Disclaimer: This article is for educational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently. Consult a licensed CPA or tax professional for guidance specific to your situation.

If you earned income as an Airbnb co-host or co-lister in 2026, you owe taxes on it. The IRS treats co-hosting income the same as any other self-employment income, and the reporting rules changed under the One Big Beautiful Bill Act (OBBBA) signed in 2025. Here is exactly how co-host income gets reported, what you can deduct, and how to structure your business to keep more of what you earn.

I have worked with co-listers who made $3,000 a month managing two properties and had no idea they needed to file quarterly estimated taxes. Others left thousands in deductions on the table because they did not track expenses. This guide covers the rules you actually need to know.

How Co-Host Income Gets Reported to the IRS

Co-host income is taxable regardless of whether you receive a 1099 form. The IRS requires you to report all income, even amounts below the filing thresholds. That said, the forms you receive depend on how you get paid.

Airbnb Pays You Directly Through the Co-Host Payouts Feature

When a property owner sets up co-listing on Airbnb and uses the platform’s co-host payouts feature, Airbnb splits the payment automatically. You receive your percentage directly from Airbnb into your bank account. In this case, Airbnb may issue you a Form 1099-K if you meet the reporting threshold.

Here is the part that confuses people: the listing owner’s 1099-K includes the full gross reservation amount, not just their share. According to the Airbnb Help Center, “Payouts shared with co-hosts through the Co-host payouts feature will not impact the amount which will be reported to the listing owner for tax information reporting purposes.” So both you and the owner may receive 1099s that, added together, exceed the total booking revenue. This is not double taxation. It is double reporting. You each report your actual share on your own return.

The Property Owner Pays You Directly

If the owner collects the full payout from Airbnb and then pays you separately (Venmo, check, bank transfer), Airbnb has no visibility into your payment. The owner is responsible for issuing you a Form 1099-NEC if they pay you $2,000 or more during the 2026 tax year. This threshold increased from $600 under Section 70433 of the OBBBA.

Many hosts do not realize they need to issue 1099-NECs to their co-hosts. If you manage properties under a direct payment arrangement, make sure to provide your W-9 to the property owner at the start of the relationship. A solid co-listing agreement should spell out who handles tax reporting.

The Double-Reporting Problem

The most common tax headache for co-hosts: the property owner receives a 1099-K for $80,000 in gross bookings. You, the co-host, receive a 1099-K for $16,000 (your 20% share paid through Airbnb). The IRS sees $96,000 in reported income for $80,000 in actual revenue. Neither of you did anything wrong. The owner deducts your co-host fees as a business expense on their Schedule C or Schedule E, which reconciles the numbers. But if the owner forgets to take that deduction, the math will not add up, and the IRS may send notices.

Keep a copy of your co-listing agreement and payment records. If you ever get an IRS notice about unreported income, these documents prove you only earned your share.

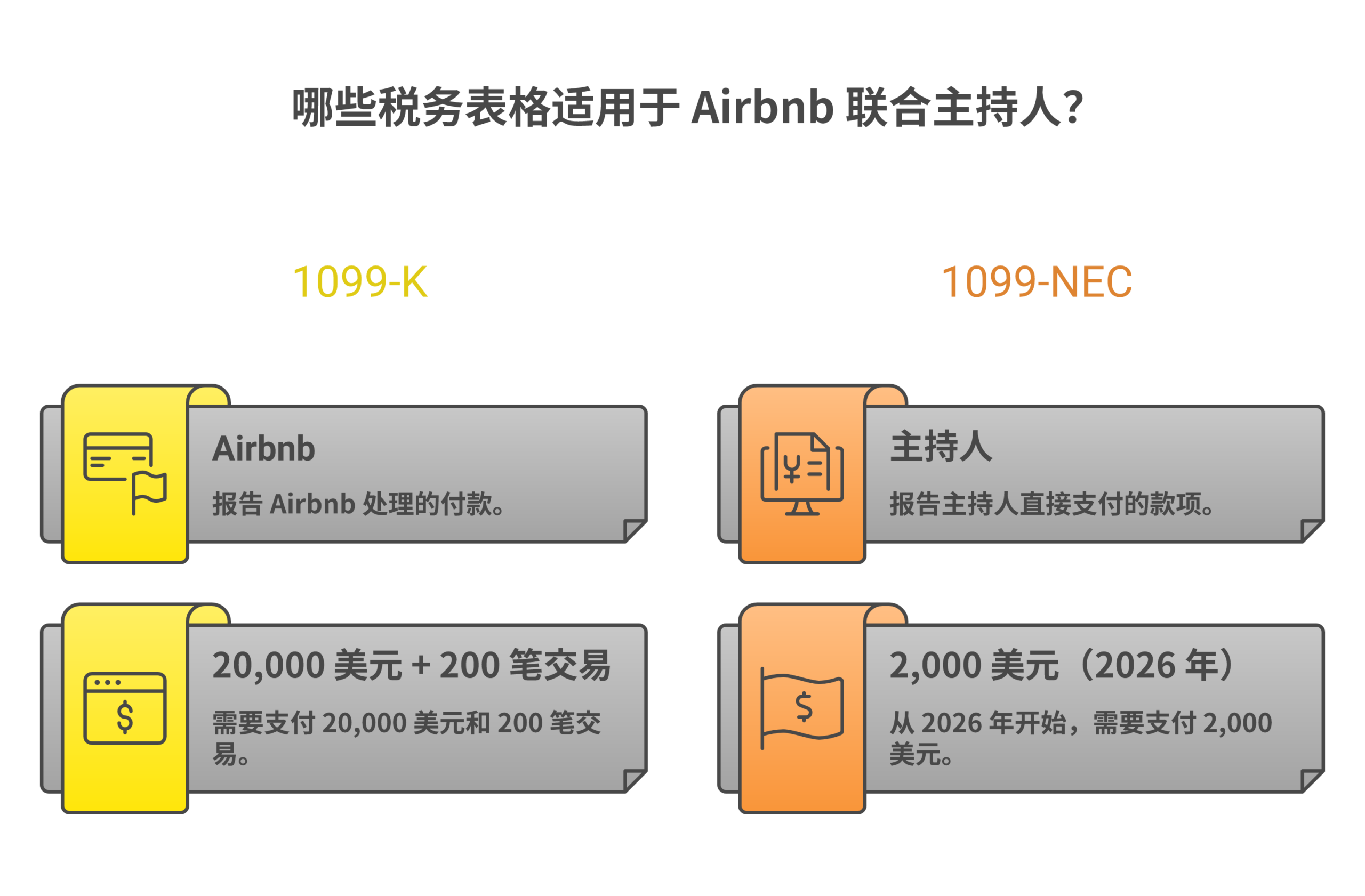

1099-K vs. 1099-NEC: Which One Will You Get?

The form you receive depends entirely on how your co-host income flows to you. Here is a side-by-side comparison with the updated 2026 thresholds.

| Detail | Form 1099-K | Form 1099-NEC |

|---|---|---|

| Who issues it | Airbnb (payment processor) | The property owner who pays you |

| When you receive it | Airbnb pays you directly via co-host payouts | Owner collects full payout, pays you separately |

| 2026 threshold | Over $20,000 AND over 200 transactions | $2,000 or more in total payments |

| Previous threshold | Was headed to $600 (reversed by OBBBA) | $600 (through 2025) |

| Where you report it | Schedule C (self-employment) | Schedule C (self-employment) |

| Subject to SE tax | Yes, 15.3% | Yes, 15.3% |

One important note: even if you fall below these thresholds and do not receive a 1099, you still owe taxes on the income. The thresholds only determine whether the payer must file a form with the IRS. Your obligation to report exists regardless.

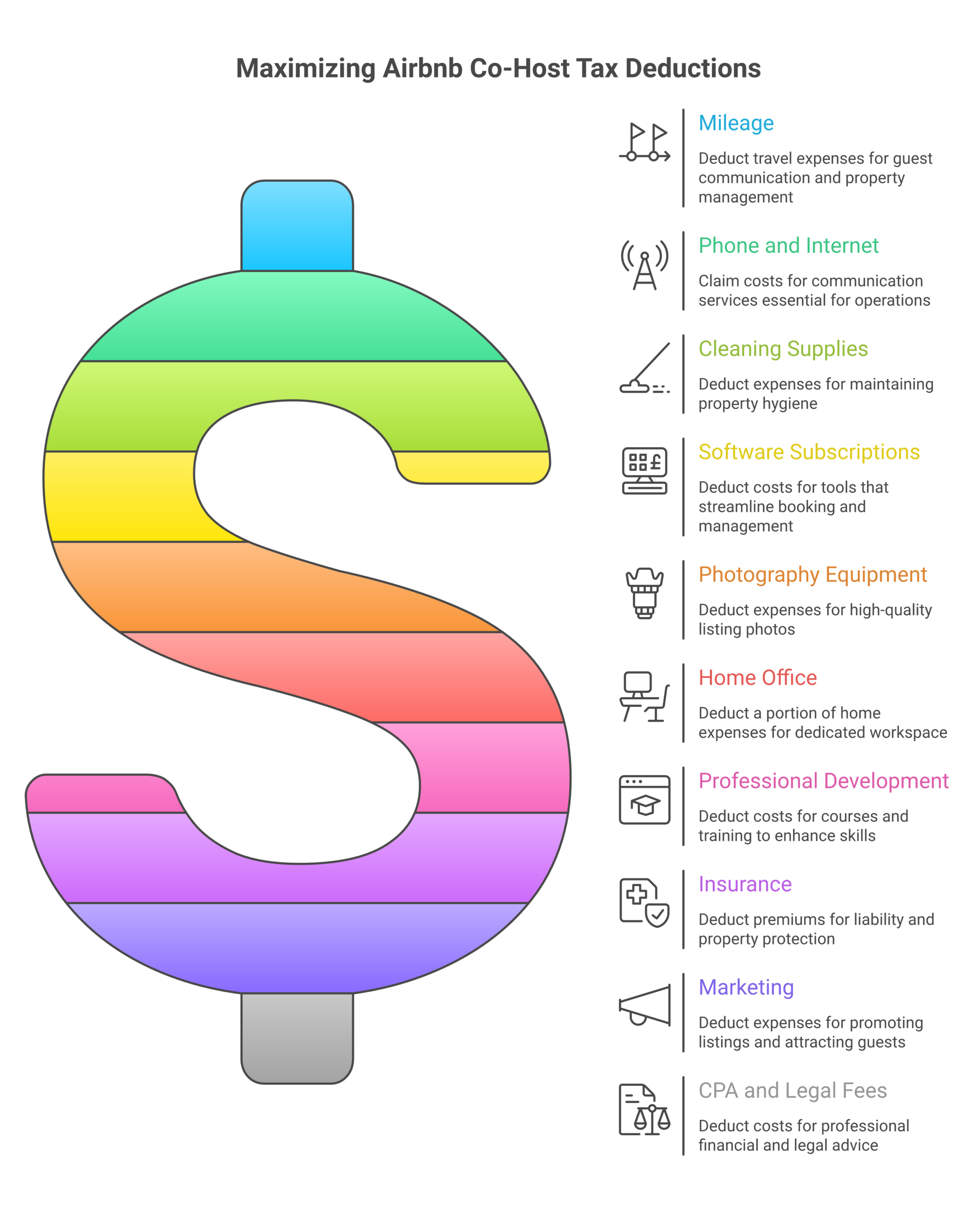

What You Can Deduct as an Airbnb Co-Host

Co-hosts can deduct ordinary and necessary business expenses against their co-hosting income. This is where most co-hosts leave money on the table. If you are not tracking these expenses, you are overpaying.

I have seen co-listers who manage five properties and never deducted their phone bill, their mileage, or the PriceLabs subscription they pay monthly. That adds up fast. Here is what qualifies.

| Expense Category | Examples | Estimated Annual Value |

|---|---|---|

| Mileage / Transportation | Driving to properties for turnovers, inspections, guest issues | $2,000 – $5,000+ (at $0.70/mile for 2026) |

| Phone and Internet | Business-use percentage of your phone plan, home internet | $600 – $1,200 |

| Cleaning Supplies | Supplies you purchase for turnovers (if you handle them yourself) | $300 – $800 |

| Software and Tools | PriceLabs, Hostaway, Guesty, Turno, iGMS, messaging tools | $1,200 – $3,600 |

| Photography Equipment | Camera, tripod, editing software for listing photos | $200 – $1,500 (first year) |

| Home Office | Dedicated space for guest communication, pricing, admin | $1,500 – $3,000 |

| Professional Development | Courses, conferences, coaching, books on STR management | $500 – $5,000 |

| Insurance | General liability, professional liability (E&O) for your co-hosting business | $500 – $2,000 |

| Marketing | Website, business cards, local advertising to acquire new clients | $200 – $2,000 |

| Professional Services | CPA, tax preparation, attorney for contracts | $500 – $2,500 |

The Mileage Deduction Alone Can Save You Thousands

The IRS standard mileage rate for 2025 was $0.70 per mile. If you drive 15 miles round-trip to a property three times a week across 10 properties, that is 450 miles per week, or roughly 23,400 miles per year. At $0.70 per mile, that is a $16,380 deduction. Even co-listers managing 2-3 properties within a 10-mile radius typically log 5,000+ miles annually.

Use a mileage tracking app like MileIQ, Everlance, or Hurdlr. Manual logs work too, but apps create automatic records that hold up during an audit. The IRS requires you to document the date, destination, business purpose, and miles driven for each trip.

Home Office Deduction

If you manage properties remotely (guest messaging, pricing adjustments, scheduling cleaners), you can claim the home office deduction. The simplified method allows $5 per square foot up to 300 square feet, for a maximum of $1,500. The regular method calculates actual expenses (rent, utilities, insurance) based on the percentage of your home used exclusively for business.

The key word is “exclusively.” A kitchen table where you also eat dinner does not qualify. A spare bedroom converted to a co-hosting command center does.

Software Subscriptions Add Up Fast

Most active co-listers use multiple tools. PriceLabs runs $20-40 per listing per month. Hostaway or Guesty can run $25-50+ per listing monthly. Add Turno for cleaning coordination, a smart lock subscription, and a messaging automation tool, and you could easily spend $200-400 per month on software across a portfolio of 5-10 listings. That is $2,400-$4,800 per year in deductible business expenses.

Business Entity Options for Co-Hosts

The question every co-lister asks after their first tax season: should I form an LLC? The answer depends on your income level, risk tolerance, and growth plans. Here is how the three most common structures compare.

| Factor | Sole Proprietorship | Single-Member LLC | S-Corp (or LLC taxed as S-Corp) |

|---|---|---|---|

| Setup cost | $0 | $50 – $500 (varies by state) | $500 – $1,500 (formation + S-Corp election) |

| Liability protection | None. Personal assets exposed | Yes. Separates personal and business assets | Yes. Same as LLC |

| Tax filing | Schedule C on personal return | Schedule C on personal return (default) | Separate S-Corp return (Form 1120-S) + personal |

| Self-employment tax | 15.3% on all net profit | 15.3% on all net profit | 15.3% only on your salary (not distributions) |

| Annual maintenance | Minimal | $0 – $800/yr (state annual report fees) | $1,000 – $3,000/yr (payroll + tax prep) |

| Best for | Just starting, under $20K/yr income | $20K – $60K/yr, want liability protection | Over $50K – $60K/yr net profit |

The S-Corp Tax Savings Math

Self-employment tax is 15.3% (12.4% Social Security + 2.9% Medicare). As a sole proprietor or single-member LLC, you pay this on your entire net profit. With an S-Corp, you pay yourself a “reasonable salary” and take the rest as distributions, which are not subject to SE tax.

Example: You earn $80,000 net profit co-listing. As a sole proprietor, you pay roughly $11,300 in SE tax (after the 92.35% adjustment). As an S-Corp, you pay yourself a $45,000 salary. SE tax on $45,000 is about $6,885. The remaining $35,000 comes as a distribution with no SE tax. That saves you about $4,400 per year.

But S-Corps have costs: payroll processing ($30-$75/month), a separate tax return ($500-$1,500 to prepare), and stricter record-keeping. The break-even point is typically around $50,000-$60,000 in net profit. Below that, the S-Corp compliance costs eat into the savings.

Why an LLC Makes Sense for Most Co-Listers

Even if you do not pursue S-Corp taxation, forming a single-member LLC creates a legal separation between your personal assets and your co-hosting business. If a guest gets injured at a property you manage and files a lawsuit naming you, an LLC shields your personal savings, home, and other assets (assuming you maintain proper separation).

The cost is minimal in most states. Wyoming charges $100 to form an LLC with a $60 annual report. Delaware charges $90 with a $300 annual tax. Your home state may charge more or less. The difference between co-listing and rental arbitrage matters here too: co-listers typically have lower liability exposure than arbitrage operators who hold leases, but the protection is still worth having.

Quarterly Estimated Tax Payments

If you expect to owe $1,000 or more in federal tax for the year, the IRS requires you to make quarterly estimated payments. Most co-hosts with consistent income fall into this category.

2026 Due Dates

| Payment Period | Income Earned | Due Date |

|---|---|---|

| Q1 | January 1 – March 31 | April 15, 2026 |

| Q2 | April 1 – May 31 | June 15, 2026 |

| Q3 | June 1 – August 31 | September 15, 2026 |

| Q4 | September 1 – December 31 | January 15, 2027 |

How to Calculate Your Quarterly Payment

The simplest approach: take last year’s total tax liability and divide by four. This is the “safe harbor” method. If you pay at least 100% of last year’s tax (or 110% if your adjusted gross income exceeded $150,000), you avoid underpayment penalties regardless of what you actually owe for 2026.

The alternative: estimate your current-year income and pay at least 90% of what you will owe. This works better if your income dropped compared to last year.

Quick formula for new co-hosts:

- Estimate your annual co-hosting income

- Subtract estimated deductions

- Multiply net profit by your effective tax rate (federal income tax bracket + 15.3% SE tax, minus the 50% SE tax deduction)

- Divide by 4

For example, if you expect $40,000 in net co-hosting income and your combined effective rate is around 30% (including SE tax), your quarterly payment would be about $3,000. Pay via IRS Direct Pay at irs.gov/payments or through EFTPS.

Penalty for Missing Payments

The IRS charges interest on underpaid estimated taxes. The rate adjusts quarterly and has been running around 7-8% annualized in recent periods. You avoid the penalty if you owe less than $1,000 at filing, or if you paid at least 90% of the current year’s tax, or 100% of last year’s tax (110% for high earners).

State-by-State Considerations

Federal taxes are only half the picture. State and local taxes add layers that vary wildly depending on where you operate.

State Income Tax

Nine states have no income tax: Alaska, Florida, Nevada, New Hampshire (limited to interest and dividends through 2024, fully eliminated in 2025), South Dakota, Tennessee, Texas, Washington, and Wyoming. If you are a co-lister in Texas managing properties in Texas, your state tax burden is zero. If you live in California and manage California properties, you are looking at up to 13.3% state income tax on top of federal.

Where you live matters, but so does where the properties are located. Some states require you to file a non-resident return if you earn income from properties in that state. If you are a Florida-based co-lister managing a cabin in North Carolina, you may owe North Carolina income tax on that income.

Transient Occupancy Taxes

Most cities and counties charge a transient occupancy tax (TOT) or hotel tax on short-term rentals. Airbnb collects and remits this in many jurisdictions automatically. But here is the question co-hosts need to answer: who is responsible when Airbnb does not collect it?

In most co-listing arrangements, the property owner bears this responsibility. Your co-listing agreement should clarify this. But if you are operating under a property management license or managing listings under your own account, the obligation may fall on you. Check your local regulations.

Business Licensing

Some states and cities require a business license or property management license for co-hosting. California, for example, requires a real estate broker license if you manage more than a certain number of properties for compensation (with some exemptions for short-term rentals). Florida has similar requirements through their real estate commission. Research your state’s rules before scaling.

Record-Keeping for Co-Hosts

Good records are your best protection in an audit and your best tool for maximizing deductions. Here is what to track and how to keep it.

What to Save

- Income records: Airbnb payout statements (downloadable from your earnings dashboard), 1099 forms, payment confirmations from property owners

- Expense receipts: Every receipt over $75 (the IRS requires documentation for expenses $75 and above, though tracking smaller amounts is smart)

- Mileage logs: Date, destination, purpose, miles driven for each business trip

- Contracts: Co-listing agreements, property management contracts, vendor agreements

- Bank statements: Separate business bank account statements (if you do not have a separate account yet, open one)

- Software subscriptions: Annual billing summaries from PriceLabs, Hostaway, and other tools

Apps for Tracking

QuickBooks Self-Employed ($15/month) or Wave (free) handle income and expense categorization. MileIQ ($5.99/month) or Everlance (free tier available) track mileage automatically using your phone’s GPS. Keeper Tax ($16/month) specifically targets freelancers and automatically scans bank transactions for deductions.

At minimum, maintain a spreadsheet with monthly income and expenses by category. It takes 20 minutes a month and saves hours during tax season.

How Long to Keep Records

The IRS generally has three years to audit a return. Keep records for at least three years after filing. If you underreported income by more than 25%, the IRS has six years. Many CPAs recommend keeping records for seven years to be safe. Digital storage makes this easy, so there is little reason not to.

When to Hire a CPA

Not everyone needs a CPA. If you manage one or two properties, earn under $20,000 per year, and operate as a sole proprietor, tax software like TurboTax Self-Employed or FreeTaxUSA can handle your return. The cost is $50-$120.

Hire a CPA if:

- You earn over $40,000 per year from co-hosting

- You manage properties in multiple states

- You are considering an S-Corp election

- You have other self-employment income streams

- You want to claim the home office deduction using the regular method

- You received an IRS notice or are being audited

What to Expect on Cost

A basic Schedule C return preparation (co-hosting income + deductions, single state) runs $200-$500 at most CPA firms. If you need multi-state returns, S-Corp filing (Form 1120-S), or entity restructuring advice, expect $500-$1,500. Some firms offer monthly bookkeeping packages ($100-$300/month) that include year-end tax prep.

Look for a CPA familiar with short-term rental taxation. Not all tax professionals understand the difference between Schedule C and Schedule E for STR income, and the classification matters. Co-hosts who actively manage properties (pricing, guest communication, maintenance coordination) typically report on Schedule C as self-employment income. Passive investors use Schedule E.

The Self-Employment Tax Deduction Most Co-Hosts Overlook

You can deduct 50% of your self-employment tax when calculating your adjusted gross income. This is an “above the line” deduction, meaning you get it whether you itemize or take the standard deduction.

On $60,000 of net co-hosting income, your SE tax is roughly $8,478 (after the 92.35% adjustment). Half of that, $4,239, reduces your taxable income. At a 22% federal bracket, that saves you about $933 in income tax. It is not a massive windfall, but it is money that belongs to you if you claim it. Tax software calculates this automatically, but co-hosts doing back-of-envelope math often forget to include it.

How Becoming a Co-Host Through Co-Listing Changes the Tax Picture

The Airbnb co-listing model where you manage someone else’s property for a revenue share has a fundamentally different tax treatment than owning rental property yourself. As a co-lister, you are providing a service, not earning rental income. This means:

- You report on Schedule C (not Schedule E)

- You pay self-employment tax on net profit

- You cannot depreciate the property (you do not own it)

- You cannot deduct property taxes, mortgage interest, or insurance on the property itself

- You can deduct YOUR business expenses (mileage, phone, software, etc.)

This distinction matters when planning your tax strategy. Co-listers often earn strong income with relatively low overhead, which means a larger percentage of revenue hits your tax return as net profit. Smart deduction tracking and the right entity structure become even more important.

Shaun Ghavami, who studied finance at UBC’s Sauder School of Business and built a portfolio generating over $100 million in Airbnb bookings, teaches the co-listing model specifically because of its low-barrier entry. The tax simplicity is part of that appeal: no property depreciation schedules, no passive activity loss rules, no rental real estate professional status requirements. Just income, deductions, and a straightforward Schedule C. If you want to learn the full model, explore co-listing training here.

Frequently Asked Questions

Do I need to pay taxes on Airbnb co-hosting income if I did not receive a 1099?

Yes. The IRS requires you to report all income regardless of whether you receive a 1099. The 1099 threshold only determines whether the payer must file the form. You owe taxes on every dollar of co-hosting income.

Can I deduct expenses if I do not have an LLC?

Yes. Business deductions are available to sole proprietors, LLCs, and S-Corps alike. An LLC is a legal structure, not a tax classification. Sole proprietors deduct expenses on Schedule C just like an LLC owner.

What is the difference between Schedule C and Schedule E for co-hosts?

Schedule C is for self-employment income (services you provide). Schedule E is for passive rental income (property you own). Co-hosts who actively manage properties for a fee use Schedule C. Property owners who rent their own properties typically use Schedule E. The distinction matters because Schedule C income is subject to self-employment tax.

Should I form an LLC before I start co-hosting?

You can start as a sole proprietor and form an LLC later. Many co-listers operate as sole proprietors during their first year while they validate the business model, then form an LLC once they are managing multiple properties. There is no tax penalty for waiting.

How does the Qualified Business Income (QBI) deduction apply to co-hosts?

Co-hosting income reported on Schedule C may qualify for the 20% QBI deduction under Section 199A. This allows you to deduct up to 20% of your qualified business income, subject to income limitations. For 2026, the full deduction phases out for single filers above $191,950 and joint filers above $383,900 (indexed for inflation). A CPA can confirm your eligibility.

Do I need to collect sales tax as a co-host?

In most cases, no. Airbnb collects and remits occupancy taxes in most jurisdictions. However, a few cities require the operator (which could be you, depending on your agreement) to register and file separately. Check your local municipality’s short-term rental regulations.

What happens if the property owner does not send me a 1099-NEC?

You still report the income. Many small hosts are unaware of their obligation to issue 1099-NECs. Keep your own records of payments received. If you earned $2,000 or more in 2026 and did not receive a 1099-NEC, you may want to remind the property owner, but your tax obligation exists either way.

Can I deduct co-hosting training and courses as a business expense?

Yes. Professional development directly related to your co-hosting business is deductible. This includes courses, coaching programs, industry conferences, and educational materials. The expense must be “ordinary and necessary” for your business, which co-hosting education clearly qualifies as.

Disclaimer: This guide is for informational and educational purposes only. It does not constitute tax, legal, or financial advice. Tax laws change frequently, and individual circumstances vary. Always consult a licensed CPA or tax professional before making tax decisions based on this content.

Want to Build a Co-Listing Business That Actually Cash Flows?

Learn the exact system behind a portfolio that has generated over $100 million in Airbnb bookings, without owning a single property. Shaun Ghavami’s free training breaks down the co-listing model step by step.