<! - wp:paragraph - >

Fix to rent loans are a powerful tool for real estate investors looking to purchase, renovate, and rent out properties to generate steady rental income. Unlike traditional fix and flip loans, which focus on quick renovations and sales, fix to rent loans are designed for investors who aim to hold properties long-term and build a rental portfolio. This Airbnb Tips article leaps into the world of fix to rent loans, answering key questions and offering unique insights to help you use financing for your next investment property. Whether you’re a seasoned investor or just starting with platforms like 10XBNB, understanding these loans can transform your approach to rentals.

<! - /wp:paragraph - >

<! - wp:heading - >

What is a Fix to Rent Loan?

<! - /wp:heading - >

<! - wp:paragraph - >

A fix to rent loan is a specialized financing product that allows investors to purchase a property, cover rehab costs, and transition the property into a long-term rental. These rent loans combine the flexibility of a fix and flip loan with the stability of a long-term rental loan. The loan typically covers the purchase price, necessary repairs, and sometimes even initial holding costs until the property is stabilized and generating rental income.

<! - /wp:paragraph - >

<! - wp:paragraph - >

For example, 10XBNB investors often use fix to rent loans to acquire distressed multifamily properties or single-family homes, renovate them to meet market standards, and then rent them out for consistent cash flow. The goal is to create stabilized properties that produce reliable income, which can later be refinanced into a conventional loan for better terms.

<! - /wp:paragraph - >

<! - wp:paragraph - >

Pro Tip: When evaluating fix to rent loans, prioritize lenders who understand the rental market and offer flexible terms, such as no prepayment penalty, to allow for early refinancing once the property is stabilized.

<! - /wp:paragraph - >

<! - wp:image {"id":2688,"sizeSlug":"large","linkDestination":"none"} - >

<! - /wp:image - >

<! - wp:heading - >

How Fix to Rent Loans Differ from Fix and Flip Loans

<! - /wp:heading - >

<! - wp:paragraph - >

While both fix to rent and fix and flip loans fund property purchases and renovations, their purposes diverge significantly. Fix and flip loans are short-term loans tailored for flip investors who renovate and sell properties quickly for a profit. In contrast, fix to rent loans cater to investors focused on long-term rentals, offering longer repayment terms and the ability to refinance into a fixed-rate mortgage after renovations.

<! - /wp:paragraph - >

<! - wp:paragraph - >

Here’s a quick breakdown:

<! - /wp:paragraph - >

<! - wp:list - >

- <! - wp:list-item - >

- Fix to Rent Loans:<! - wp:list - >

- <! - wp:list-item - >

- Purpose: Purchase, rehab, and rent.

- Loan Term: Short-term (6-24 months) with options to refinance.

- Focus: Generating rental income.

- Ideal for: Multifamily properties, single-family rentals, or commercial properties.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

- Fix and Flip Loans:<! - wp:list - >

- <! - wp:list-item - >

- Purpose: Purchase, rehab, and sell.

- Loan Term: Short-term (6-18 months).

- Focus: Quick sale for profit.

- Ideal for: Properties with high after-repair value.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - wp:paragraph - >

For investors using 10XBNB’s strategies, fix to rent loans align perfectly with the goal of building wealth through rentals. Learn more about short-term rental investments at 10XBNB’s guide to short-term rentals.

<! - /wp:paragraph - >

<! - wp:heading - >

Benefits of Fix to Rent Loans

<! - /wp:heading - >

<! - wp:paragraph - >

Fix to rent loans offer several advantages for real estate investors:

<! - /wp:paragraph - >

<! - wp:list {"ordered":true} - >

- <! - wp:list-item - >

- Complete Financing: Covers purchase price, rehab costs, and sometimes holding costs.

- Flexibility: Allows investors to stabilize the property before refinancing into a long-term rental loan.

- Cash Flow Potential: Enables investors to generate rental income while building equity.

- Scalability: Ideal for growing a rental portfolio with multiple properties.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - wp:paragraph - >

However, there are challenges to consider:

<! - /wp:paragraph - >

<! - wp:list - >

- <! - wp:list-item - >

- Higher Interest Rates: Compared to conventional loans, fix to rent loans often have higher rates due to their short-term nature.

- Credit Requirements: Lenders may require decent credit scores, though some offer leniency for experienced investors.

- Origination Fees: These can increase the overall cost of the loan.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - wp:heading - >

How Can I Borrow Money to Pay Rent?

<! - /wp:heading - >

<! - wp:paragraph - >

For investors needing funds to cover rent or stabilize a property during the rehab process, fix to rent loans can provide the necessary cash. These loans are structured to finance the entire project, including renovations and initial holding costs, until the property generates rental income. Here’s how the process works:

<! - /wp:paragraph - >

<! - wp:list {"ordered":true} - >

- <! - wp:list-item - >

- Identify the Property: Find a property with strong rental potential, such as a distressed home or multifamily unit.

- Secure the Loan: Work with a lender specializing in fix to rent loans. Provide details on the purchase price, rehab budget, and expected rental income.

- Complete Renovations: Use loan funds to make necessary repairs and upgrades to maximize rent potential.

- Stabilize the Property: Lease the property to tenants to generate rental income.

- Refinance: Transition to a long-term rental loan or conventional loan to lower interest rates and secure fixed-rate terms.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - wp:paragraph - >

For those starting with limited capital, 10XBNB offers strategies to enter the rental market with minimal upfront investment. Check out their guide on Airbnb with no money for creative financing tips.

<! - /wp:paragraph - >

<! - wp:paragraph - >

Pro Tip: Use a mid-term rental calculator to estimate cash flow and ensure your property will generate sufficient rental income to cover loan payments and operational costs.

<! - /wp:paragraph - >

<! - wp:heading - >

What Credit Score Do You Need for a Fix and Flip Loan?

<! - /wp:heading - >

<! - wp:paragraph - >

While fix to rent loans and fix and flip loans differ, their credit requirements can overlap, especially for lenders offering both products. For fix and flip loans, most lenders require a credit score of 620-680, though some hard money lenders may go as low as 600 for experienced flip investors. Fix to rent loans often have similar requirements, as lenders assess the borrower’s ability to manage the rehab process and stabilize the property.

<! - /wp:paragraph - >

<! - wp:paragraph - >

Factors that influence credit requirements include:

<! - /wp:paragraph - >

<! - wp:list - >

- <! - wp:list-item - >

- Experience: Seasoned investors with a track record of successful projects may qualify with lower credit scores.

- Property Type: Multifamily properties or commercial properties may require stricter credit checks due to higher loan amounts.

- Loan-to-Value Ratio: Lenders may be more lenient if the loan amount is a small percentage of the after-repair value.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - wp:paragraph - >

To improve your chances of qualifying, maintain a strong credit profile and prepare a detailed rehab budget. If your credit is a concern, consider partnering with a co-borrower or exploring hard money loans, which prioritize property potential over credit.

<! - /wp:paragraph - >

<! - wp:heading - >

What is a Fix and Hold Loan?

<! - /wp:heading - >

<! - wp:paragraph - >

A fix and hold loan is another term for a fix to rent loan. These loans are ideal for investors who want to fix a property, rent it out, and either refinance or hold it as part of their rental portfolio. The “hold” aspect distinguishes it from a flip loan, as the goal is to generate ongoing cash flow rather than a quick sale.

<! - /wp:paragraph - >

<! - wp:paragraph - >

For example, an investor might use a fix to rent loan to acquire a distressed property, complete renovations, and lease it to tenants. Once the property is stabilized, they can refinance into a DSCR loan (Debt Service Coverage Ratio loan), which evaluates the property’s rental income to determine loan eligibility. This strategy is particularly effective for 10XBNB investors focusing on short-term or mid-term rentals.

<! - /wp:paragraph - >

<! - wp:heading - >

Types of Fix to Rent Loans

<! - /wp:heading - >

<! - wp:paragraph - >

Several loan types fall under the fix to rent umbrella, each with unique features:

<! - /wp:paragraph - >

<! - wp:list {"ordered":true} - >

- <! - wp:list-item - >

- Hard Money Loans:<! - wp:list - >

- <! - wp:list-item - >

- Best for: Investors with lower credit scores or urgent financing needs.

- Pros: Fast approval, flexible terms.

- Cons: Higher interest rates, shorter terms.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

- DSCR Loans:<! - wp:list - >

- <! - wp:list-item - >

- Best for: Refinancing stabilized properties with strong rental income.

- Pros: Based on property income, not personal credit.

- Cons: Requires proof of consistent rental income.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

- FHA Loans:<! - wp:list - >

- <! - wp:list-item - >

- Best for: Owner-occupants or small multifamily properties.

- Pros: Low down payment, fixed rates.

- Cons: Strict occupancy requirements.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

- Conventional Loans:<! - wp:list - >

- <! - wp:list-item - >

- Best for: Refinancing after stabilization.

- Pros: Lower interest rates, long-term stability.

- Cons: Stringent credit and income requirements.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - wp:heading - >

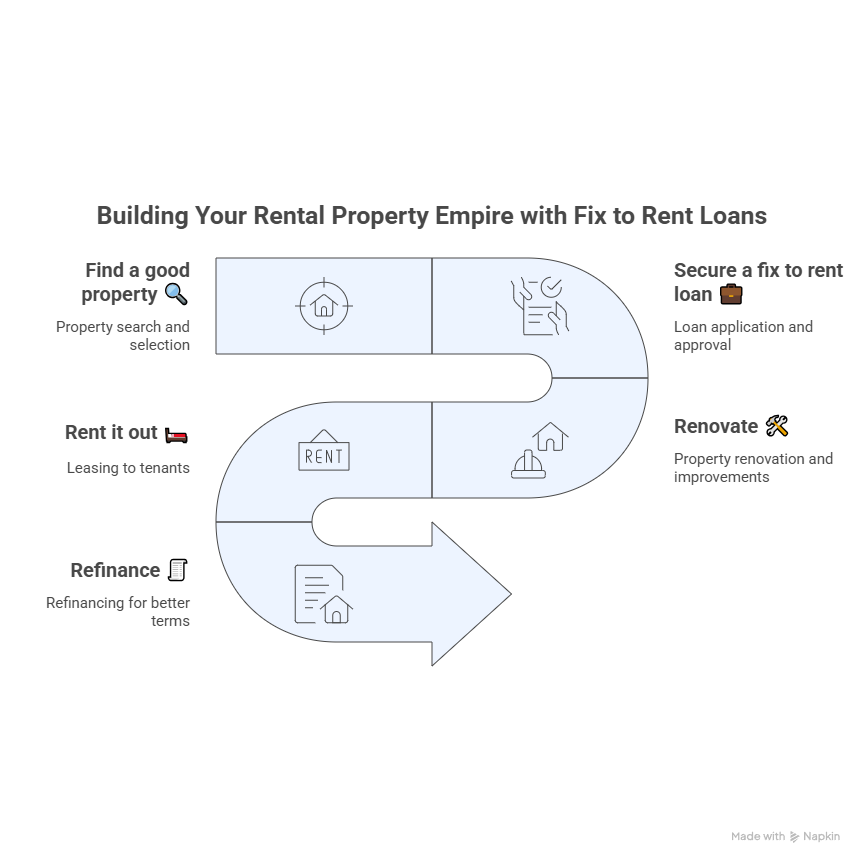

The Application Process for Fix to Rent Loans

<! - /wp:heading - >

<! - wp:paragraph - >

Securing a fix to rent loan involves a streamlined application process:

<! - /wp:paragraph - >

<! - wp:list {"ordered":true} - >

- <! - wp:list-item - >

- Pre-Qualification: Submit basic financial information, including credit history and investment experience.

- Property Analysis: Provide details on the property, including purchase price, rehab budget, and expected after-repair value.

- Loan Proposal: The lender evaluates the deal and offers terms, including interest rate, origination fee, and loan amount.

- Underwriting: The lender conducts appraisals and verifies financials.

- Closing: Sign documents and receive funds to start the project.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - wp:paragraph - >

For a smoother process, work with lenders familiar with 10XBNB’s rental strategies, as they understand the unique needs of short-term rental investors.

<! - /wp:paragraph - >

<! - wp:image {"id":3852,"sizeSlug":"full","linkDestination":"none"} - >

<! - /wp:image - >

<! - wp:heading - >

How to Maximize Fix to Rent Loan Success

<! - /wp:heading - >

<! - wp:paragraph - >

To make the most of fix to rent loans, follow these expert tips:

<! - /wp:paragraph - >

<! - wp:list - >

- <! - wp:list-item - >

- Conduct Thorough Market Research: Analyze local rental demand to ensure your property will attract tenants. Tools like 10XBNB’s Airbnb appraisal guide can help estimate property value and rental potential.

- Create a Detailed Rehab Budget: Account for all necessary repairs and unexpected costs to avoid budget overruns.

- Choose the Right Lender: Look for lenders with experience in fix to rent financing and competitive terms, such as low origination fees or flexible repayment options.

- Plan for Refinancing: Aim to refinance into a DSCR loan or conventional loan once the property is generating consistent rental income to reduce interest costs.

- Protect Your Investment: Ensure proper insurance coverage for your rental property. Learn more at 10XBNB’s insurance guide.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - wp:heading - >

Common Pitfalls to Avoid

<! - /wp:heading - >

<! - wp:paragraph - >

While fix to rent loans are powerful, investors should watch out for these pitfalls:

<! - /wp:paragraph - >

<! - wp:list - >

- <! - wp:list-item - >

- Underestimating Rehab Costs: Overly optimistic budgets can lead to funding shortages.

- Ignoring Tenant Demand: A property in a low-demand area may struggle to generate rental income.

- Overleveraging: Taking on too many loans can strain cash flow, especially during the rehab phase.

- Skipping Due Diligence: Failing to verify lender terms or property condition can derail the project.

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - wp:list-item - >

<! - /wp:list-item - >

<! - /wp:list - >

<! - wp:heading - >

Refinancing After Stabilization

<! - /wp:heading - >

<! - wp:paragraph - >

Once your property is renovated and leased, refinancing is a critical step to optimize financing. By transitioning to a long-term rental loan, such as a DSCR loan or conventional loan, you can secure lower interest rates and fixed-rate terms. This reduces monthly payments and improves cash flow, allowing you to scale your rental portfolio.

<! - /wp:paragraph - >

<! - wp:paragraph - >

For investors planning to sell their rental properties later, 10XBNB’s guide to selling Airbnb properties offers valuable insights on maximizing returns.

<! - /wp:paragraph - >

<! - wp:image {"id":2690,"sizeSlug":"large","linkDestination":"none"} - >

<! - /wp:image - >

<! - wp:heading - >

Why Choose 10XBNB for Fix to Rent Strategies?

<! - /wp:heading - >

<! - wp:paragraph - >

10XBNB is a leading resource for real estate investors looking to master the fix to rent model, particularly for short-term and mid-term rentals. Their platform offers tools, calculators, and guides to streamline the process, from property selection to financing and tenant management. By using 10XBNB’s expertise, investors can confidently navigate fix to rent loans and build a profitable rental portfolio.

<! - /wp:paragraph - >

<! - wp:paragraph - >

For example, their vacation rental accounting software guide helps investors track rehab costs, rental income, and loan payments.

<! - /wp:paragraph - >

<! - wp:heading - >

Conclusion

<! - /wp:heading - >

<! - wp:paragraph - >

Fix to rent loans are a major shift for real estate investors aiming to build wealth through rentals. By financing the purchase, rehab, and stabilization of properties, these loans enable investors to generate consistent rental income and scale their portfolios. With the right strategy, tools like those offered by 10XBNB, and a clear understanding of the process, you can turn distressed properties into cash-flowing assets. Whether you’re renovating a single-family home or a multifamily property, fix to rent loans provide the flexibility and funds needed to succeed in the competitive rental market.

<! - /wp:paragraph - >

<! - wp:paragraph - >

Start your journey today by exploring fix to rent loans and tapping into 10XBNB’s resources to maximize your investment potential.

<! - /wp:paragraph - >