won’t send the IRS a 1099-K for you. But, and I can’t stress this enough, you still owe taxes on every dollar. The form is just paperwork. Your obligation exists whether the form does or not.

Other Tax Forms You’ll Encounter

| Form | What It Reports | 2026 Threshold |

|---|---|---|

| 1099-K | Gross transaction payments from Airbnb | $20,000 + 200 transactions (OBBBA) |

| 1099-MISC | Co-host payments, referral bonuses, other income | $2,000 (increased from $600 by OBBBA) |

| 1099-NEC | Non-employee compensation (contractor co-hosts) | $2,000 (increased from $600 by OBBBA) |

| Schedule C | Your business profit or loss | You file this yourself |

| Schedule E | Rental income (if no substantial services) | You file this yourself |

| Schedule SE | Self-employment tax | Net earnings > $400 |

Schedule C vs. Schedule E: Which One Do You File?

This is a question I get asked constantly in the arbitrage community. The answer depends on the services you provide:

- Schedule C (Business Income) – File this if you provide “substantial services” to guests beyond just renting the space. If you handle cleaning between guests, provide fresh linens, offer check-in assistance, stock amenities, or manage guest communication. That’s substantial services. Most rental arbitrage operators file Schedule C.

- Schedule E (Rental Income) – File this if you’re a passive landlord who simply rents a space with minimal services. Rare for short-term rental hosts.

Why does it matter? Schedule C income is subject to self-employment tax (15.3%) on top of your regular income tax. Schedule E income is not. But Schedule C also opens the door to more aggressive deductions and the qualified business income (QBI) deduction. For most arbitrage hosts, Schedule C is both the correct filing method and the more advantageous one.

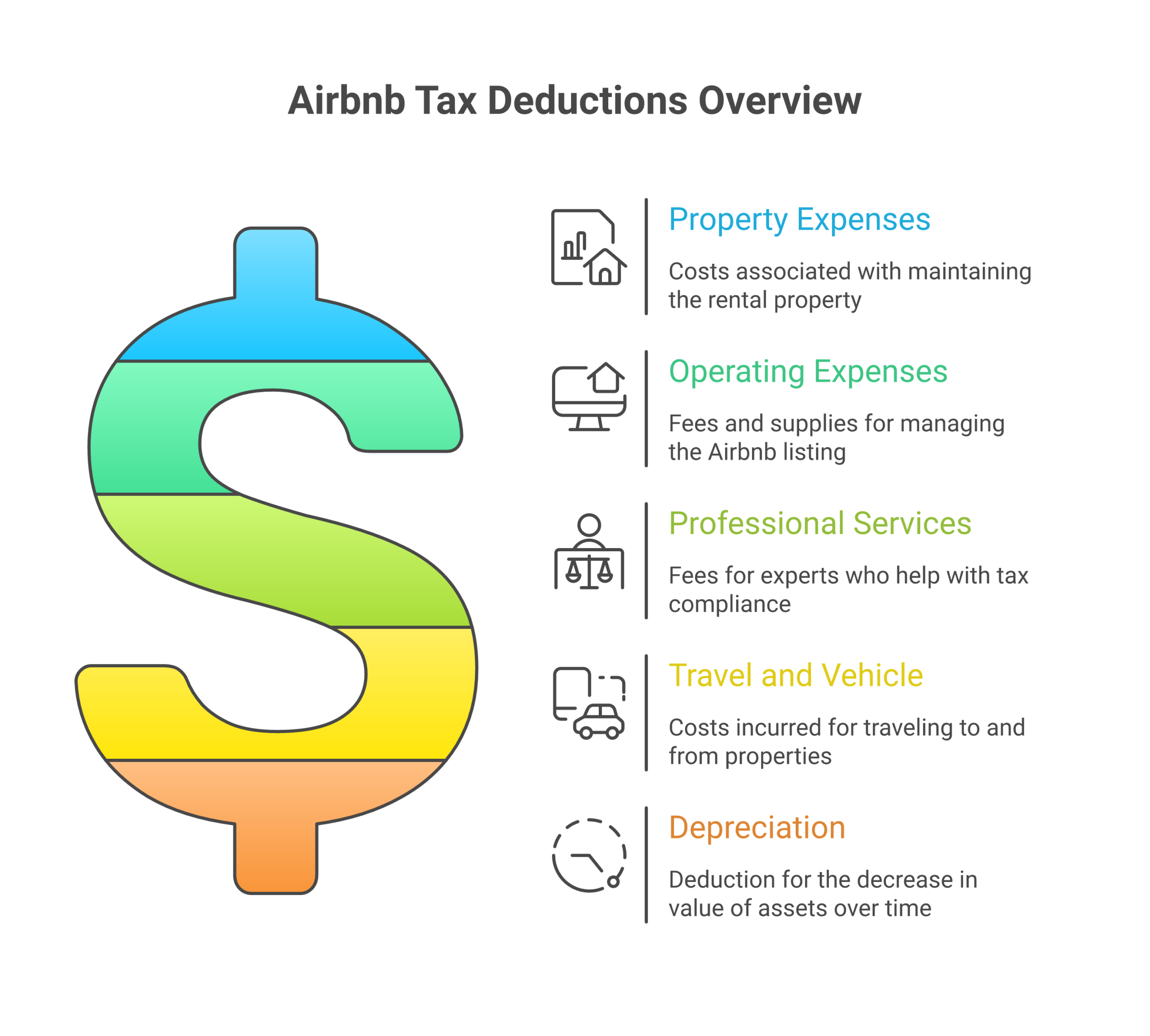

The Complete Deductions Checklist for Rental Arbitrage Hosts

This is where you make or lose thousands of dollars. I’ve talked to arbitrage hosts who missed $8,000-$12,000 in legitimate deductions because they didn’t track expenses properly or didn’t know what qualifies. Here’s everything you can deduct, organized by category.

Property Expenses (Your Biggest Deductions)

| Expense | Deductible? | Notes |

|---|---|---|

| Monthly rent payments | 100% | Your single largest deduction in arbitrage |

| Utilities (electric, gas, water) | 100% if dedicated unit | Prorate if mixed personal/business use |

| Internet/WiFi | 100% if dedicated unit | Essential for guest communication and smart locks |

| Renters insurance | 100% | Plus any supplemental STR insurance |

| Repairs and maintenance | 100% | Plumbing, HVAC, appliance repairs, deduct the year incurred |

| Cleaning between guests | 100% | Whether you hire a cleaner or buy supplies |

| Cleaning supplies and consumables | 100% | Trash bags, paper towels, dish soap, laundry detergent |

| Pest control | 100% | Regular treatments are deductible |

Your rent payment is the cornerstone of rental arbitrage tax strategy. When you’re renting a property at $1,800/month and generating $4,200/month in booking revenue, that $21,600 annual rent is fully deductible against your rental income. This is the same way any business deducts the cost of the space it operates from.

Operating and Platform Expenses

| Expense | Deductible? | Notes |

|---|---|---|

| Airbnb host service fee | 100% | Currently 15.5% under the host-only fee model (effective Oct 2025) |

| Other platform fees (VRBO, Booking.com) | 100% | Service fees from any booking platform |

| Property management software | 100% | Hospitable, Guesty, OwnerRez, etc. |

| Dynamic pricing tools | 100% | PriceLabs, Beyond Pricing, Wheelhouse |

| Professional photography | 100% | Listing photos are a business expense |

| Guest amenities | 100% | Toiletries, coffee, snacks, welcome baskets |

| Furnishings and decor | Depreciated or Section 179 | Items over $2,500 should be depreciated; under $2,500 can use de minimis safe harbor |

| Smart home devices | 100% or depreciated | Smart locks, thermostats, noise monitors |

| Linens and towels | 100% | Replacement linens, mattress protectors, pillow cases |

The Airbnb host service fee changed significantly in late 2025. As of October 27, 2025, Airbnb transitioned most hosts to a 15.5% host-only fee model (replacing the old split-fee where hosts paid 3% and guests paid 14-16.5%). That 15.5% comes straight off your gross booking revenue, and it’s 100% deductible as a business expense. On $60,000 in annual bookings, that’s $9,300 in service fees you can deduct.

Professional Services

- CPA or tax preparer fees – What you pay your accountant to file your return is deductible

- Legal fees – Attorney costs for lease review, LLC formation, or dispute resolution

- Bookkeeping software – QuickBooks, Wave, FreshBooks subscriptions

- Property management company – If you hire a co-host or manager, their fees are deductible

- Business coaching or education – Courses, books, and training directly related to your rental business (this is where programs like rental arbitrage training come in)

Travel and Vehicle Expenses

You can deduct mileage or actual vehicle expenses for trips related to your rental business. This includes:

- Driving to and from your rental properties for inspections, turnovers, or maintenance

- Trips to buy supplies, furniture, or amenities

- Travel to meet potential landlords or view properties

- Attending industry conferences or networking events

For 2026, the IRS standard mileage rate is $0.70 per mile for business use. If you drive 4,000 miles per year for your arbitrage business, that’s a $2,800 deduction just for mileage. Track every trip with an app like MileIQ or Everlance, the IRS requires contemporaneous records.

Home Office Deduction

If you manage your Airbnb business from a dedicated home office (a specific area used exclusively and regularly for business), you can deduct a portion of your home expenses. You have two methods:

- Simplified method: $5 per square foot, up to 300 square feet (maximum $1,500 deduction)

- Regular method: Calculate the percentage of your home used for business and apply it to mortgage/rent, utilities, insurance, repairs

I use the simplified method because it’s clean and audit-proof. No complicated calculations, no receipts required for home expenses. Just measure your office space and multiply.

Business Structure: LLC, S-Corp, or Sole Proprietor?

Your business structure directly impacts how much you pay in taxes. Here’s the breakdown for arbitrage hosts:

Sole Proprietorship (Default)

If you haven’t formed a separate entity, you’re a sole proprietor by default. You report income and expenses on Schedule C. Simple, but no liability protection and you pay self-employment tax on all net income.

Single-Member LLC

An LLC for your Airbnb business provides liability protection but doesn’t change your tax situation, the IRS treats a single-member LLC as a “disregarded entity” and you still file Schedule C. The value is legal protection, not tax savings. If a guest slips and sues, the LLC shields your personal assets.

S-Corporation Election

This is where it gets interesting. Once your net profit exceeds roughly $40,000-$50,000, an S-Corp election can save you thousands in self-employment tax. Here’s an example:

| Scenario | Sole Prop / LLC | S-Corp |

|---|---|---|

| Net profit | $80,000 | $80,000 |

| Reasonable salary | N/A | $45,000 |

| Distribution (not subject to SE tax) | N/A | $35,000 |

| Self-employment tax (15.3%) | $12,240 | $6,885 (on salary only) |

| SE tax savings | – | $5,355 |

The S-Corp adds complexity, you’ll need payroll, W-2s, and quarterly filings. But if you’re clearing $80,000+ net across your properties, the $5,000+ annual savings justifies the extra paperwork. Talk to a CPA before making this election. Your Airbnb business plan should factor in entity structure from day one.

The Short-Term Rental Tax Loophole: Bonus Depreciation + Material Participation

This is the most valuable tax strategy in short term rentals (also called short-term rentals), and the OBBBA just made it dramatically more powerful. Here’s how it works.

What Is the STR Tax Loophole?

Normally, rental losses are “passive”. They can only offset other passive income, not your W-2 salary. But short-term rentals have a special carve-out. If your average guest stay is 7 days or less AND you materially participate in the management, the IRS classifies your rental as a non-passive activity. That means losses from depreciation can offset your regular income, including a W-2 job.

For arbitrage operators, the 7-day rule is almost always satisfied. Your average Airbnb booking is typically 2-4 nights. The material participation requirement is the one you need to document carefully.

Material Participation: The 7 IRS Tests

You need to pass at least ONE of these seven tests for each property:

- 500-hour test: You participate in the activity for more than 500 hours during the tax year

- Substantially all test: Your participation constitutes substantially all of the participation by any individual

- 100-hour/most participation test: You participate more than 100 hours, and no one else participates more than you

- Significant participation test: You participate in multiple activities totaling more than 500 hours

- 5-of-10-year test: You materially participated in any 5 of the prior 10 tax years

- Personal service activity test: The activity is a personal service activity and you materially participated in any 3 prior years

- Facts and circumstances test: You participate on a regular, continuous, and substantial basis for more than 100 hours

Most arbitrage hosts qualify under Test 1 (500 hours) or Test 3 (100 hours + more than anyone else). Keep a contemporaneous log. I use a simple spreadsheet with the date, hours, and description of what I did. Guest communication, pricing adjustments, coordinating cleaners, property inspections, bookkeeping. It all counts.

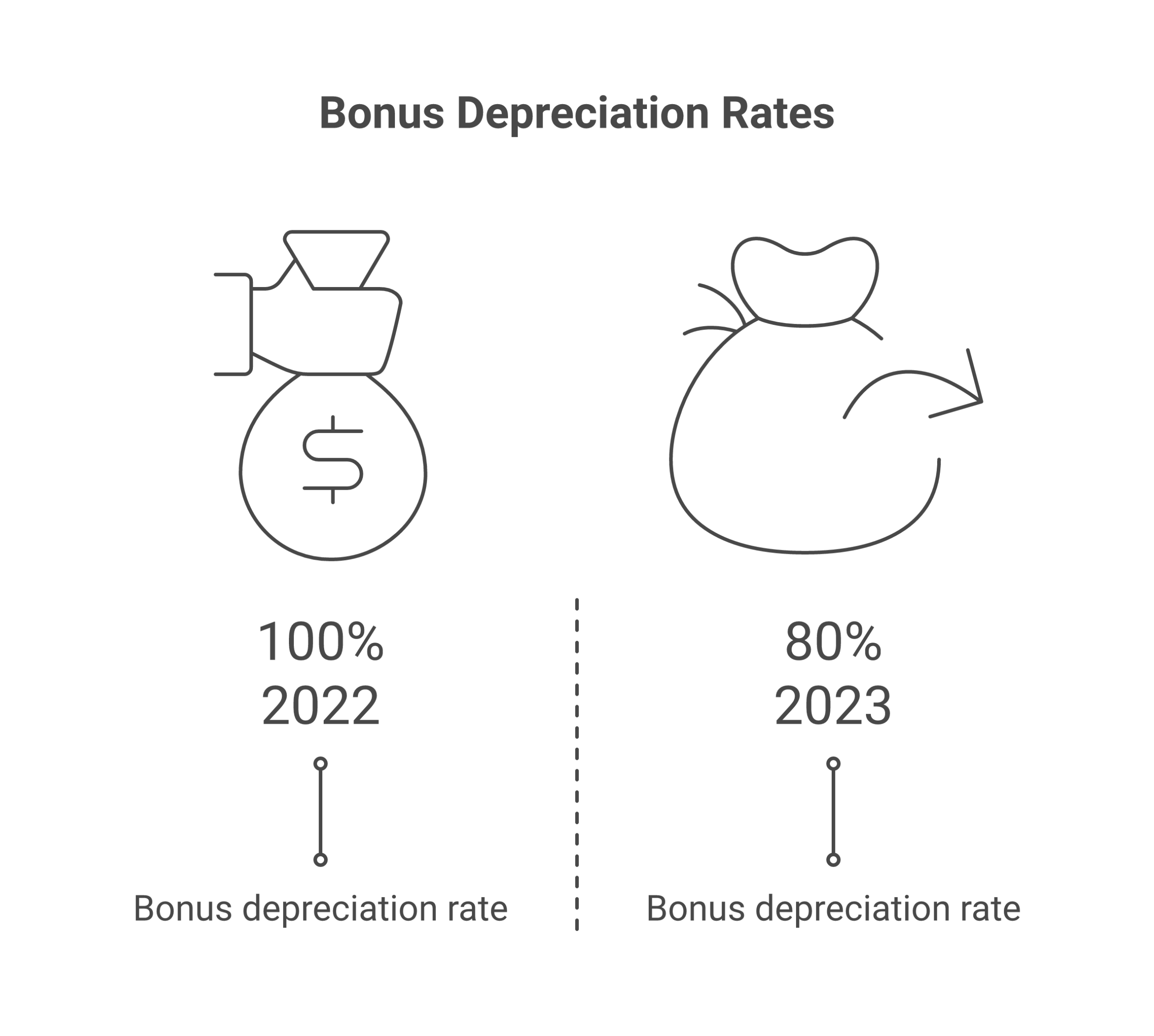

100% Bonus Depreciation Is Back (Thanks to OBBBA)

The OBBBA permanently restored 100% bonus depreciation for qualified property placed in service after January 19, 2025. Before this law passed, bonus depreciation was phasing out:

| Year | Bonus Depreciation Rate |

|---|---|

| 2022 | 100% |

| 2023 | 80% |

| 2024 | 60% |

| Jan 1-19, 2025 | 40% |

| After Jan 20, 2025 | 100% (permanent, OBBBA) |

This applies to assets with a recovery period of 20 years or less: furniture, appliances, flooring, landscaping, certain improvements. Not the building structure itself (that’s 27.5-year residential property). But a cost segregation study can reclassify 20-40% of a property’s value into shorter-lived categories that qualify for bonus depreciation.

How This Works for Arbitrage Hosts

In a typical rental arbitrage setup, you don’t own the building. So you can’t depreciate the structure. But you CAN depreciate (and bonus depreciate) everything you put INTO the property:

- Furniture (7-year property), couches, beds, dressers, dining tables

- Appliances (5-year property), washer/dryer, dishwasher, microwave

- Electronics (5-year property), TVs, smart speakers, noise monitors

- Leasehold improvements (15-year property), flooring upgrades, lighting fixtures, built-in shelving

With 100% bonus depreciation, you deduct the full cost in year one. If you furnish a new unit for $12,000, you write off $12,000 against your income that same year instead of spreading it over 5-7 years. Across multiple properties, this creates massive paper losses that offset your active income.

Occupancy Taxes and Local Tax Obligations

This is the area where I see hosts get blindsided. Federal income tax is one thing. But state and local taxes add layers of complexity that vary wildly by jurisdiction.

Occupancy Taxes (Transient Occupancy Tax / Hotel Tax)

Most cities and counties impose an occupancy tax on short-term rentals, the same way they tax hotel stays. Rates range from 2% to 15%+ depending on your jurisdiction. The good news: Airbnb automatically collects and remits occupancy taxes on your behalf in most major markets. They handle the calculation, collection from guests, and payment to tax authorities.

But “most” isn’t “all.” Check your local laws. If Airbnb doesn’t collect in your jurisdiction, you’re responsible for:

- Registering for a tax permit with your local tax authority

- Collecting the tax from guests (added to the nightly rate or listed as a separate fee)

- Filing periodic returns and remitting payment (monthly, quarterly, or annually)

Failing to collect and remit required occupancy taxes can result in back taxes, penalties, and interest assessed against you personally, even if you didn’t know you were supposed to collect.

State Income Tax

Most states tax your rental income the same way the federal government does. If you operate in a state with income tax, you’ll file a state return reporting your Airbnb business income. Some states also require estimated quarterly payments if your tax liability exceeds a threshold (typically $500-$1,000).

If you operate properties in multiple states, you may owe income tax in each state where you have a listing. This is especially relevant for arbitrage hosts expanding to multiple cities across state lines.

Sales Tax

Some states treat short-term rentals the same way as hotel rooms for sales tax purposes. In these jurisdictions, you may need to collect state and/or local sales tax on top of occupancy taxes. Again, Airbnb handles this automatically in many places, check your Airbnb tax settings to see what’s being collected on your behalf.

Business License and Permit Fees

Many cities require a business license or short-term rental permit to operate legally. These fees, typically $50-$500 per year, are 100% deductible as business expenses. Don’t skip the permit to save money. The fines for operating without one are 10-50x the permit cost in most jurisdictions.

Quarterly Estimated Tax Payments: Don’t Get Penalized

If you expect to owe $1,000 or more in federal taxes for the year (after subtracting withholding and credits), you’re required to make quarterly estimated payments. Miss them and the IRS charges an underpayment penalty. It’s essentially interest on money you should have paid earlier.

2026 Quarterly Payment Deadlines

| Quarter | Income Period | Payment Due |

|---|---|---|

| Q1 | January 1 – March 31 | April 15, 2026 |

| Q2 | April 1 – May 31 | June 15, 2026 |

| Q3 | June 1 – August 31 | September 15, 2026 |

| Q4 | September 1 – December 31 | January 15, 2027 |

How to Calculate Your Estimated Payments

There are two safe harbor methods to avoid underpayment penalties:

- 100% of prior year tax: Pay at least 100% of what you owed last year, divided into four equal payments (110% if your AGI was over $150,000)

- 90% of current year tax: Pay at least 90% of what you’ll owe this year

I use method 1 because it’s predictable. Take last year’s total tax liability, divide by 4, and pay that amount each quarter. If your business is growing and you’ll owe significantly more this year, adjust upward to avoid a surprise bill in April.

Use IRS Form 1040-ES to calculate and submit payments. You can pay online through IRS Direct Pay or EFTPS.

The Qualified Business Income (QBI) Deduction

The OBBBA made the QBI deduction permanent. This is huge for arbitrage operators. If you qualify, you can deduct the maximum amount of 20% of your qualified business income from your taxable income. On $60,000 in net profit, that’s a $12,000 deduction, potentially saving you $2,640-$4,440 depending on your tax bracket.

Do Arbitrage Hosts Qualify for QBI?

Yes, in most cases. The QBI deduction applies to pass-through businesses (sole proprietorships, partnerships, S-Corps, LLCs). Your rental arbitrage income reported on Schedule C qualifies as long as:

- Your taxable income is below the threshold ($191,950 single / $383,900 married filing jointly for 2026)

- The income comes from a qualified trade or business

- You’re not in a “specified service trade or business” (rental operations generally aren’t)

Above the income threshold, the deduction phases out and gets more complicated. But for most hosts building their first few arbitrage units, the full 20% deduction is available.

Record-Keeping: What the IRS Actually Wants to See

If you get audited, and arbitrage operators do get audited because the business model raises questions. Your records are your defense. Here’s what to keep and how to organize it.

The Non-Negotiable Records

- Booking confirmations from every reservation (Airbnb provides these in your transaction history)

- Bank statements showing Airbnb payouts and business expenses paid

- Receipts for every deductible expense – digital is fine, the IRS accepts photos and PDFs

- Lease agreements for every property (proves your rent expense)

- Mileage log with date, destination, purpose, and miles driven

- Material participation log with date, hours, and activity description (critical for the STR loophole)

- Depreciation schedules listing every asset, purchase date, cost, and useful life

- 1099 forms received from Airbnb and any other platforms

How Long to Keep Records

The IRS can audit you for up to 3 years from the date you file (6 years if they suspect underreporting of income by more than 25%). Keep all tax-related records for a minimum of 7 years. Digital storage is fine. You need easy access to everything. I use Google Drive with a folder structure organized by year, then by property.

Separate Business Bank Account

Open a dedicated bank account for your Airbnb business. Don’t commingle personal and business funds. This isn’t just organizational. It protects your LLC liability shield and makes record-keeping dramatically easier. Every deposit is business income. Every payment from this account is a business expense. Clean, simple, audit-proof.

8 Common Tax Mistakes Arbitrage Hosts Make

After working with dozens of arbitrage operators, these are the mistakes I see most often:

1. Not Tracking Expenses From Day One

I’ve talked to hosts who ran their business for 18 months before they realized they needed to track expenses for taxes. By then, they’d lost thousands in deductions because they had no receipts. Start tracking the day you sign your first lease, before you even list the property.

2. Forgetting to Deduct the Airbnb Service Fee

Airbnb’s 15.5% host service fee is automatically deducted from your payouts. Because you never “see” this money, many hosts forget to claim it as a deduction. It’s on your 1099-K (which reports gross earnings before fees) but not in your bank deposits. You’re paid the net amount, but taxed on the gross. So you must deduct that fee to avoid paying taxes on money you never received.

3. Missing the Section 199A (QBI) Deduction

The 20% QBI deduction is free money that many hosts (and some CPAs who don’t specialize in rentals) overlook. Make sure your tax preparer knows about your qualification.

4. Not Making Quarterly Estimated Payments

Underpayment penalties are avoidable and frustrating. If you owe more taxes in April than you expected, the IRS penalizes you for not paying throughout the year. Set calendar reminders for the four quarterly deadlines.

5. Failing to Separate Personal and Business Use

If you ever use an arbitrage property for personal stays, you must prorate your expenses. The IRS counts personal use days against your business deductions. For example, if you stay in one of your units for 10 days out of 365, you reduce your deductions by about 2.7%. Most arbitrage operators avoid this entirely by never using their units personally, which keeps the math clean and deductions at 100%.

6. Depreciating Instead of Expensing (or Vice Versa)

Items under $2,500 can be expensed immediately under the de minimis safe harbor rule. Items over $2,500 should be depreciated. Mixing these up either understates your current-year deductions (if you depreciate a $200 coffee maker over 5 years) or overstates them (if you expense a $4,000 couch in year one without using Section 179 or bonus depreciation properly).

7. Ignoring State and Local Tax Obligations

Federal taxes get all the attention, but your state and local taxes can blindside you. Register for occupancy tax permits. Check if Airbnb collects on your behalf. File state returns in every state where you operate. The penalties for non-compliance at the local level are often more aggressive than federal ones.

8. Using a Non-Specialist CPA

A general CPA who does primarily W-2 returns will miss rental-specific strategies. Find a CPA or enrolled agent who specializes in real estate or short-term rentals. The STR tax loophole, cost segregation, material participation logging, S-Corp elections. These are specialized strategies that a generalist won’t proactively suggest. The right CPA will save you multiples of their fee.

When to Hire a CPA vs. DIY

Here’s my honest take on when you need professional help versus when you can handle taxes yourself:

| Situation | DIY? | Hire a CPA? |

|---|---|---|

| 1 property, straightforward expenses | Yes, TurboTax or FreeTaxUSA handles this | Optional |

| 2-5 properties, multiple states | Risky | Recommended |

| Net profit over $50K | No | Yes, S-Corp evaluation needed |

| Using the STR tax loophole | No | Yes, material participation documentation matters |

| Cost segregation study | No | Yes, need CPA + cost seg specialist |

| Multi-member LLC or partnership | No | Yes, partnership returns are complex |

A good STR-specialized CPA costs $500-$2,000 per year depending on complexity. If they identify even one strategy you’d miss, like the QBI deduction on $60,000 income ($12,000 deduction saving you $2,640+), they pay for themselves immediately.

Airbnb Service Fees: What You Pay and What You Deduct

Understanding how much Airbnb actually takes from each booking is critical for accurate tax reporting. Here’s the current fee structure:

Host-Only Fee Model (Current as of October 2025)

Most hosts now pay a flat 15.5% host service fee on the booking subtotal (nightly rate + any host-set fees like cleaning, minus taxes). Guests see a single all-in price with no separate “Airbnb service fee” line item.

Previously, Airbnb used a split-fee model where hosts paid 3% and guests paid 14-16.5%. The new model shifts the full fee to the host but makes pricing more transparent to guests, which Airbnb argues increases booking conversion.

Tax Treatment of Service Fees

Once your tax information is submitted and verification successful in the Airbnb dashboard, your 1099-K reports gross booking revenue, the full amount the guest paid before Airbnb’s cut. But your bank account only receives the net payout after the 15.5% fee. You MUST deduct the service fee as a business expense to avoid paying income tax on money Airbnb kept.

For example, on a $200/night booking for 3 nights:

- Gross revenue (on 1099-K): $600

- Airbnb service fee (15.5%): $93

- Your payout: $507

- Deductible fee expense: $93

Over a year with $60,000 in gross bookings, that’s $9,300 in deductible service fees. Don’t leave that on the table.

Real Tax Scenario: Sample Schedule C for an Arbitrage Host

Let me walk through a realistic example. This is loosely based on numbers I’ve seen from hosts running 3 arbitrage units in a mid-sized city:

| Line Item | Amount |

|---|---|

| Gross Income (3 units) | $144,000 |

| Airbnb service fees (15.5%) | ($22,320) |

| Rent payments (3 × $1,800/mo) | ($64,800) |

| Utilities (3 units) | ($7,200) |

| Cleaning (between guests) | ($9,600) |

| Internet (3 units) | ($2,160) |

| Insurance (3 units) | ($3,600) |

| Supplies and amenities | ($2,400) |

| Software subscriptions | ($1,200) |

| Repairs and maintenance | ($1,800) |

| Mileage (3,500 mi × $0.70) | ($2,450) |

| Professional photography | ($900) |

| CPA fees | ($1,200) |

| Depreciation (furniture, appliances) | ($8,000) |

| Home office (simplified) | ($1,500) |

| Total Expenses | ($129,130) |

| Net Profit (Schedule C) | $14,870 |

On $144,000 in gross revenue, this host’s taxable business income is only $14,870 after legitimate deductions. That’s the difference between owing $30,000+ in taxes and owing a fraction of that. The QBI deduction would reduce the taxable amount by another $2,974 (20% × $14,870).

And yes, if this host qualifies for the STR tax loophole and takes bonus depreciation on $12,000 in new furnishings, the net profit drops even further. Some hosts in their first year of operations actually show a net loss on Schedule C, which offsets income from other sources.

Tax Planning Calendar for Arbitrage Hosts

Don’t wait until April to think about taxes. Here’s a month-by-month calendar to keep you on track:

January

- Review prior year income and expenses

- Gather all 1099 forms from Airbnb and other platforms

- Organize receipts and records for the prior tax year

- Pay Q4 estimated tax (due January 15)

February, March

- Meet with your CPA to prepare your return

- Review depreciation schedules for accuracy

- File your return early if expecting a refund

April

- File your tax return or extension by April 15

- Pay Q1 estimated tax for the current year (due April 15)

- Review your estimated payment amount for accuracy

June

- Pay Q2 estimated tax (due June 15)

- Mid-year financial review, are your projections on track?

September

- Pay Q3 estimated tax (due September 15)

- If you filed an extension, prepare your return (October 15 deadline)

- Start planning year-end tax strategies (asset purchases, S-Corp evaluation for next year)

October, December

- Make any planned asset purchases for bonus depreciation (must be “placed in service” before Dec 31)

- Review whether an S-Corp election makes sense for next year (deadline: March 15 of the following year)

- Verify occupancy tax compliance for all jurisdictions

- Close your books for the year

Special Situations for Arbitrage Hosts

Operating in Multiple Jurisdictions

If you run arbitrage units in different cities or states, each jurisdiction has its own rules. You may need separate business licenses, occupancy tax registrations, and state income tax filings. This is where the right CPA earns their fee, navigating multi-state filing requirements is genuinely complicated.

The good news: expenses are allocated to the jurisdiction where they occur. Your rent for a Nashville unit is deducted against Nashville income. Your Dallas expenses go against Dallas revenue. Keep your books organized by property and the allocation sorts itself out.

When Your Landlord Doesn’t Know

Some arbitrage operators don’t disclose their subletting arrangement to landlords. I’m not here to judge. But from a tax perspective, it doesn’t matter. Your tax obligations exist regardless of your lease situation. You still report income, claim deductions, and pay taxes the same way. The IRS doesn’t check whether your landlord approved your Airbnb listing. They check whether you reported your income.

Vacation Rental Losses and the “Hobby” Rule

If your arbitrage expenses exceed your income, you report a business loss on Schedule C. That loss can offset other income on your personal return (like a W-2 job), reducing your total tax liability. But there’s a catch: if you report losses for multiple consecutive years, the IRS may challenge your “profit motive” and reclassify your activity as a hobby.

Hobby income is still taxable, but hobby expenses aren’t deductible. To protect yourself, keep records showing you’re actively trying to be profitable: pricing optimization, marketing efforts, scaling plans, revenue growth tracking. The IRS uses a facts-and-circumstances test, but the general guideline is that you should show a profit in at least 3 out of 5 years.

The 14-Day Rule (Augusta Rule)

This rarely applies to arbitrage operators, but it’s worth knowing: if you rent a property for fewer than 15 days per year, you don’t have to report the rental income at all. It’s completely tax-free. This is called the “Augusta Rule” (named after homeowners who rent their houses during the Masters golf tournament). For most arbitrage operators renting year-round, this rule is irrelevant. But if you have a vacation property you occasionally list on Airbnb, it could apply.

How Much Should You Set Aside for Taxes?

A question I hear constantly from hosts who are just starting their Airbnb business: how much of each booking should go to taxes?

The honest answer: it depends on your total income, filing status, and deductions. But a safe rule of thumb for arbitrage operators:

- 25-30% of net profit (after deductions) for federal income tax + self-employment tax

- Add 5-10% if your state has an income tax

- So roughly 30-40% of net profit set aside in a separate savings account

I transfer 30% of every Airbnb payout into a dedicated “tax savings” account the day it hits my bank. By the time quarterly payments roll around, the money is already there. No scrambling, no surprises.

Want to estimate your actual profit before taxes? Use the Airbnb profit calculator to model different scenarios.

Financing and Tax Implications

If you’re using DSCR loans or other financing to fund your arbitrage expansion, the interest on those loans is deductible as a business expense. This applies to:

- Credit card interest on business purchases (furnishings, supplies)

- Personal loan interest if the funds were used for your rental business

- Line of credit interest for business operating expenses

Keep documentation showing that borrowed funds were used exclusively for your rental business. Commingling personal and business debt makes it nearly impossible to justify the deduction in an audit.

Frequently Asked Questions

Do I owe taxes on Airbnb income if I didn’t receive a 1099-K?

Yes. You owe taxes on all rental income regardless of whether Airbnb sends you a 1099-K. The $20,000/200-transaction threshold (OBBBA) only determines when Airbnb reports to the IRS. It doesn’t affect your tax obligation. Report every dollar.

Can I deduct my rent if I’m doing rental arbitrage?

Yes. Your monthly rent payment to the landlord is 100% deductible as a business expense when the property is used exclusively for short-term rentals. This is typically the largest single deduction for arbitrage operators.

What’s the difference between repairs and improvements?

Repairs maintain property condition (fixing a leaky faucet, patching drywall, replacing a broken door handle) and are fully deductible in the year paid. Improvements add value or extend the useful life (new flooring, kitchen renovation, bathroom upgrade) and must be depreciated over their useful life. The distinction matters because repairs give you an immediate deduction while improvements spread the deduction over years.

Is Airbnb cleaning income taxable for my cleaners?

If you pay a cleaning person more than $2,000 in a year (OBBBA threshold), you’ll need to issue them a 1099-NEC. Their income is taxable to them. Your payment to them is deductible to you. Keep records of every payment.

Can I deduct furniture I already owned?

If you convert personal furniture to business use, you can depreciate it. But based on its fair market value at the time of conversion, not what you originally paid. A couch you bought for $2,000 three years ago might have a fair market value of $800 when you put it into an Airbnb unit. You’d depreciate the $800.

What happens if I get audited?

The IRS will request documentation for your income and deductions. Having organized records (booking confirmations, receipts, lease agreements, mileage logs, material participation logs) is your best defense. Most audits are resolved by correspondence. You mail in documentation and the IRS reviews it. If you’ve been honest and thorough with your records, an audit is stressful but survivable.

Can my arbitrage losses offset my W-2 income?

Only if you qualify for the short-term rental tax loophole (average guest stay 7 days or less + material participation). If you meet both requirements, your rental is classified as non-passive, and losses, especially from bonus depreciation, can offset your W-2 income. If you don’t meet the requirements, rental losses are passive and can only offset passive income.

Do I need to collect sales tax from guests?

It depends on your jurisdiction. In markets where Airbnb automatically collects and remits occupancy and sales taxes on your behalf, no. It’s handled. In jurisdictions where Airbnb doesn’t collect, you may need to register for a sales tax permit, charge guests the tax, and remit it yourself. Check your Airbnb tax settings to see what’s being collected in your area.

How does the OBBBA affect my taxes as an Airbnb host?

The One Big Beautiful Bill Act (signed July 4, 2025) made several changes that benefit Airbnb hosts: it permanently restored 100% bonus depreciation for assets placed in service after January 19, 2025; it made the 20% QBI deduction permanent; it reverted the 1099-K threshold to $20,000 + 200 transactions; and it increased the 1099-MISC and 1099-NEC thresholds to $2,000. All of these changes are favorable for short-term rental operators.